We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Why doesn't everyone just buy Vanguard LifeStrategy?

Comments

-

Would you kindly explain "historical efficient frontier"? Thanks.bostonerimus wrote: »Active funds certainly have the potential to beat a passive index fund. If I could know the performance of funds a year ahead I would definitely be 100% active, but as I don't have a working crystal ball I'm 100% index tracker funds and use [strike]guess work[/strike] research and the historical efficient frontier to come up with an asset allocation. In the accumulation phase I did not look to maximize my possible return, I attempt to minimize the probability of investment failure and I chose an allocation that provided my required investment return with the minimum risk.0 -

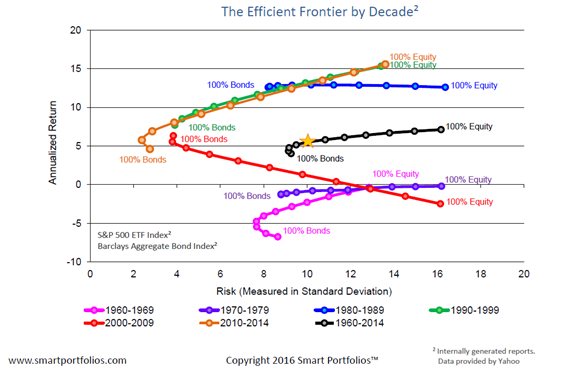

aroominyork wrote: »Would you kindly explain "historical efficient frontier"? Thanks.

If you plot the return against the risk of a set of portfolios (usually with different allocations to equity and fixed income) then the portfolios will generally fall within a parabola and the positively sloped section of that parabola is the efficient frontier.

A simple way to create an efficient portfolio is to diversify and reduce fixed costs by using index trackers. Here are several historical efficient frontiers that plot the return vs the risk parabola of portfolios made up of different percentages of S&P 500 Index and Barclays Aggregate Bond Index for several decades. “So we beat on, boats against the current, borne back ceaselessly into the past.”0

“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

You’re obsessed with crashes, and seem to live in fear of losing everything. You may not have the temperament for stock market investment. The "downside support" is the profit already made and yet to come, especially if you can continue to buy while stocks are cheap.

I still think you’re misunderstanding the American chart you posted earlier, which shows how much better equities perform than defensive investment. That said, as you’ve made clear, your priority is not growth but protection of capital. With that investment objective, your approach might be right. But most people here have more ambitious targets.

Also, most people here are definitely not young, inexperienced, idealistic punters as you surmised in an earlier post. I’m less than 5 years from retirement myself.

I am not overly concerned at the prospect of a crash, I do however consider risk in most things that I do , this rather than blindly charge into what is perceived to be the most profitable course of action, aka 100% equities.

Slowly but surely some posters are getting there on this point, we're now seeing the word diversification appear more more and more in positive terms, some are even mentioning diversification of asset classes for goodness sake. And let's not forget that VLS, the subject of this very thread, is typically a mixed asset product that comingles bonds (and other instruments) with equities, if that is not a case for asset class diversification, given the massive popularity of the product range, I don't know what is.

Finally on this subject of diversification and it takes us back to IFA's: does anyone really think that more than 0.05% of the UK IFA population would actually recommend 100% equities to any of their clients, in order to do that they would have to have sizeable wealth and a risk profile that is in the top 5% of risk tolerance. Perhaps it's worth thinking about why that is.

**paragraph removed by forum team**0 -

Here's one mans take on the cash vs shares issue albeit he doesn't show his workings, his findings and conlusions, however, are not what might be expected and challenge traditional conventions: https://www.theguardian.com/money/2016/jun/18/cash-trumps-shares-for-top-returns0

-

bostonerimus wrote: »People should have an asset mix that reduces the probability of them failing to meet their financial goals to an acceptable level. That asset mix is rarely 100% equities.

A home is the obvious key investment for most people. But if we ignore the home, then 100% equities (in the less volatile markets/sectors) is sensible for people more than 10 years from retirement. Assuming they have the stomach for it of course. Some will panic when the markets fall 30%, and sell up thereby crystallising the losses which would otherwise be recovered within a few years. I have no idea what proportion of people fit the panic profile. I have a cold analytical approach to these things (emotionally dead in some people's terms") ). 0

). 0 -

bostonerimus wrote: »A simple way to create an efficient portfolio is to diversify and reduce fixed costs by using index trackers.

Do you have proof of that statement?0 -

bostonerimus wrote: »We aren't going to agree about the ability of most people to pick consistent active winners. You might be one of those that does over 10, 20 or 30 years. I think the mathematics and the studies show that the highest probability for most people of meeting a specified investment return with the lowest risk is done with index funds.

I could believe that, however this forum is not really about 'most people'. It's about people with some investment savvy. I've met many people who fit your description i.e. they do not understand the markets, and passive investments would be by far the best choice.0 -

chiang_mai wrote: »Here's one mans take on the cash vs shares issue albeit he doesn't show his workings

His workings consisted of taking an extremely poor share investment (HSBC's FTSE 100 tracker, a poor choice of fund to track a poor choice of index) over an extremely poor period and comparing it with the very best possible cash investment (best-buy one year bonds).

For a more detailed rebuttal, see Abraham Okusanya's article.

As an academic exercise in showing that you can prove anything with statistics, it's quite interesting to see how you can contort the data to make cash outperform shares. As information to someone deciding their investment strategy it's completely useless. No-one who had the wherewithal to research the best-buy cash accounts on an ongoing basis would stick all their money in a FTSE 100 tracker (and an expensive HSBC one at that).

Paul Lewis is a bit of a standing joke. Getting energy and mobile companies to sort out incorrect bills is his comfort zone, whenever he delves into areas requiring an understanding of numbers he comes unstuck.

You're casting around the Internet for anyone who supports your theory that equities will lose money over the long term. That the best you can come up with is Paul Lewis should tell you something.0 -

You're not kidding, if his tweets are anything to go by he doesn't recommend pensions and his own retirement strategy seems to be mostly cash based. His objective research is often good but his opinions and conclusions are frequently weak (and highly partisan). Pick and choose carefullyI’m a keen listener to Lewis's shows, but he’s always been ultra-cautious about stock market investing, instead excitedly revealing news about new "high interest" bank accounts paying rates well below inflation.0 -

Nobody has answered the point regarding IFA advice, if 100% equities are such a great thing why aren't all IFA's recommending this as the prefered way forward for more/all clients. The fact is, hardly any IFA would recommend that as an approach, other than for extreme and exceptional clients.

IanMAnc - attack the post, not the poster, put forward constructive or informative counter arguments with supporting evidence if you wish - the idea is debate and different opinions, not borderline name calling!

Cash vs equities: it was a single article I came across, I don't know anything about the man et al. I thought it might be a useful item to post to try and stimulate debate on the subject and indeed it has. It might be a step too far to assume that a majority of people who invest, (as opposed to investors), buy into balanced diversified investments, I'm unsure on this point but I suspect it's so.

But yes I did read to the end of the article and what it also said was that equities also only win if the dividend is reinvested - why you think that bond (fund) investors wouldn't reinvest and that only equity investors would escape me!

VLS: I think it was pretty obvious that VLS for most readers here means a mixed asset product!

I think that equity diversification is fine and it's an admission that diversification is a positive strategy, where we seem to disagree is the extent to which diversification is good and it comes back to the risk-reward trade-off. If your age, risk profile and financial circumstances are such that you can fully tolerate all that 100% equities entails, good for you, go for it in the full knowledge of what it involves.

But it's arrogant if not borderline criminal, to imply that approach is suitable as a broad brush solution for a majority because, for all but the knowledgeable few, the approach will cost them money.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards