We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

DMP mutual support thread part 13 !!

Comments

-

@Inafunk2025

This question has been posted many times previously, its a common concern.

If you re-mortgage with your current lender, no credit check is usually performed, so your credit file doesn't matter to a great extent.

Its only an issue if you choose a product with another lender.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

@Inafunk2025

I switched my mortgage at least twice when I was in a DMP. As sourcrates has said, its only an issue if you choose a new mortgage with another lender, but also if you look to change the terms of your current one (by that I mean borrow more or alter the years remaining - that may trigger a hard search).

0 -

Trying to get W*sc*t to agree a F&F , but they say the debt is still owned by L**k and they are managing it on their behalf. I have explained the money is coming from a relative who is trying to help us out, and answered all their questions about how much total debt we have etc, but now they have come back to me saying I have to fill in a I&E form for them to be able to consider it. I have emailed back and asked them how that is even relevant if the money is coming as a gift from FIL and in no way impacts our day to day spending. Is it likely they will agree without me filling this in. I thought the days of filling in those, were long gone from back when we first started the DMP route. Thing that worries me is we have been saving EF pots and other savings pots, so if they think we have more money than we say, we have, they will not accept our offer. Has any one had F&Fs accepted without filling in the forms.Making the debt go down and savings go up

LBM 2015 - debt £57K / Now £26,104....its going down

Mortgage Free December 9th 2024! 18mths ahead of schedule.Challenges

EF £290/3000

Studies/surveys July £70.99

Decluttering items 1400/2025. 345/2026

Books read 23 in 2025. 2026- 15 (target is 52)

Jigsaws done 20 in 2025. 3 this year.

My debt free diary...https://forums.moneysavingexpert.com/discussion/6396218/we-will-get-this-debt-d£own-the-savings-up0 -

Wescott are simply collecting this debt on behalf of their client, they are just a 3rd party engaged to collect your payments, that`s it.Makingabobor2 said:Trying to get W*sc*t to agree a F&F , but they say the debt is still owned by L**k and they are managing it on their behalf. I have explained the money is coming from a relative who is trying to help us out, and answered all their questions about how much total debt we have etc, but now they have come back to me saying I have to fill in a I&E form for them to be able to consider it. I have emailed back and asked them how that is even relevant if the money is coming as a gift from FIL and in no way impacts our day to day spending. Is it likely they will agree without me filling this in. I thought the days of filling in those, were long gone from back when we first started the DMP route. Thing that worries me is we have been saving EF pots and other savings pots, so if they think we have more money than we say, we have, they will not accept our offer. Has any one had F&Fs accepted without filling in the forms.

They will have been given certain boundaries that they can work between in terms of accepting offers to settle, if your offer falls outside of these boundaries, they have to refer the matter back to their client for approval.

They will follow certain guidelines in order to assess your offer, if you want it to be considered, you will have to jump through their hoops I`m afraid.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Yes, it just seems odd as we've never been asked that on other ones we have settled. L*n* do certainly seem to be the hardest ones to deal with. I hadn't even realised they still owned it, I thought they had sold it to W*sc*t. It was originally a B/cd debtsourcrates said:

Wescott are simply collecting this debt on behalf of their client, they are just a 3rd party engaged to collect your payments, that`s it.Makingabobor2 said:Trying to get W*sc*t to agree a F&F , but they say the debt is still owned by L**k and they are managing it on their behalf. I have explained the money is coming from a relative who is trying to help us out, and answered all their questions about how much total debt we have etc, but now they have come back to me saying I have to fill in a I&E form for them to be able to consider it. I have emailed back and asked them how that is even relevant if the money is coming as a gift from FIL and in no way impacts our day to day spending. Is it likely they will agree without me filling this in. I thought the days of filling in those, were long gone from back when we first started the DMP route. Thing that worries me is we have been saving EF pots and other savings pots, so if they think we have more money than we say, we have, they will not accept our offer. Has any one had F&Fs accepted without filling in the forms.

They will have been given certain boundaries that they can work between in terms of accepting offers to settle, if your offer falls outside of these boundaries, they have to refer the matter back to their client for approval.

They will follow certain guidelines in order to assess your offer, if you want it to be considered, you will have to jump through their hoops I`m afraid.Making the debt go down and savings go up

LBM 2015 - debt £57K / Now £26,104....its going down

Mortgage Free December 9th 2024! 18mths ahead of schedule.Challenges

EF £290/3000

Studies/surveys July £70.99

Decluttering items 1400/2025. 345/2026

Books read 23 in 2025. 2026- 15 (target is 52)

Jigsaws done 20 in 2025. 3 this year.

My debt free diary...https://forums.moneysavingexpert.com/discussion/6396218/we-will-get-this-debt-d£own-the-savings-up0 -

Hi Newbie here!

I’m currently in £26k worth of debt. I have been with Payplan since July 2024, making £703 monthly payments.It’s my husband and I’s goal to be debt free by the beginning of 2026.

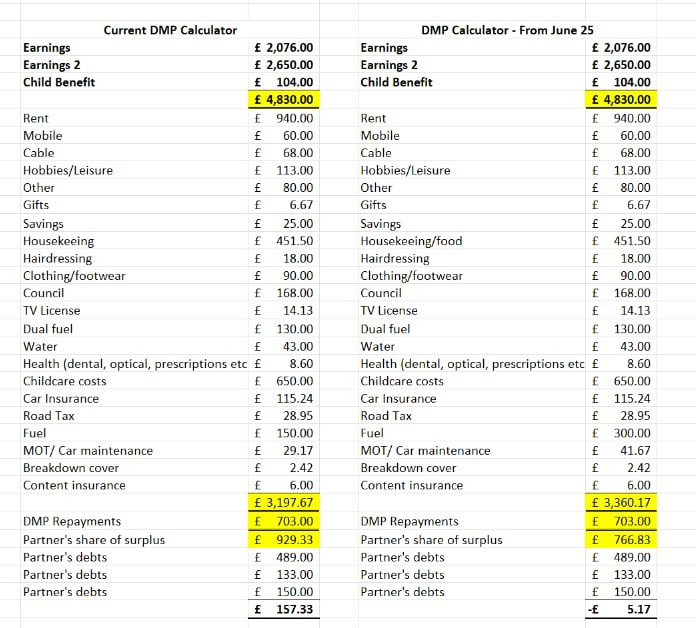

Since starting my DMP, my husband started a new job which pays him very well and has allowed him to be able to pay his debt (currently £9k) quicker than expected and then save some money on the side. We are budgeting to have around £10k saved by the end of December. By that point my debt should stand at £18.4k

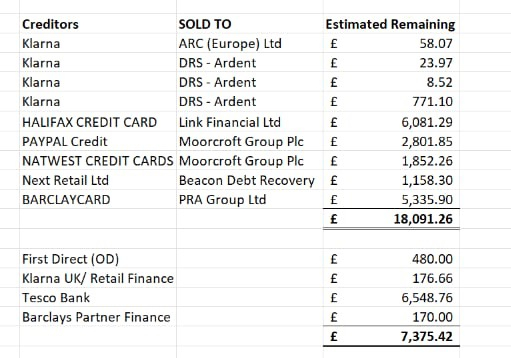

So we wanted to know how likely or how can we prepare ourselves to offer final payment settlements to my creditors. I have read that debt sold to third parties are more likely to accept 40-55% of the debt.

I have gone through my list of creditors and I can see that some of them haven’t been sold to a debt recovery agency. Eg Tesco, I believe this is because the monthly payment offered to them by Payplan is actually more than what the agreed monthly repayment is. To the point where every month I get a letter from them thanking me for my overpayment. For this reason, I was thinking of “changing the outgoings” when doing my Payplan yearly DMP calculation so my monthly payments are reduced and hopefully Tesco ends up selling my loan too. Is this a plausible idea? What do you recommend me to do?

Also, I’m not sure if this is relevant but I’m planning to get pregnant in June-July, which would mean I’m going to go on maternity leave in March-April 2026 so my salary will reduce to SMP.

I have attached my current DMP and creditor list.

Tia, a mum on her way to be debt free.

0

0 -

Hey all.

Just managed to escape being tied to a family mortgage which left my finances a mess in 2016 and I wasn't even able to live there. I have managed to get equity from with which I can clear my DMP . I was dealing with step change who were life savers at the time. I haven't spoken to them yet, but what's the best approach to keep as much of the equity as possible, not !!!!!! lenders and finally end the DMP. I'm happy to off a 100% of it, but would be delighted if I can get it down to 70%. Would it be best to call each debt, ask for full final settlement? Or ask step change to negotiate?0 -

Dear thread, thank you everyone who has given their expertise, I have read many pages of this thread and taken in so much information, you have been so helpful and I gathered the courage to cancel my DMP and go self-managed. I have one question which I have tried to find the info on but I am getting confused with overload. My first credit card letter intending to default me has arrived and I am very pleased to have received it. They explain that if I don't pay they will default, which I understand is what I want.

My confusion is, when they default, do I contact them then? Or do I keep waiting for it to be sold? Is it safe to keep waiting after the default or is that the time to write and offer them a small amount? I am not worried about the first card as it is very small but I have a loan over £13k which will make me slightly nervous if I continue to ignore them after it defaults. I am worried because I know some companies do not sell it on! How do I decide how long to wait?

Thank you very much for your help.

DettyLBM: 💡February 2025💡 DMP debt: 💰 £0 repaid of £33,753 💰 Self-Managed DMP starting date: 📆 March 2025 📆 Debt Charity's projected finish date: 📆 January 2044 📆 Detty's hoped finish date: 📆 December 2034 📆0 -

Hi @Debt_Overload

The default process takes a few weeks, during that time the creditor will be deciding what to do with your account, depending on there particular company policy, they may sell the debt, they may assign it to a collector to manage, they may do the collection work themselves, or they may not do anything.

Whatever they decide, they, or whoever gets a hold of your account, will write to you in due course, just wait and see who it is, then you can arrange payments or whatever directly with them.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Hi,

I want to write an affordability complaint but my debt was sold to Cabot but it was originally from MBNA.

Do I need to address my complaint to Cabot or MBNA?

Thanks…tksnota0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards