We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

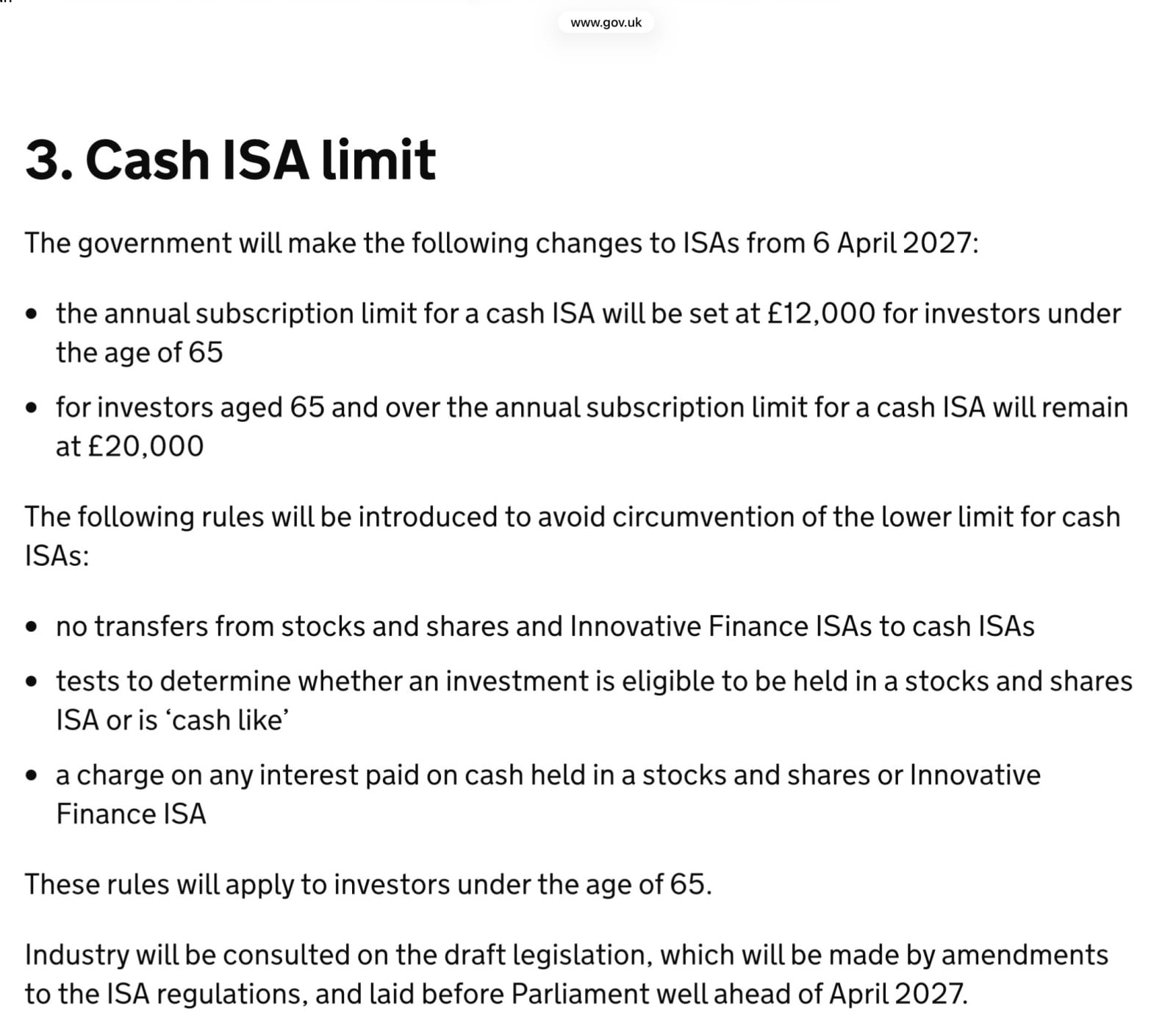

New ISA rules 2027

£12000 in cas ISA and £8000 in S&S ISA.

What if I want £20000 cash ISA?.

Could a Money Market fund be used for the £8000. sell immediately and then transfer to a cash ISA.?.

Comments

-

You'll have to wait for the rules to be announced to know for sure. If you want £20,000 in a cash ISA then you'll need to be 65 or over. Transfers from S&S ISAs to Cash ISAs were due to be stopped for under 65s too.

2 -

You would sell the MM fund (or any S&S investment) in the S&S ISA, so the cash would remain in the S&S ISA, the same as accumulated dividends and other cash.

The rules would then

(i) prohibit or limit transferring funds from S&S ISA to Cash ISA (so you can't transfer more if you're exhausing your £12 cash limit)

(ii) limit or tax the interest earned on cash in a S&S ISA (so there's no point on it being in an ISA, may as well be in a normal savings account).

Obvious loophole has already been thought of.

1 -

Yeah, just thinking ahead. Just speculation as you say. (may well have different Chancellor before too long - may be after even more tax)

OC won't work if S&S to cash ISA are stopped..

Probably stick the £8k in the SIPP rather than ISA

0 -

Seeing as pensions are more tax-efficient than ISAs for most people, then maybe do more than just the £8,000?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Yeah, just thinking ahead. Just speculation as you say. (may well have different Chancellor before too long - may be after even more tax)

To put things into context the ability to earn interest tax free is much more generous in the UK than in similar countries, even after the 2027 changes.

1 -

Won't work. The final, definitive rules haven't been published but the plan is that transfers from S&S to Cash Isas won't be allowed for people under 65.

The good news is that they're in a mess trying to finalise the new rules. With any luck it'll all be delayed:

"It comes after The Telegraph revealed a flaw in the policy that would have allowed savers to dodge Ms Reeves’s crackdown on cash. The loophole would have allowed savers to invest just 1p in the stock market and hold the rest in funds that mimic cash savings accounts, effectively swerving the levy."

https://www.telegraph.co.uk/money/investing/isas/treasury-delays-isa-tax-rules/

https://www.gov.uk/government/publications/tax-free-savings-newsletter-19/tax-free-savings-newsletter-19-november-2025 1

1 -

Always a possibility these silly plans - which cost the government more in the long run - will be dropped. Rachel Reeves probably won't be Chancellor by the time the next budget comes around - whoever takes over from Starmer.

1 -

"It comes after The Telegraph revealed a flaw in the policy that

would have allowed savers to dodge Ms Reeves’s crackdown on cash. The

loophole would have allowed savers to invest just 1p in the stock market

and hold the rest in funds that mimic cash savings accounts,

effectively swerving the levy."I don't understand that one. If cash-like funds are taxed, then they'd just tax the £7999.99 in those funds, having an additional 1p in a different fund/stock wouldn't prevent that. And if they're not taxed, just put the full £8000 in.

Maybe the telegraph is suggesting a new fund is formed which is cash-like with a small proportion of equities, in which case I expect there'd be some kind of boundary like there is for determining whether income from a fund counts as dividend or interest (something like <40% equities means the fund income is treated as interest).

2 -

You'd think that but apparently this is how the new rules have been drafted - I'm guessing they're back to the drawing board.

Apparently, unlike the pre-2014 rules, the new rules weren't to ban MMFs, <5yr gilts and the like from being held but rather only levy the 22% charge if the portfolio was 100% cash-like. It was pointed out that just one penny in shares would therefore fail this test and the charge would't be levied.

I suspect the complications arise because they want two sets of rules, one for under-65s and another for over-65s, and the brokers/platforms want to be able to provide the full range of financial securities with the simplest implementation.

3 -

Hopefully they'll shelve the whole idea.

Bit of a dogs breakfast, if you ask me.

How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)10

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards