We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Why doesn't everyone just buy Vanguard LifeStrategy?

Comments

-

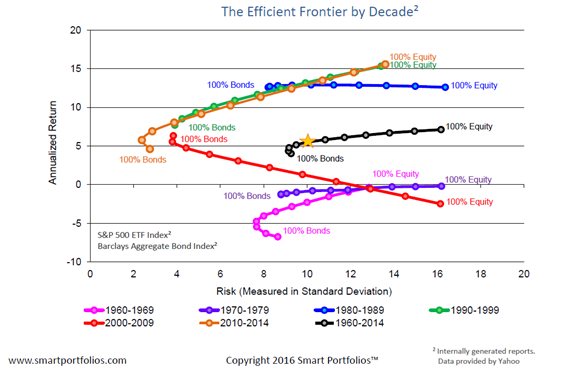

bostonerimus wrote: »If you plot the return against the risk of a set of portfolios (usually with different allocations to equity and fixed income) then the portfolios will generally fall within a parabola and the positively sloped section of that parabola is the efficient frontier.

A simple way to create an efficient portfolio is to diversify and reduce fixed costs by using index trackers. Here are several historical efficient frontiers that plot the return vs the risk parabola of portfolios made up of different percentages of S&P 500 Index and Barclays Aggregate Bond Index for several decades.

That's an excellent visual.0 -

chiang_mai wrote: »Nobody has answered the point regarding IFA advice, if 100% equities are such a great thing why aren't all IFA's recommending this as the prefered way forward for more/all clients. The fact is, hardly any IFA would recommend that as an approach, other than for extreme and exceptional clients.

IanMAnc - attack the post, not the poster, put forward constructive or informative counter arguments with supporting evidence if you wish - the idea is debate and different opinions, not borderline name calling!

Cash vs equities: it was a single article I came across, I don't know anything about the man et al. I thought it might be a useful item to post to try and stimulate debate on the subject and indeed it has. It might be a step too far to assume that a majority of people who invest, (as opposed to investors), buy into balanced diversified investments, I'm unsure on this point but I suspect it's so.

But yes I did read to the end of the article and what it also said was that equities also only win if the dividend is reinvested - why you think that bond (fund) investors wouldn't reinvest and that only equity investors would escape me!

VLS: I think it was pretty obvious that VLS for most readers here means a mixed asset product!

I think that equity diversification is fine and it's an admission that diversification is a positive strategy, where we seem to disagree is the extent to which diversification is good and it comes back to the risk-reward trade-off. If your age, risk profile and financial circumstances are such that you can fully tolerate all that 100% equities entails, good for you, go for it in the full knowledge of what it involves. But it's arrogant if not borderline criminal, to suggest that approach as a broad brush solution because for all but the knowledgeable few the approach it will cost them money.

So you've changed your argument from your assertion that a mixed equity bond fund will outperform a pure equity investment, it would be nice to have some consistency.

You've also acknowledged that for many a pure equity approach is high risk, which is true for much of the population, however on these boards you are dealing with people with a little more knowledge and experience in general.

Many people may not have the stomach for volatility, but that doesn't mean they will be better off with a lower risk strategy. For example someone in their twenties would be encouraged to be 100% equity in their pension, as the returns from 40 years of contributions will almost certainly be higher than from including bonds, it's pretty much that simple.

The official reason for IFAs not proposing 100% equity is that the average person has a medium risk attitude and couldn't stomach the volatility; a real reason might be that the IFA is far less likely to get into trouble and be subject to redress if he invests below someone's risk profile than above it. For example we've had plenty of mis selling scandals, and in many of these cases a product has been confirmed as mis sold, but there has been no redress as that product has significantly outperformed the product that would have been more appropriate, maybe the client should have had to pay the excess back?0 -

I'll take Markowitz's word for it. Seriously, diversification and cost control are simple ways to increase return for a given risk in Modern Portfolio Theory. If you can get more return for the same risk by consistently choosing high performing active funds then that would be a more efficient portfolio.BananaRepublic wrote: »Do you have proof of that statement?“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

I recently left IFAs and started self investing for two reasons. First, I realised their in-house constructed portfolios did not perform well. Secondly, and to answer your question, because they err on the side of caution so that when the market dips they do not have endless worried clients on the phone. My experience of the way they assess your risk tolerance is disingenuous. They have questionnaires asking questions such as how concerned you would be about the value of your portfolio falling, but with no reference to your age and hence eg the likelihood of it recovering. So for inexperienced investors who do not understand the short term and long term patterns of the stock market, a 30 year old and a 55 year old might give similar answers and be allocated to similar portfolios.chiang_mai wrote: »Nobody has answered the point regarding IFA advice, if 100% equities are such a great thing why aren't all IFA's recommending this as the prefered way forward for more/all clients.

I know IFAs on this forum will say the questionnaires should only be one element of the analysis, but my experience is that IFAs rely on it hugely and then push their clients towards overly ‘safe ‘ investments.0 -

BananaRepublic wrote: »An IFA will determine the client's risk profile, and advise on that basis. Thus someone with a high risk tolerance would be 100% equities, someone who spends all day clinging to a scruffy piece of fabric and sucking their thumb would be 0% equities.

Ironically an infant with a bare trust investment is one of the few clients to whom an IFA might recommend a 100% equity portfolio, because

a) they have a 15+ year investment horizon

b) as they can't spend the money, even if they really want to, their capacity for loss (meaning recoverable, short-term losses) is 100%

c) they aren't going to ring the IFA up in a panic on their Fisher-Price Farm Animal Sounds phone wanting to sell everything during a crash.

100% equities is pretty exceptional nowadays, even for high risk investors, because a cornerstone of Modern Portfolio Theory is that by introducing a small proportion of bonds and other alternative asset classes, such as commercial property, you get a significant reduction in volatility with a negligible reduction in potential returns.

Ten years ago when IFAs were more likely to come from a sales background and not an economics background, fund choices tended to be less scientific and more likely to be 50% In-House UK Equity Fund 50% In-House International Equity Fund or along those lines.0 -

bostonerimus wrote: »I'll take Markowitz's word for it. Seriously, diversification and cost control are simple ways to increase return for a given risk in Modern Portfolio Theory. If you can get more return for the same risk by consistently choosing high performing active funds then that would be a more efficient portfolio.

I read from another of your posts that you are in the US, and I believe that for the US market tracker funds are 'better' than active ones, and hence your statement would be true. But apply it to other markets, well I'd like to see a link to some proof.0 -

A bottle of lao khao would probably suffice

") 0

0 -

BananaRepublic wrote: »I read from another of your posts that you are in the US, and I believe that for the US market tracker funds are 'better' than active ones, and hence your statement would be true. But apply it to other markets, well I'd like to see a link to some proof.

I'm not making an argument that distinguishes between active and passive funds.

Whether passive or active funds are "better" will be long debated on here and I'm sure you can easily google the many US and recent UK studies that compare the returns of the two approaches. Modern Portfolio Theory and historical efficient frontiers can be applied to come up with an asset allocation whether you are using diversified active or passive funds. For the purposes of this discussion I am just highlighting the efficient frontier for different proportions of equites and fixed income however you choose to invest. if you think you can get a better return for the same risk with an active portfolio rather than a passive one then you should use active funds. However the same principles of asset allocation on the efficient frontier apply.“So we beat on, boats against the current, borne back ceaselessly into the past.”0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards