We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Early-retirement wannabe

Comments

-

Update on our retirement plans now that we have both turned 48. I had expected both my wife and myself to be retired by now, but it is dragging on, we don't even have agreed last day of service or signed exit agreements yet although I expect that to happen soon. The most likely scenario is that I leave at the end of April and my wife leaves a month or two after that.

No children, but we added a rescue dog to our household in December. He is a 3.5 year old Huskamute (Alaskan Malamute / Husky cross), who weighs 31kg and needs to get up to about 35kg, so quite a big dog.

Current assets (excl pension)

Our net non-pension assets at the moment are shown below.

High-level summary

House

£733,000

Investment ISA

£275,000

Cash/near cash net of all debt

-£78,000

The reason for the large negative cash balance is due to £87,000 of 0% borrowing on credit cards and provision for tax liabilities. The house is undervalued, as I just track purchase price against price change in the area for s/s purposes so all the recent refurbishments I have made are effectively valued at zero. However, the actual value of the house is of little significance, it might well provide some extra funds in the dim and distant future but that is not worth factoring in, except as assurance that our very old age will be well-provisioned and we won't be at the mercy of the State.

I have our offset mortgage in place, fully offset, which is enabling all higher rate income to be put into a pension. I will be a higher-rate taxpayer in all years after age 55, but my wife shouldn't be a higher rate taxpayer until she reaches State Pension age. In due course, we will draw from the offset savings account in the years before age 55, and then replenish it at age 55 from tax-free lump sum. That means money that would otherwise be taxed at 40% will be taxed at 30% when drawn from the pension for me (40% tax, with 25% tax free) and 15% for my wife.

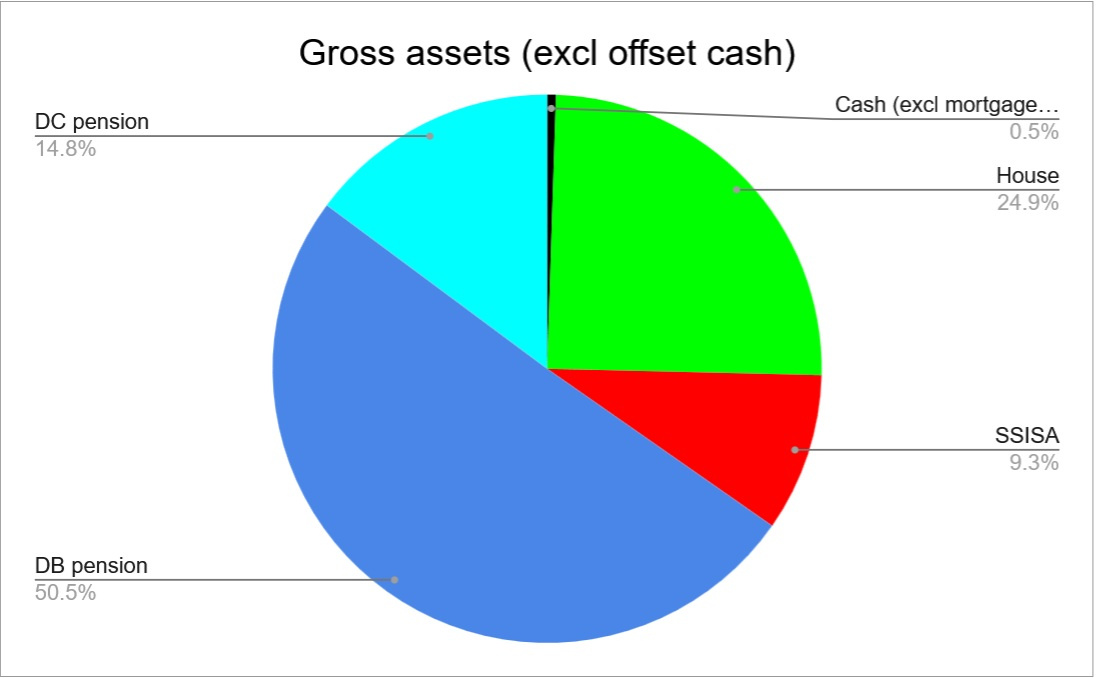

Across all our assets, the distribution (using CETV for DB pension and ignoring State Pension) is:

Invested funds are reasonably cautious, taken across all wrappers they are 50% equity, 40% bonds, 5% gold, 5% other. Once we actually leave employment I will probably increase our cash holdings in cash ISAs, perhaps even transferring all the investment ISA given I expect to use all of that within the next 7 years.

Income from leaving employment and future income

Between now and when we leave employment, we expect to receive £160,000 in cash (after tax) and £90,000 into DC pension as a combination of salary and exit payments.

On the pension front, based on the post April rates, we will have pre-tax annual income from our Defined Benefits and State Pension after State Pension age of a bit over £90,000 p/a and a net income of a bit over £77,000 based on today's income tax rates and thresholds. We will draw our DB pensions from age 55 and use DC pension to top them up such that we also have net income of a bit over £77,000 after tax in all years from age 55. This assumes DC pension increases by CPI, on top of fees (for ease of calculation - that is cautious, but fiscal drag will hurt and that isn't in the forecast either so they will offset).

The amount of DC we need to top-up DB income, and to also make Class 3 State Pension contributions, is £314,000 (after tax) and currently our DC pots total £413,000.

Taking into account the remaining cash and pension payments from employment, we should have about £120,000 (after tax) spare in the DC pensions to use to replenish the mortgage offset savings account at age 55, ie, those funds can be drawn from the offset savings account prior to age 55.

Using the cash from leaving employment along with our investment ISA and paying off all debt, we have £54,000 p/a to age 55. Using the spare pension cash via the mortgage offset savings account boosts that to £72,000 p/a to age 55. So income from retirement to death is pretty well smoothed out.

Expenditure

I've spent the last year carefully monitoring our predictable regular expenditure, which looks like this. The electric bill includes electric car charging.

Annual

House bills, incl regular maintenance

£4,553

Council tax and green waste

£4,021

Pet costs (insurance, food, vet)

£1,375

Club memberships (running, rambling, concert band, leisure centre)

£1,087

Car bills (Insurance, VED, MoT, Breakdown, Service, Cleaning)

£680

Medical (Contact lenses, dental, and eye checks)

£610

Other (Mobile phones, VPN, password manager, haircuts, presents)

£571

Total

£12,896

That excludes food, clothes, travel and holidays, car and house repairs, entertainment, and capital spend. In preparation for retirement, we bought a new car last year and after moving house we refurbished the house that now has a new roof, new windows, new doors, new consumer unit, new boiler, a new kitchen and bathrooms, was fully landscaped outside, and fully decorated inside. Hopefully, capital expenditure should be low in the next few years (ie until we both reach age 55 in 2032).

The delay in leaving employment has been quite welcome up to now, as it has given a nice little boost to resources after spending more than expected on our new home and refurbishment. However, we already have more than I can ever see us needing once the exit payments are factored in, so it is all getting a bit frustrating now, and it would be great if we could wrap everything up and both leave before the summer.

12 -

nice dog. Our costs a lot more than that per year but he is old now - the insurance alone is £128 pcm

I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.3 -

Didn't the govt announce plans to limit cash ISAs?

I think....0 -

There will be a ban on transfers from investment ISAs to cash ISAs to apply from April 2027, I'd do any transfers before then.

Before I did all the house purchase and refurbishments, I transferred ISA savings into a flexible ISA before withdrawal, then preserved the flexible balance by topping-up from the offset mortgage each year at the start of April and moving the money back at the start of the tax year. That maintained the flexible balance for the cost of a trivial amount of mortgage interest. That means we are able to deposit a bit over £210,000 into cash ISAs in 2025/26, and although I won't deposit anything more into cash ISAs this tax year, I will again preserve the flexible amount by moving mortgage offset savings in April 2026. So although contribution limits drop to £12,000 per person per year from April 2027, I'll be able to drop a quarter of a million (!) of new money into cash ISAs in 2026/27. That will take care of all of the cash from the exit payments with a lot of room left over.

I plan to carry on preserving the unused flexible balance using the offset savings each year to age 55, which should then enable me to drop a lot of tax-free pension cash into ISAs if I want to, given ISAs are probably lower policy change risk than pensions. It does seem perverse that this is an option, when new savers can only put £12,000 into cash, but those are the rules of the game.

0 -

I'm playing exactly the same game, have done for a few years and intend to continue which would allow me to deposit tfls from pension into isa if I choose, no other reason. As I'm over 55 I could do it now, not sue if there is a reason not to?

0 -

Good strategy and if the rate on your offset is higher that the rate on the flex ISA then it makes sense. However if you can get a higher rate on a (non flexible) isa than you are paying on the mortgage then perhaps you should be stoozing the mortgage instead?!

I think....0 -

Quote from hugheskevi: " That means we are able to deposit a bit over £210,000 into cash ISAs in 2025/26, and although I won't deposit anything more into cash ISAs this tax year, I will again preserve the flexible amount by moving mortgage offset savings in April 2026. So although contribution limits drop to £12,000 per person per year from April 2027, I'll be able to drop a quarter of a million (!) of new money into cash ISAs in 2026/27. That will take care of all of the cash from the exit payments with a lot of room left over. "

I'm not seeing the gain here over just leaving the cash ISA alone and dropping the pension TFC direct into offset mortgage savings ? Doesn't it end up the same ?

0 -

I'm playing exactly the same game, have done for a few years and intend to continue which would allow me to deposit tfls from pension into isa if I choose, no other reason. As I'm over 55 I could do it now, not sure if there is a reason not to?

I don't think there is any reason not to, but equally there may not be much reason in doing so. Having a large flexible ISA balance is useful if there might be unexpected future income, eg, inheritance, redundancy, or something like that. If those things have all been exhausted then it probably has little value, so no harm in shoving a pension tax free lump sum into it if desired.

Good strategy and if the rate on your offset is higher that the rate on the flex ISA then it makes sense. However if you can get a higher rate on a (non flexible) isa than you are paying on the mortgage then perhaps you should be stoozing the mortgage instead?!

It isn't about interest rates and arbitrage, it is about the option value of preserving a large flexible ISA contribution limit. There is a very small interest cost to be paid due to using the money in the offset savings account to preserve the flexible ISA contribution limit, but that is well worth it for the future option value it provides.

As I always intended to fully offset the mortgage from the start, it is a very uncompetitive rate as I preferred to have a fee-free mortgage. In about 5 years time when I might start to draw from the offset savings account for day-to-day living, I hope to be able to change mortgage type to something much more competitive and for a much lower amount (using funds in the offset account to reduce the balance considerably), probably with a fixed term until just after I am 55, and then probably fully repay mortgage from pension at the end of the term.

Quote from hugheskevi: " That means we are able to deposit a bit over £210,000 into cash ISAs in 2025/26, and although I won't deposit anything more into cash ISAs this tax year, I will again preserve the flexible amount by moving mortgage offset savings in April 2026. So although contribution limits drop to £12,000 per person per year from April 2027, I'll be able to drop a quarter of a million (!) of new money into cash ISAs in 2026/27. That will take care of all of the cash from the exit payments with a lot of room left over. "

I'm not seeing the gain here over just leaving the cash ISA alone and dropping the pension TFC direct into offset mortgage savings ? Doesn't it end up the same ?

Right now, there is no cash ISA balance, that was all used in the past to buy and refurbish our current house. There is just a big mortgage and an equally big mortgage offset savings acccount. There is also a flexible ISA contribution limit of £210,000 on the cash ISA, with another £40,000 that will be added to that for 26/27 across my wife and myself. Hence when we get paid redundancy that can all go straight into the cash ISA due to having preserved the flexible ISA contribution limit by temporary deposits into the cash ISA in early April each year from the offset savings account, and then returning them at the start of tax year.

As the mortgage offset savings is already fully offset, any further cash into that would get 0% interest.

So the offset savings account is just a big pile of low-interest liquidity, which can conveniently be used to preserve a high flexible cash ISA contribution amount for future use. Then in future years it will serve its main purpose of being low interest borrowing to be repaid from tax advantaged pension a few years later.

2 -

@hugheskevi who is the flexible cash ISA with? The only flexible ISAs I can find are S&S like Trading 212, Fidelity, Barclays and Freetrade. I cannot seem to find any cash ones, though i guess money market funds in the S&S ones might work, at least until April 2027.

Thanks.0 -

Trading 212s cash one is flexible - possibly not the best rate though.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards