We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Why doesn't everyone just buy Vanguard LifeStrategy?

Comments

-

It is easy for an investor to hold the mixed equity you describe. Just buy a global equity tracker.

You seem very confused over the calculation of returns. Your table shows that small and mid cap returned on average about 9.6% per year. That takes into account crashes and recovery. It would have easily beaten your diversified fund over that time period. Sure, in some years it would have performed rather worse, but these were more than offset by it performing very much better in the good years.

Yes a tracker might do that. But of course the downside to a tracker is that when the index falls the tracker will also fall, there is no downside support, I think the purpose of a good portfolio is to not only generate good levels of profit but also to provide some protection to the downside, but that's just me.0 -

chiang_mai wrote: »Yes a tracker might do that. But of course the downside to a tracker is that when the index falls the tracker will also fall, there is no downside support, I think the purpose of a good portfolio is to not only generate good levels of profit but also to provide some protection to the downside, but that's just me.

We've tried to explain these fairly simple concepts to you, you really should understand investing a little better, but that's up to you.

This last post is a little better in that it acknowledges that you are after a risk adjusted return that manages volatility at the costs of some returns.

However you still fail to understand the concept that a higher risk, equity heavy portfolio will, in the vast majority of cases, outperform a more mixed and diversified portfolio including binds and potentially other assets.

Your reference in this thread, and others, to monitoring the performance of your portfolio over weeks or months is however still very concerning, investments should be made with a significant multi year if mot multi decade horizon, five years is often quoted as an absolute minimum and ten years ideally. These time periods offer the opportunity for recovery after any crashes, and monitoring iver shorter periods is futile really, particularly weeks or months, that's just noise.0 -

Possibly, but despite the volatility the average return on the FTSE100 over that time period with dividends re-invested was around 8%/year. What was the average return on cash?

In that link above, Paul Lewis uses the term "best buy cash". As far as I can tell he looked at the best possible one year fixed rate saving account for each year, and assumed the investor had moved all their cash into it.

.PaulLewisMoney wrote:Money invested in best buy cash over the whole 21 year period from 1 January 1995 to 1 January 2016 would have produced an average annual compound return of 5.0%. Over the same period the tracker would have produced a compound annual return of 6.0%. The 1% difference is far lower than the 3% to 8% typically quoted for the ‘risk premium’ of investing in shares.

The thing about cash, we know that it is going to hold its nominal value - even if its real value shrinks a little bit most years. We can't say the same about stocks, or about bond funds (unlike individual bonds bought at issue and held to maturity).

For me, this is an important consideration for investments held in ISAs. While I have no plans to spend the money in the short or medium term, it is possible that something may happen to change those plans, and I don't want to be nursing a 30% or 40% loss at that time.

If someone had to choose a starting point from which they might expect stocks to drop in value, they might choose a point at which the global economy was buoyant, and stock markets were at record highs.

If someone had to choose a starting point from which they might expect bonds to drop in value, they might choose a point at which interest rates were at record lows.

With equity markets at record highs, and interest rates at record lows- *maybe* we are at that point now- vulnerable to both equities and bonds falling, at the same time.0 -

chiang_mai wrote: »Yes a tracker might do that. But of course the downside to a tracker is that when the index falls the tracker will also fall, there is no downside support, I think the purpose of a good portfolio is to not only generate good levels of profit but also to provide some protection to the downside, but that's just me.

You’re obsessed with crashes, and seem to live in fear of losing everything. You may not have the temperament for stock market investment. The "downside support" is the profit already made and yet to come, especially if you can continue to buy while stocks are cheap.

I still think you’re misunderstanding the American chart you posted earlier, which shows how much better equities perform than defensive investment. That said, as you’ve made clear, your priority is not growth but protection of capital. With that investment objective, your approach might be right. But most people here have more ambitious targets.

Also, most people here are definitely not young, inexperienced, idealistic punters as you surmised in an earlier post. I’m less than 5 years from retirement myself."I don't mind if a chap talks rot. But I really must draw the line at utter rot." - PG Wodehouse0 -

I think that's why its important to keep a decent cash buffer.Ray_Singh-Blue wrote: »While I have no plans to spend the money in the short or medium term, it is possible that something may happen to change those plans, and I don't want to be nursing a 30% or 40% loss at that time.0 -

Ray_Singh-Blue wrote: »In that link above, Paul Lewis uses the term "best buy cash". As far as I can tell he looked at the best possible one year fixed rate saving account for each year, and assumed the investor had moved all their cash into it.

.

The thing about cash, we know that it is going to hold its nominal value - even if its real value shrinks a little bit most years. We can't say the same about stocks, or about bond funds (unlike individual bonds bought at issue and held to maturity).

For me, this is an important consideration for investments held in ISAs. While I have no plans to spend the money in the short or medium term, it is possible that something may happen to change those plans, and I don't want to be nursing a 30% or 40% loss at that time.

If someone had to choose a starting point from which they might expect stocks to drop in value, they might choose a point at which the global economy was buoyant, and stock markets were at record highs.

If someone had to choose a starting point from which they might expect bonds to drop in value, they might choose a point at which interest rates were at record lows.

With equity markets at record highs, and interest rates at record lows- *maybe* we are at that point now- vulnerable to both equities and bonds falling, at the same time.

Morning! Was it you who was saying that you are investing to pay your mortgage off? And that you'd reached the halfway point and was wondering whether to pay off half now or risk a crash and keep going to pay it all off?

Apologies if this makes no sense as I mis-remembering. I was just wondering you you (or the person in question) decided to do in the end.0 -

chiang_mai wrote: »I'm talking about consistency of returns over the twenty years shown.

I can agree with this, or at least I can agree with this reading of the last 20 years of returns. However I'm not so sure that I buy into the future performance of bonds as providing a suitable buffer to help with smoothing, and there is definitely nothing in the grid that shows any assistance to your previous comments about people losing out if they were holding a 100% forever equity position.

At the end of the day it's up to every individual investor to decide on what they need from their portfolio. So if someone prefers a smoother ride then that is fine for them, but if they are investing for the long-term then they must accept that the likelihood is that they are giving up performance by moving away from a 100% diverse equity position. It's only once they move to a shorter term investing horizon that bonds etc can be a valuable component to guard against any dips that they do not have time to recover from.0 -

But if they decide what they need from their portfolio is the sort of returns that you can get from a 60/40 equity/bond portfolio longer term, there is no need for them to have to accept the volatility of 100% equities.At the end of the day it's up to every individual investor to decide on what they need from their portfolio. So if someone prefers a smoother ride then that is fine for them, but if they are investing for the long-term then they must accept that the likelihood is that they are giving up performance by moving away from a 100% diverse equity position. It's only once they move to a shorter term investing horizon that bonds etc can be a valuable component to guard against any dips that they do not have time to recover from.0 -

Morning! Was it you who was saying that you are investing to pay your mortgage off? And that you'd reached the halfway point and was wondering whether to pay off half now or risk a crash and keep going to pay it all off?

Apologies if this makes no sense as I mis-remembering. I was just wondering you you (or the person in question) decided to do in the end.

Hi & yep, that's me.

My plan is to stay the course I have chosen, essentially 50% equities and 50% cash, and see where that leads.

I prefer cash to bonds for the reasons given above. Which is why I don't hold any lifestrategy funds, although keep an eye on VLS60 as a performance benchmark.0 -

But if they decide what they need from their portfolio is the sort of returns that you can get from a 60/40 equity/bond portfolio longer term, there is no need for them to have to accept the volatility of 100% equities.

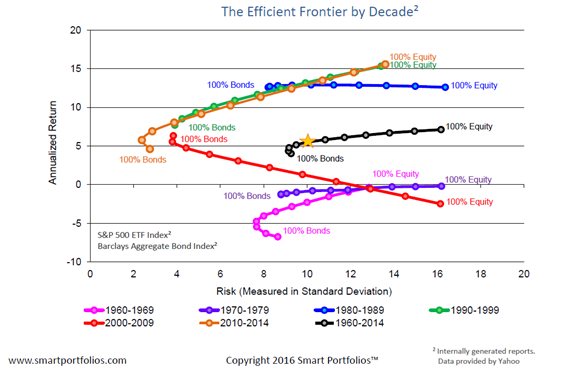

Historically 60/40 has been the classic mix of risk and return. That might not be the case over the next decade with such low Gilt and Treasury returns, but I have only guesses about what might happen over the longer term. So for all but the oldest and most risk averse I'd say that a 60% equity allocation is probably as low as they should go. Also maybe a little reading about efficient frontiers and contemplation of the enclosed graph might be useful for people interested in this discussion. Of course how people react to market volatility is also very important which is where discipline and a strong stomach are required. “So we beat on, boats against the current, borne back ceaselessly into the past.”0

“So we beat on, boats against the current, borne back ceaselessly into the past.”0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards