We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Top Easy Access Savings Discussion Area

Comments

-

A bit like RBS were too big to fail? I seem to remember they were pretty big. I would just stay under FSCS and spread the load or go NS&Icwep2 said:

Personally, I'd happily put much more in Santander, Chase, even on a permanent basis. These are backed up by extremely well capitalised banks. Banks that are to big to fail to some extent. Would say same for Barclays, HSBC and a few other UK high street (bank) names, but they don't tend to be top of the tables for more than limited size accounts - a regular saver limited to £250/month isn't going above the 85k limit....SeriousHoax said:Hi I know it's a good thing to spread your money about to be on the safe side. £85k

Anyway is there many here that sticks more than 85k in an account.

In short term I'd happily put more in Marcus and Investec (eg if I had a fix maturing in 2 months and wanted to open another one) as these are backed by big, if a little less big, banks. Would probably lump the big UK building societies in with this group as well.

Anyone else I'd stick below the FCA guarantee, as long as I've verified it myself on the FCA website.16 Panel (250W JASolar) 4kWp, facing 170 degrees, 40 degree slope, Solis Inverter. Installed 29/9/2015 - £4700 (Norfolk Solar Together Scheme); 9.6kWh US2000C Pylontech batteries + Solis Inverter installed 12/4/2022 Year target (PVGIS-CMSAF) = 3880kWh - Installer estimate 3452 kWh:Average over 6 years = 4400 :j1 -

Had trouble with Kroo because they were overloaded so took 2 days. Tandem the other day took literally 2 minutes from app download until first funding. Maybe check your credit files as this might be a reason why you can't be verified by those institutions. Some cashback is in it as well with topcashack and Experian full file you can access with MSE Credit Club for free.samlad80 said:Just wondering if people are having similar experiences to me..

I’ve tried to open a Kroo account, waiting 10 days now with no sign of any progress on the authentication process.I’ve also tried to open a tandem account for a similar rate, again - it went straight to authentication with no email, nothing.It’s great of Martin to recommend these products but - if they can’t provide what’s advertised are they actually any good??0 -

Yeah they (RBS) *were* too big to fail, which is why the UK govt bailed them out.Rheumatoid said:

A bit like RBS were too big to fail? I seem to remember they were pretty big. I would just stay under FSCS and spread the load or go NS&Icwep2 said:

Personally, I'd happily put much more in Santander, Chase, even on a permanent basis. These are backed up by extremely well capitalised banks. Banks that are to big to fail to some extent. Would say same for Barclays, HSBC and a few other UK high street (bank) names, but they don't tend to be top of the tables for more than limited size accounts - a regular saver limited to £250/month isn't going above the 85k limit....SeriousHoax said:Hi I know it's a good thing to spread your money about to be on the safe side. £85k

Anyway is there many here that sticks more than 85k in an account.

In short term I'd happily put more in Marcus and Investec (eg if I had a fix maturing in 2 months and wanted to open another one) as these are backed by big, if a little less big, banks. Would probably lump the big UK building societies in with this group as well.

Anyone else I'd stick below the FCA guarantee, as long as I've verified it myself on the FCA website.

Generally speaking massive retail banks (say with >5% market share) will be a massive societal problem if they go under, sure you have FSCS which covers most, but salaries not being accessible, direct debits not being paid, no access to cash machines for >5% of the population, it *might* be manageable but it might be carnage which is essentially why Gordon Brown made that decision back in 2008.

I happened to know some of the people (at RBS) who had to make the call that they needed to go to the treasury/BoE, that if something didn't happen they couldn't fund themselves (because other banks wouldn't lend to them) and they wouldn't make payments. It was a political decision to choose to save them. Note that Lehman didn't have a retail banking side, they were only an investment bank and they were allowed to fail, so the impact on 'general population' would be limited in that case and decision was different.

That's essentially why in a post on previous page I distinguished between Chase and Marcus, one is backed by a retail bank in the US (which also has an investment banking arm ~25% of company), the other is backed by a 90% investment bank. Chase/JPMorgan is 3-5x the size of Goldman Sachs, but I guess when you are in the trillions of assets it maybe is a moot point comparing, but Santander as well is massive retail bank in Spain, as well as many other places in Europe, the Spanish govt would probably see them as too big to fail, but Chase (JPMorgan) vs Marcus (Goldman Sachs) there's one the US govt would see as too big to fail and one that they've shown in the past they have let fail, sure they may make different decision this time but on that basis alone, with my money I see less risk with one vs the other.

Of course capital requirements and regulations in the last 15 years mean than all banks have had to put much more aside to cover any risks, with the aim that 2008 would never happen again, so in theory they are *all* much safer now than then.3 -

Love it how some people seem to have wiped Lehman Brothers from their memory.0

-

And it all started with Bear Stearns, which was sold to, guess who, JPMorgan ChaseBand7 said:Love it how some people seem to have wiped Lehman Brothers from their memory.0 -

Maybe we could start another thread to discuss the stability of the banking sector

3

3 -

'Savers don't WANT more interest on easy access accounts' bank bosses tell MPs - saying they prefer regular savers with better rates but more restrictions

https://www.thisismoney.co.uk/money/saving/article-11723171/Bank-bosses-defend-savings-rates-MPs-saying-customers-dont-want-easy-access.html

Apparently we don't want more interest on easy access accounts...interesting...If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.1 -

Well I suppose we want the highest rates possible but thinking about it if easy access rates were the highest nobody would go for notice accounts.ForumUser7 said:'Savers don't WANT more interest on easy access accounts' bank bosses tell MPs - saying they prefer regular savers with better rates but more restrictions

https://www.thisismoney.co.uk/money/saving/article-11723171/Bank-bosses-defend-savings-rates-MPs-saying-customers-dont-want-easy-access.html

Apparently we don't want more interest on easy access accounts...interesting...1 -

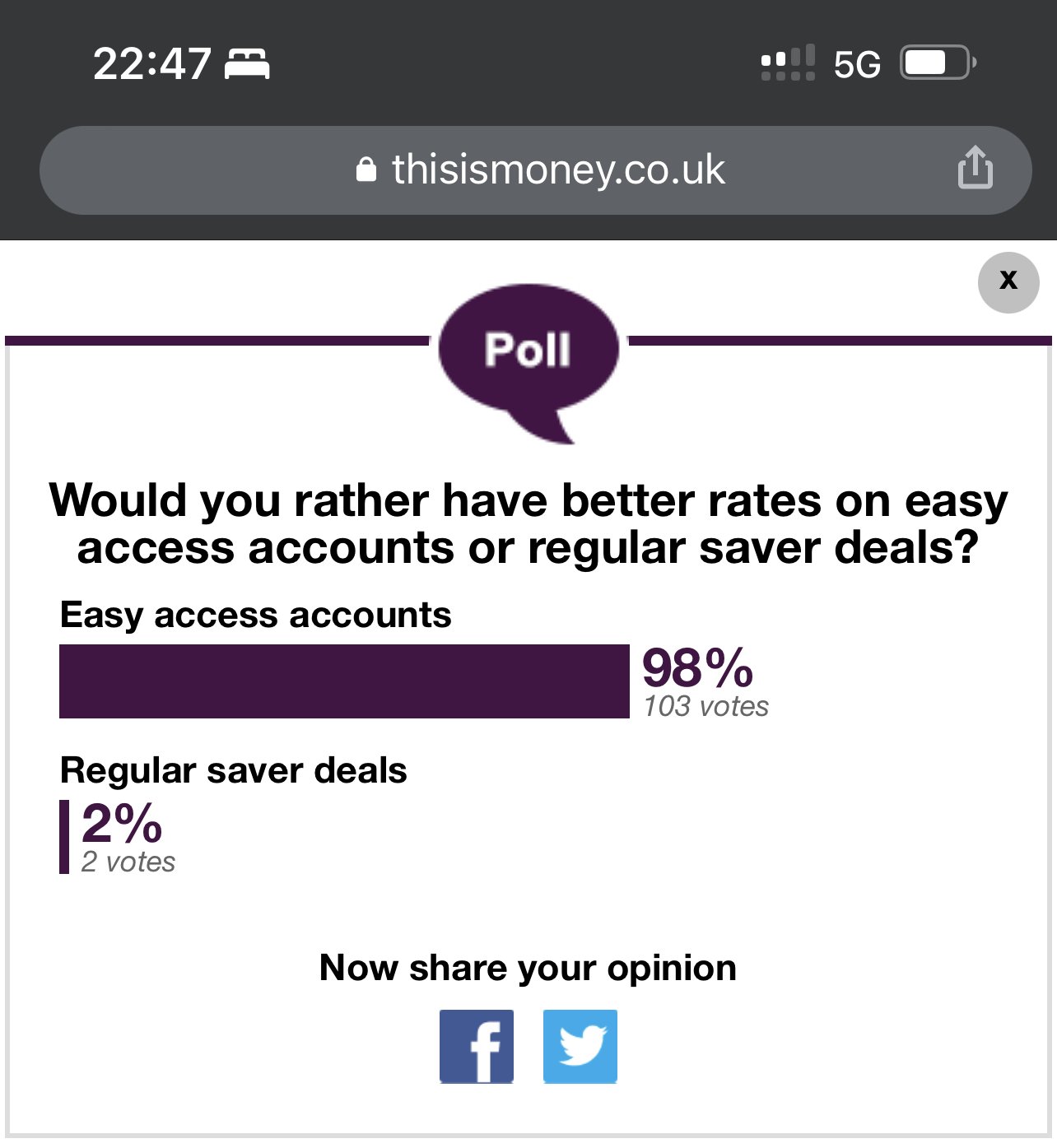

There’s an under-loved poll in this articleForumUser7 said:'Savers don't WANT more interest on easy access accounts' bank bosses tell MPs - saying they prefer regular savers with better rates but more restrictions

https://www.thisismoney.co.uk/money/saving/article-11723171/Bank-bosses-defend-savings-rates-MPs-saying-customers-dont-want-easy-access.html

Apparently we don't want more interest on easy access accounts...interesting...

And the explanation offered by thisismoney for the Regular Saver interest rates is a total car crash 🤦🏽♀️ 0

0 -

Thanks for the heads-up. I have a Triple Access account that I’m planning to close before the end of the tax year, to use up what’s left of my PSA, but it was getting to the point where I would lose more by keeping the money in there at 2.65% than the amount I’d be saving in tax.GalacticaActual said:Skipton Building Society have now issued a PDF showing the rate changes to variable accounts effective from Monday 13th February 2023:

https://www.skipton.co.uk/-/media/skipton-co-uk/pdf/savings/changes-to-variable-accounts.ashx

https://www.skipton.co.uk/base-rate-changeWith effect from Monday 13 February 2023, we will be increasing all our variable savings rates, with no variable rate product paying less than 2.25% AER.1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards