We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

ISA flexibility: withdrawing current tax-year subscriptions and replacing elsewhere

Comments

-

Vanquis Triple Access Cash ISA (issue 5)

I've waited until today to open the above account because of the question posed earlier earlier regarding the 2025/26 subscription. My intention is to fund the account with £20,000 now, but I expect to withdraw all the funds in July and subscribe again later in the year, most likely as a fixed term ISA with another provider. On the Vanquis application there is a choice of monthly/annual interest back into the ISA, my question is "what can I do with the interest if I keep the Vanquis ISA open." Obviously, I could just leave the interest in the Vanquis account, but is the only way to move the interest funds via an ISA Transfer?

0 -

Thanks, sounds like I could be playing with fire here…

Round numbers for ease. £40k in T212 at start of 25/26 (old money)

£10k withdrawn and put in ISA1 (not flexible)

£10k withdrawn and put in ISA2 (not flexible)

(so all my 25/26 new subscriptions used but I have a 'replacement allowance in T212 that I planned to top back up at the end of 25/26)

Other withdrawals made in year to fund RS etc so my net withdrawals exceed my net deposits into T212

£20k REPLACED into T212 (doesnt affect 25/26 threshold) and is going into the same ISA anyway.

Finally, flexibly withdraw from T212 as the deposits into it were made in 25/26 and because of this they can be withdrawn and deposited into a different ISA (so copilot tells me...)

I suspect I could be in for a breach here as the replacement made in 25/26 are

possiblydefinitely seen as 24/25 funds, so the subsequent withdrawal would be back from 24/25 and should technically only go back into the same ISA (which was my plan, but the temptation on Prosper at 4.7% + £100 was too much to pass up)

I will contact Prosper to see if they can sort it out….0 -

Yes. Vanquis is a flexible ISA so you could withdraw the 20k and replace it in a new ISA but to keep the interest within the ISA umbrella, you either need to keep the interest in the Vanquis ISA or do an ISA transfer.

What may work better is for you to replace the money back into the Vanquis and then initiate the ISA transfer to a fixed cash ISA (or you may decide you aren't bothered about keeping the interest within the ISA umbrella and decide to close Vanquis and withdraw interest)

#24 Save 12k in 20261 -

Thank you for you helpful response, would it be better to choose monthly interest, or doesn't it make a difference?

0 -

Yes, you do appear to have contributed £40K in 2025/26, so you can either cancel the Prosper ISA, if still within the cooling-off period, or wait and see what action, if any, HMRC take when they run their compliance checks later in the year - anecdotally, first-time 'offenders' will often be forgiven for minor breaches, but not sure if they'd be so generous when paying in double the allowance.

0 -

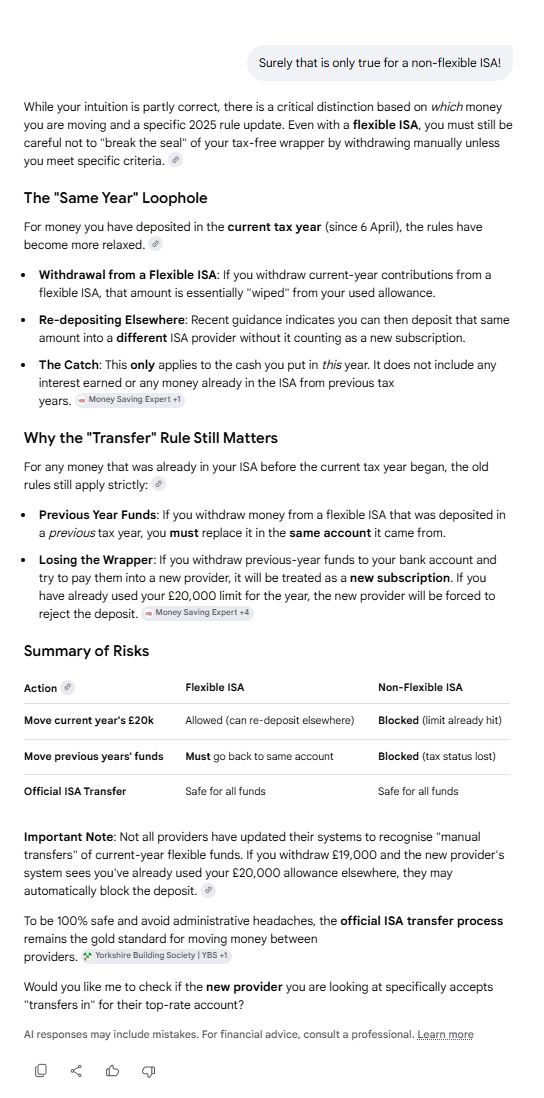

And yet another demonstration of the dangers of believing what AI says!

The steer given in that response only applies to non-flexible ISAs, whereas flexible ones do allow withdrawal of current year money and redepositing it into a different ISA (by year-end) without this counting towards the contribution allowance.

3 -

Thanks for that. I went back to the 'AI' question for clarification and I think it's now saying what you are? Does this sound better?

0

0 -

That looks better, although the last line is probably the most relevant! Stuff like "If you withdraw £19,000 and the new provider's system sees you've already used your £20,000 allowance elsewhere…" reduces credibility when there is no such way for one provider to see what's been deposited elsewhere…

0 -

Just by way of conclusion, I phoned HMRC on Tue 7th (only 50mins wait….) who said they could see no evidence of overpayment at the time and suggested I speak to ISA provider, but in any case it would be picked up later in the year with any extra tax on the interest calculated (no mention of fines/penalties)

In the meantime I'd got in touch with Prosper, with whom I'd made the most recent overpayment to explain I'd oversubscribed in 25/26 and would like it in 26/27, and they said to just withdraw it and redeposit it! I confirmed this would put the funds into the correct tax year, and they said it would (I was dubious as a flexible ISA it would be a withdrawal of previous year funds and replacement BACK INTO the previous year, but I didn't press them on this)

So, funds out and back in again within 24 hours. My app still says I haven't used any of my 26/27 allowance, but I will assume that I have and I will keep the records of the conversation with the customer service agent in case of any comeback with HMRC later on.

Will try and keep things simpler for this year!

1 -

Withdrawing from a flexible ISA and then replacing the funds into the same ISA is pointless as you correctly understood. You still have your full 26/27 ISA allowance to use wherever you like. HMRC may or may not catch up with you on the 25/26 allowance in due course, but I would not give up this year's allowance as this will be unlikely to change anything.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards