We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Cash ISAs: The Best Currently Available List

Comments

-

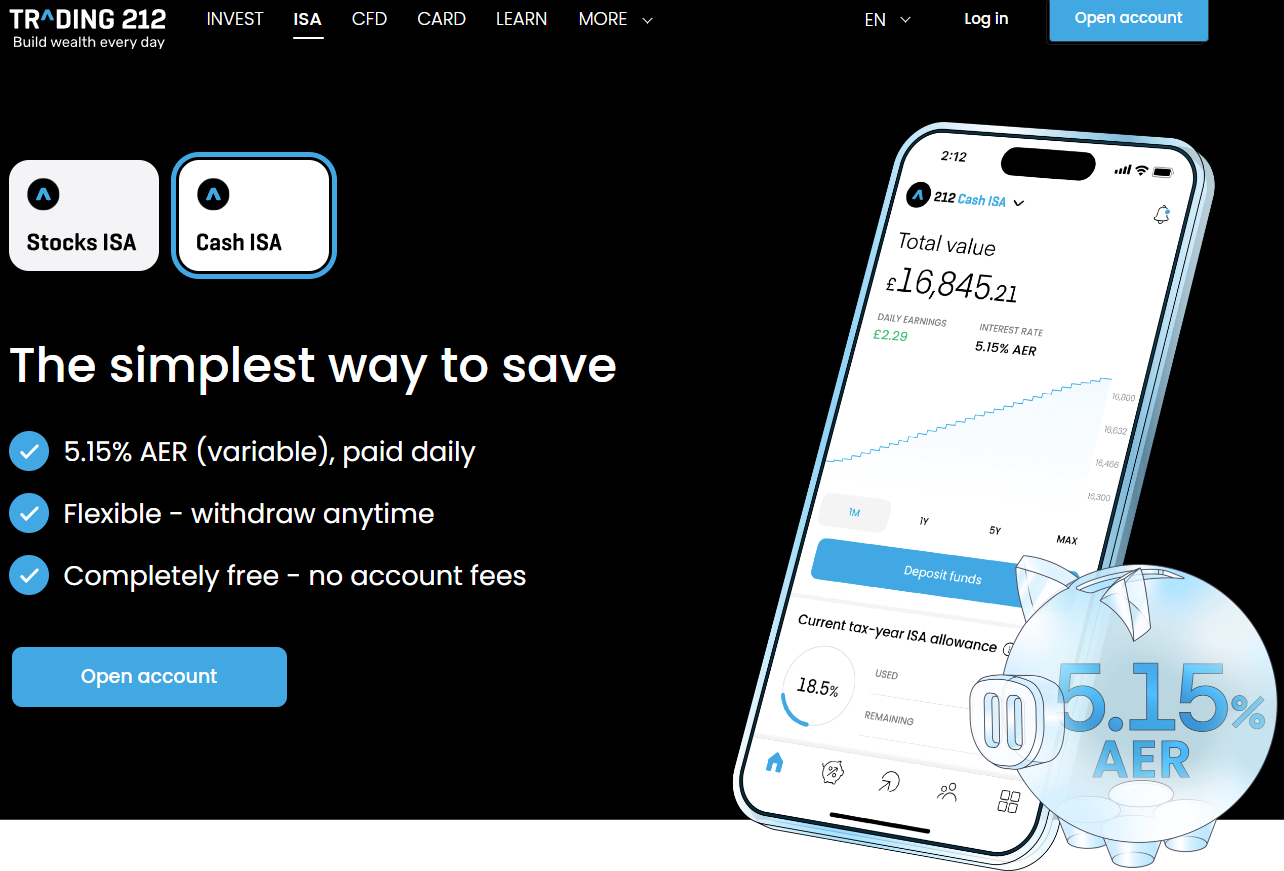

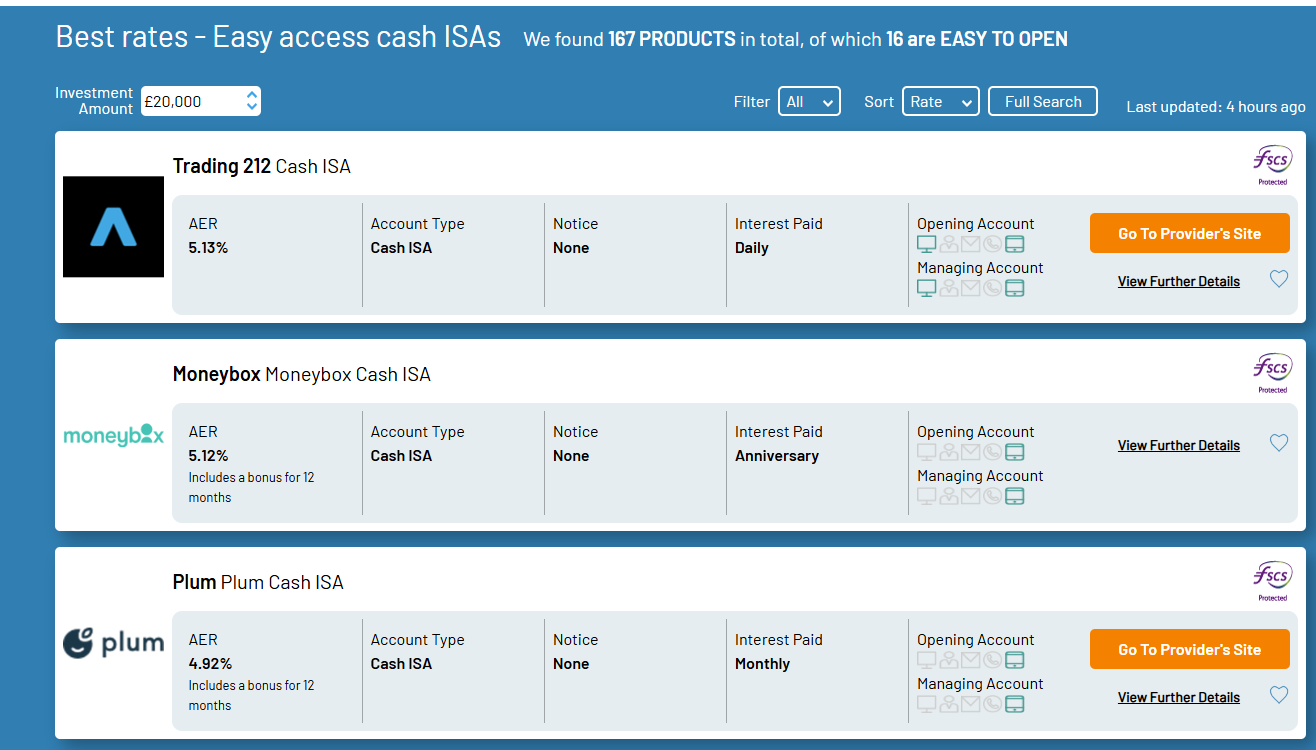

gt94sss2 said:Trading 212 has increased the interest rate on GBP balances to 5.15% AER

Trading website shows 5.15% indeed.Bridlington1 said:

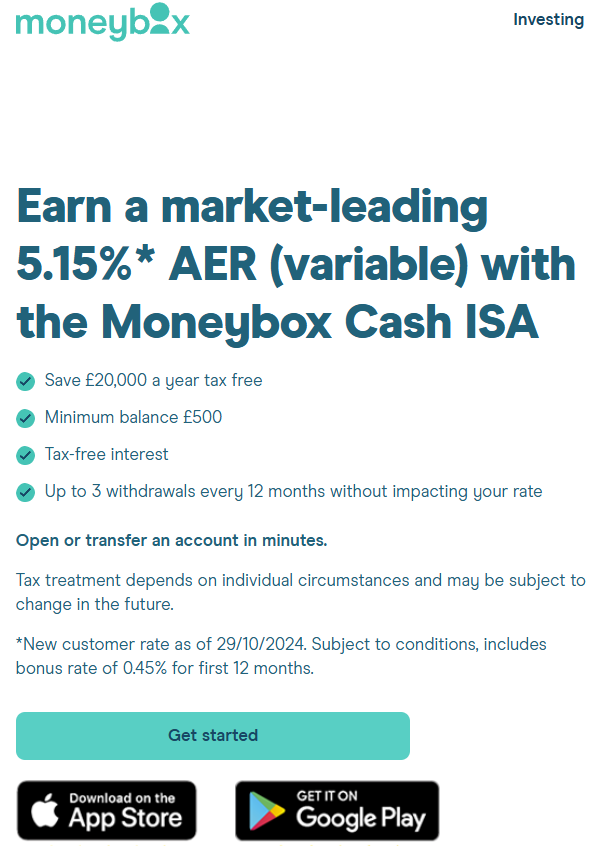

Along with Moneybox, who have matched the rate.gt94sss2 said:Trading 212 has increased the interest rate on GBP balances to 5.15% AER

Moneyfacts shows the below and has so catching up to do

Trading212 interest change history:Interest changes 25th May 2024* 5.07% 5.2% AER 9th September 2024 4.88% 5.0% AER 16th September 2024 4.93% 5.05% AER 17th September 2024 4.975% 5.1% AER 29th October 2024 5.02% 5.15% AER

*Rate was at that level before but I captured the rate on the day the Cash ISA was opened

4 -

Excellent. T212's willingness to nudge the rate up to be at the top of the table - at a time of savings rates generally declining - is the account's best feature.0

-

How long will it last with the BOE expected to drop the base rate on the 7th Novdlevene said:Excellent. T212's willingness to nudge the rate up to be at the top of the table - at a time of savings rates generally declining - is the account's best feature.0 -

Trading not directly lowered rates last time and gave around 10-12 days notice, for Euro rates it is even more notice just now (dropping on 1st November). So if rates go don on 7th we may be lucky to get the rate until around mid November or beyond.Johnny-Cage said:

How long will it last with the BOE expected to drop the base rate on the 7th Novdlevene said:Excellent. T212's willingness to nudge the rate up to be at the top of the table - at a time of savings rates generally declining - is the account's best feature.2 -

It gives the impression of an institution that wishes to stay top of the best buy tables which is encouraging given I'll likely put my whole year isa allowance in there.pecunianonolet said:

Trading not directly lowered rates last time and gave around 10-12 days notice, for Euro rates it is even more notice just now (dropping on 1st November). So if rates go don on 7th we may be lucky to get the rate until around mid November or beyond.Johnny-Cage said:

How long will it last with the BOE expected to drop the base rate on the 7th Novdlevene said:Excellent. T212's willingness to nudge the rate up to be at the top of the table - at a time of savings rates generally declining - is the account's best feature.0 -

Investors Chronicle:

The government will freeze allowances for Isas, Lifetime Isas and Junior Isas at their current levels until 2030, in a blow to investors. Annual limits on the trio will remain at £20,000, £4,000 and £9,000 respectively. Labour also confirmed it would not go ahead with the £5,000 British Isa allowance, to solely invest in domestic shares, as proposed by the last Tory government.

A 'blow' would've been a reduction!

Edit: Apologies, already being discussed here:

ISA changes (or lack of changes) in the Autumn 2024 budget — MoneySavingExpert Forum3 -

Agree, a blow would have been a reduction or any other change so welcome news that nothing is changing (for now and until the next budget). How many "working people" can fill year after year their 20k ISA allowance anyway. Luckily, I am in that camp now, when 5 years ago this was unthinkable.mebu60 said:Investors Chronicle:

The government will freeze allowances for Isas, Lifetime Isas and Junior Isas at their current levels until 2030, in a blow to investors. Annual limits on the trio will remain at £20,000, £4,000 and £9,000 respectively. Labour also confirmed it would not go ahead with the £5,000 British Isa allowance, to solely invest in domestic shares, as proposed by the last Tory government.

A 'blow' would've been a reduction!0 -

This is the 8th year in a row at £20k and we can look forward to another 5 years or more at that level. Of course this is an annual allowance and the amount held in ISA continues to grow and grow. It'll be a trillion pounds soon.mebu60 said:Investors Chronicle:

The government will freeze allowances for Isas, Lifetime Isas and Junior Isas at their current levels until 2030, in a blow to investors. Annual limits on the trio will remain at £20,000, £4,000 and £9,000 respectively. Labour also confirmed it would not go ahead with the £5,000 British Isa allowance, to solely invest in domestic shares, as proposed by the last Tory government.

A 'blow' would've been a reduction!

Edit: Apologies, already being discussed here:

ISA changes (or lack of changes) in the Autumn 2024 budget — MoneySavingExpert Forum0 -

@Kazza242

Virgin Money Easy Access Cash ISA Exclusive (issue 2) - 4.76%

Has been replaced with Issue 3 paying 4.51%0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards