We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Early-retirement wannabe

Comments

-

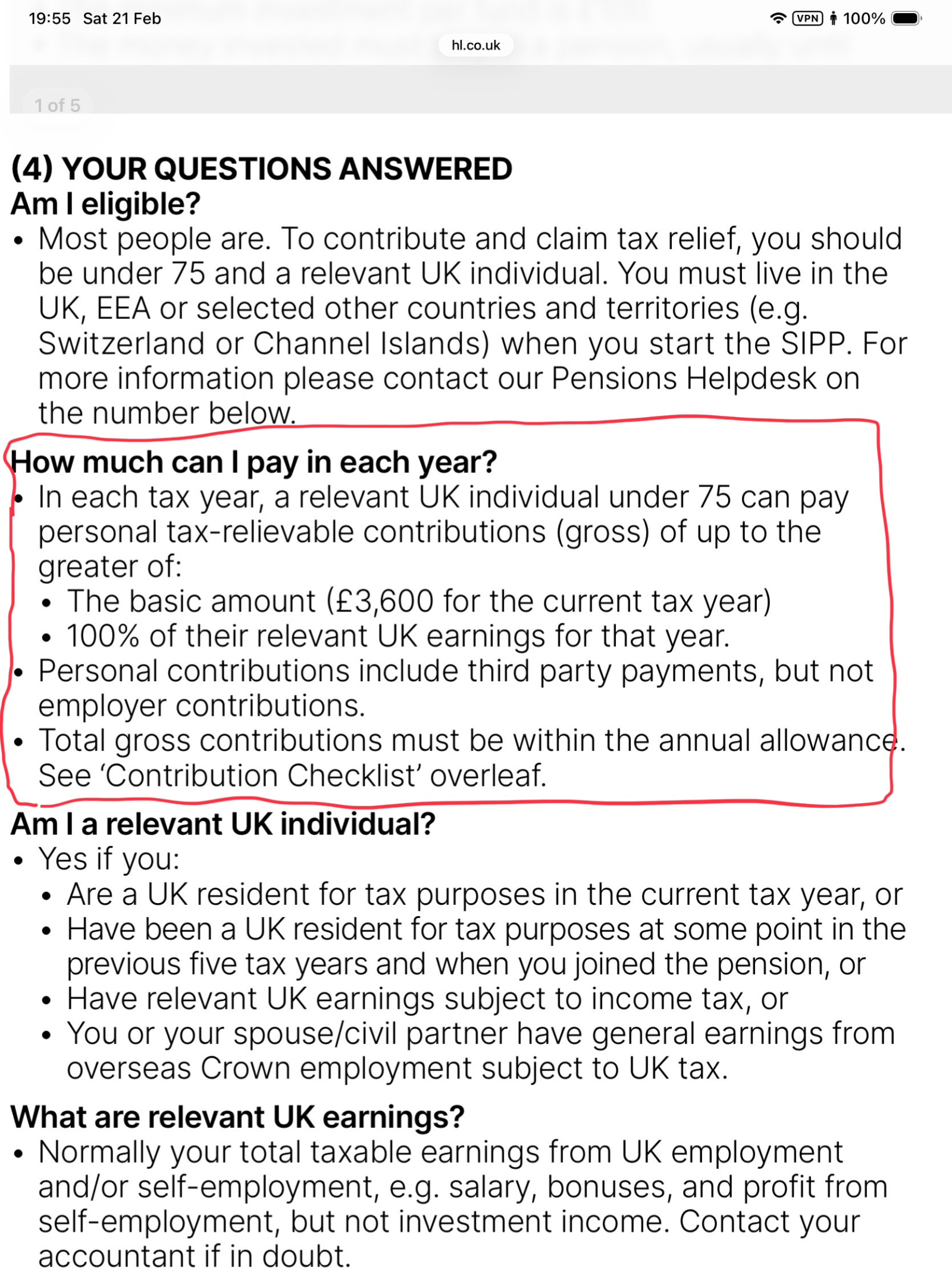

when you contribute to a pension you are asked questions like 'do you have sufficient earned income to support this contribution' and 'are you limited to £10k as a result of triggering the MPAA by drawing down any taxable income from a DC pension'. If you have no earned relevant income then you are not supposed to contribute more than £3600. You certainly cannot get tax relief on anything above £3600 if you haven't earned anything in the tax year.

I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.2 -

I hope you read this HL page, and especially the bit:

You'll only get tax relief on personal pension contributions up to 100% of your UK earnings, or £3,600 if this is greater (if you're a low or non-earner).

HL automatically claims basic rate relief on contributions from HMRC, and also shares information on contributions with HMRC.

HMRC will match all the information against an individual's tax records. Your case would be a fairly blatant outlier being a big contribution for an older individual with only pension income being taxed, so should be picked up relatively soon, but it may well take HMRC several months into 26/27 before it gets picked up. It could potentially take a lot longer - just this week I have been dealing with a case that HMRC plan to impose interest on relating to pension tax issues dating back to 2019/20, which they seem to have only recently identified.

If you do as QrizB suggests, then it may well be able to be unwound. If you wait to see if HMRC catch you or not, you are running a far greater risk. Probably HMRC will consider it a mistake and simply reclaim the tax relief above the amount due on a £3,600 contribution, but they could consider it careless and impose interest and even potentially penalties.

4 -

Correct, my property is in Trust set up by my late Dad. It passes down his family line. No inheritance tax I believe! My statement applies if it were not.

I will take your advice and contact HL. I will post their response.

3 -

Correct, my property is in Trust set up by my late Dad. It passes down his family line. No inheritance tax I believe!

I've not taken much interest in trusts but isn't there tax to pay every 10 years? The trustees should be dealing with this for you.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.1 -

@Top_of_the_Stocks you say you could sell your house for £325000. In that cases you and your spouse would need a further £675000 in your estate to fall within the scope of inheritance tax (assuming no other gifts or allowances are used). Sometimes trying to save a few bob from the tax man can cost a lot more in the long run.

2 -

Thank you to all above.

I have queried this with HL and they are are sending me a form to sign for the repayment of the excess tax claimed.

I have lodged a complaint that this sort of claim should be checked by them as they are doing the claiming on my behalf.

If there was tax to pay on a investment income I am sure they would be on the ball.

I am not to unhappy at my mistake. I am treating it as a short term interest free loan. I have made nearly £4k profit and I still get to keep £800 of the claim for the wife and I.

Thanks again

5 -

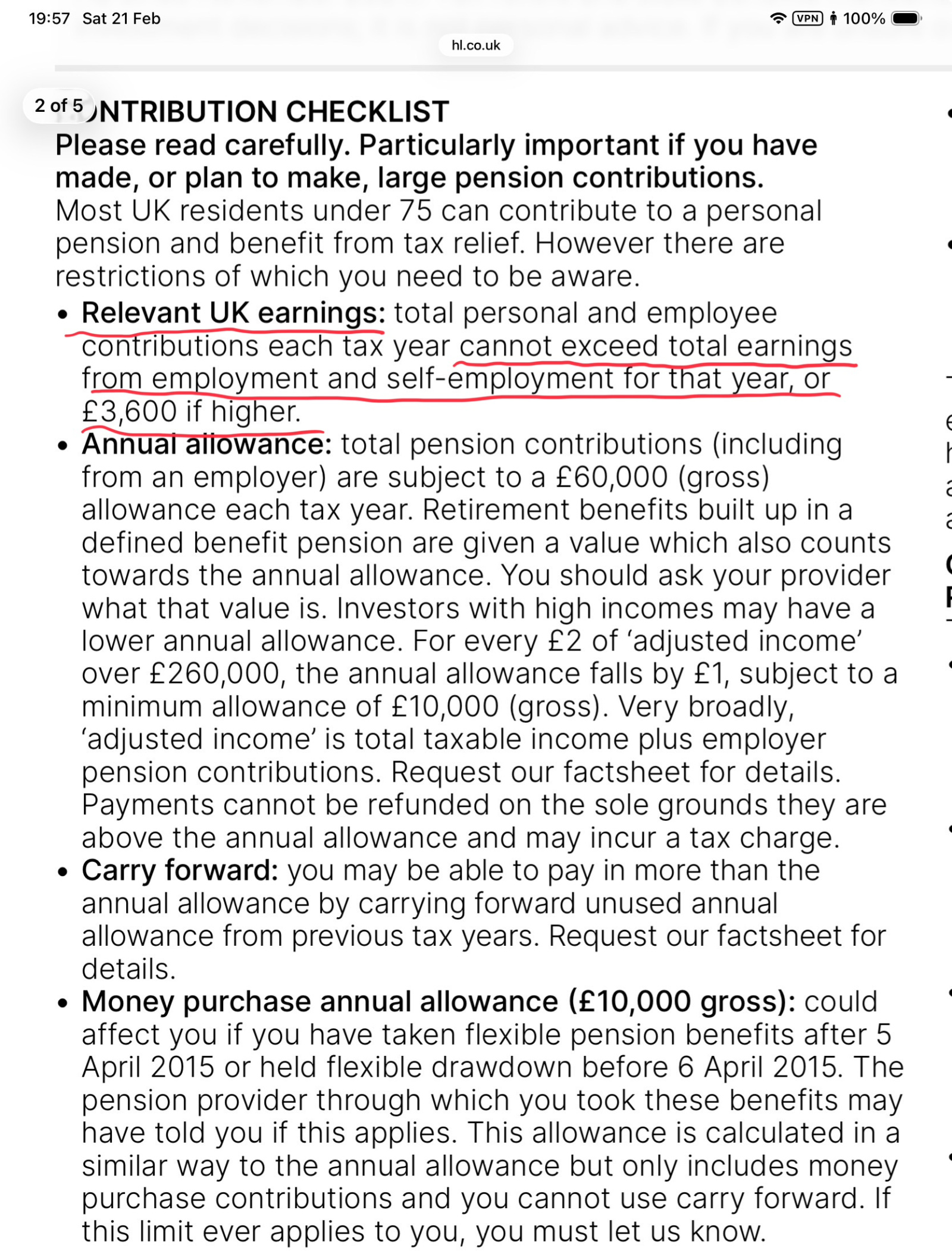

I don’t think it’s HL at fault here as the information provided when you pay a contribution does show the maximum allowed

However if they are helping you unwind it then all is well.

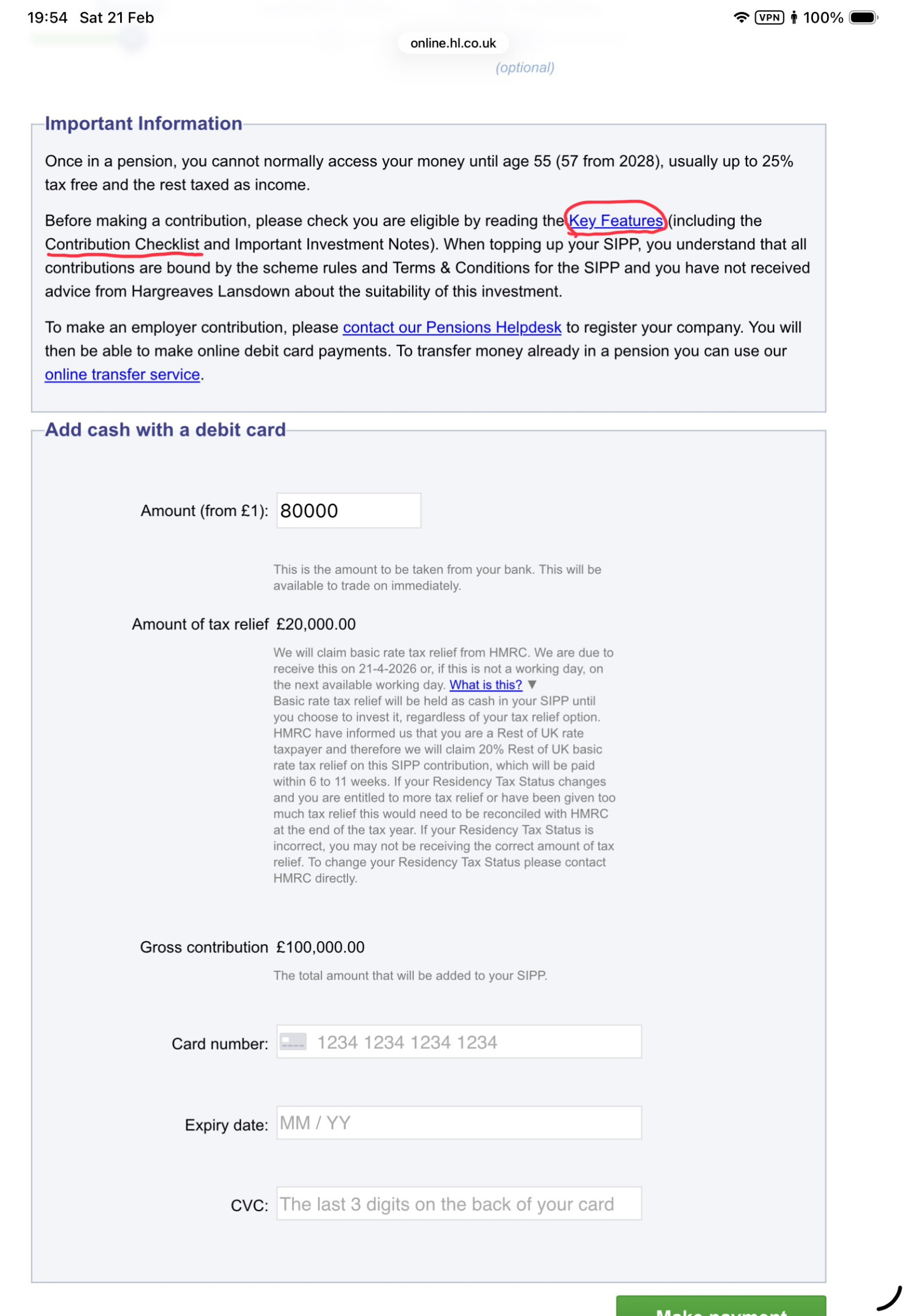

When you make a contribution …

Key Features

Contributions Checklist 5

5 -

I'm not sure you have grounds for a complaint the burden is on you.

0 -

I agree with the comments above. Thank you for taking the time highlight the rules.

I should read all small print, I didn't. I also have a HL Drawdown pension I contributed to for thirty years. I assumed I would have no problems with a new SIPP and the box next to my accounts front screen said add up to £60k, so I did.

My complaint is that HL should have checked and contacted me to make sure such a large claim was valid. I am 71 and not likely to be earning the money to pay in £45k to claim the tax.

1 -

it’s standard procedure, none of the pension providers will do what you suggest. The onus is on you.

Same as paying £20k in an ISA with HL and on the same day paying £20k into an ISA with AJ Bell. Not allowed but the systems will allow you to do it.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards