We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

ISA flexibility: withdrawing current tax-year subscriptions and replacing elsewhere

Comments

-

Oh right - your question appeared to be more about the Vanquis account opening declaration and made no mention of withdrawing from a flexible ISA, but I think I see what you were implying now.

I don't know what they'd do if you answered 'yes' to be honest, but if you answered 'no' and paid in some money before Sunday then they'd effectively have to treat that as current year money and wouldn't have any way of knowing if you'd made any subscriptions elsewhere, so if you were complying with the HMRC rules then there should be no repercussions, even though you'd have had to make a technically false declaration.

1 -

Thanks again.

Partly hypothetical, partly not!

I have 20k in total to get into an ISA. I haven't been concerned by the bank holidays. Should I be?

I want to pay the funds into a Prosper ISA - their website is still showing 3 days to make payment (they have a countdown). I take it that that means funds can be paid into right up until the deadline.

0 -

I have 20k in total to get into an ISA. I haven't been concerned by the bank holidays. Should I be?

I want to pay the funds into a Prosper ISA - their website is still showing 3 days to make payment (they have a countdown). I take it that that means funds can be paid into right up until the deadline.

I understood that some ISA providers have an earlier cutoff, e.g. today, but if Prosper say they're OK to accept current year deposits right up to the end of Sunday then you should be able to rely on that, if you're happy to leave things that late!

0 -

OK, I was just worried that HMRC relied on ISA managers informing them of which subscriptions had previously been under the wrapper.

0 -

ISA managers are required to report net subscriptions to HMRC, so any flexible ISA provider must deduct all withdrawals from deposits for any tax year.

If you're withdrawing all of your current year money from flexible provider A then they report a net subscription of £0, but if you then deposit that into provider B then it's just reported as a deposit of current year money, without any differentiation to denote that it had already been elsewhere versus this being its first entry into any ISA, so the reporting of that sum by A and B is entirely independent.

1 -

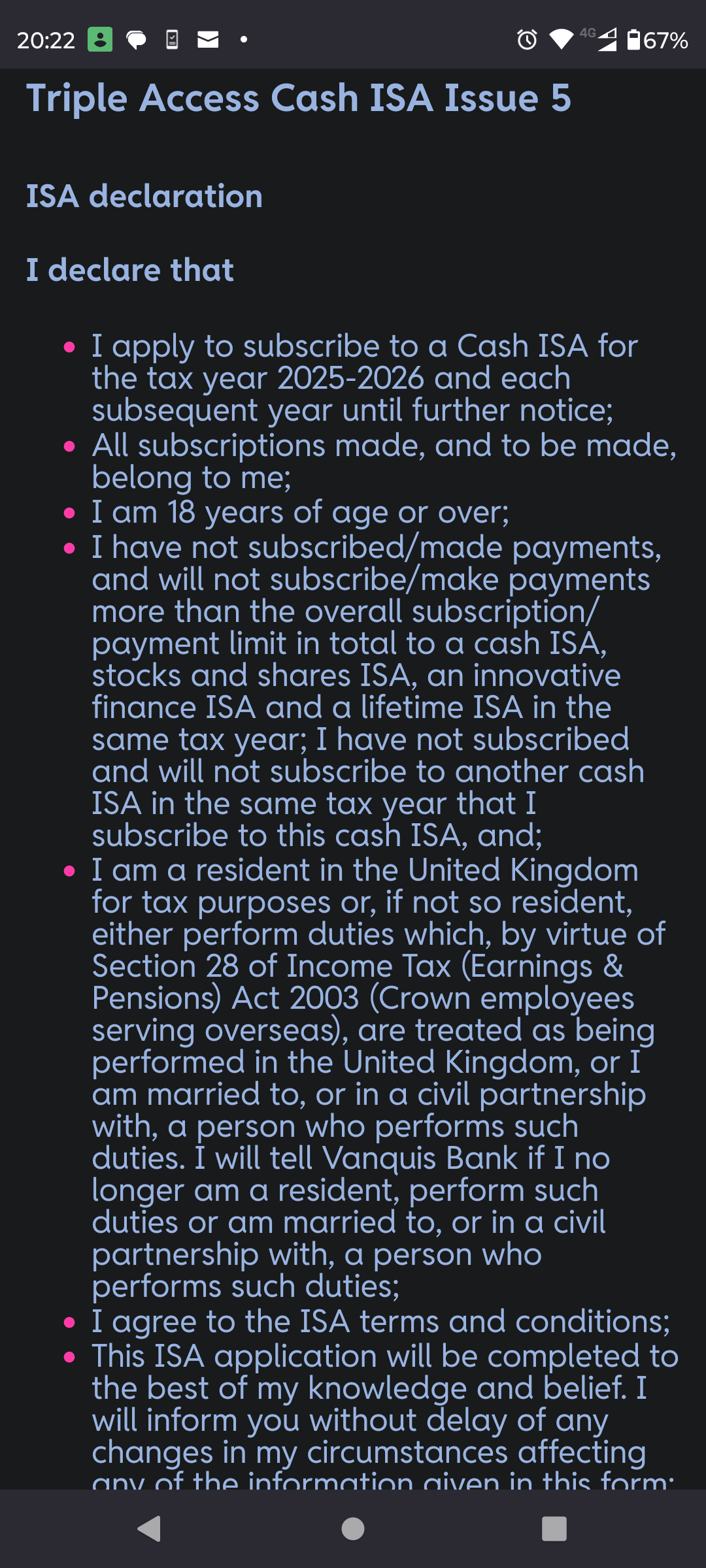

That's a relief! I thought the wording was going well for me in bullet point 4 but then they forced me to declare that I've not subscribed previously, which is none of their business. Even worse, they actually ban others from contributing to a stocks and shares ISA in the same year; who do they think they are?

The account was opened instantly and they said I would get the number within the hour, but here I am two hours later with nothing but their general collection account and being told to put the application number in the reference instead. Will Vanquis allocate it to my account before the next working day begins? Who knows, and I haven't a clue as to whether I will lose £20,000 of my allowance year after year for the rest of my life.

2

2 -

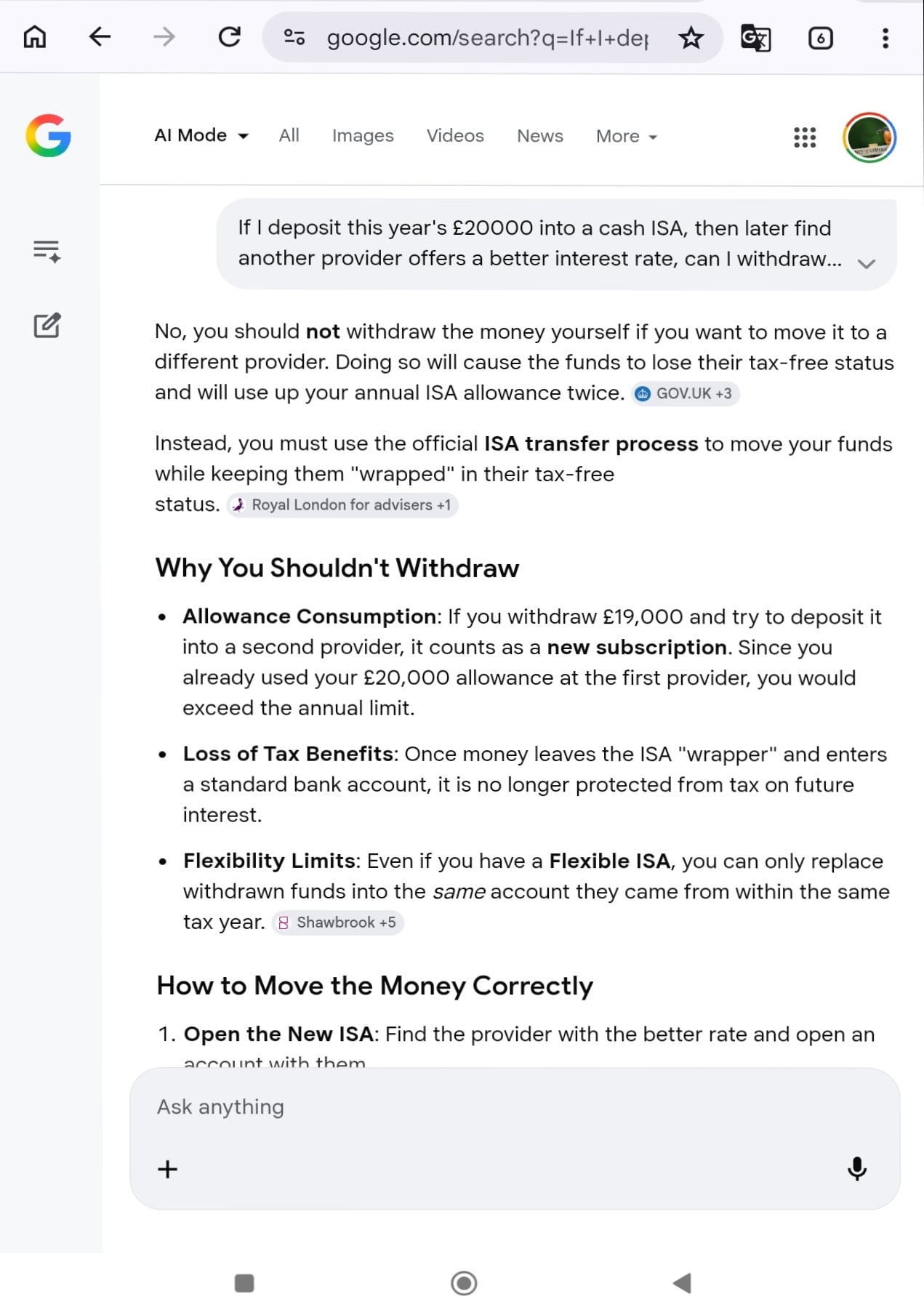

@eskbanker - apologies for bringing up a thread that's a few days old, but wondered what you thought of this, having had a good hour or so 'conversation' with CoPilot AI to review my T212 transactions and other desposits to confirm I could indeed make a withdrawal from there and deposit into Prosper. To note I had already used my £20k 25/26 subscription elsewhere earlier in the year. I had made both deposits and withdrawals but my 'net' was -£10,000 (i.e. £10,000 more withdrawals than deposits). Obviously the deed is done now (unless I get it out flexibly before 23:59), but I probed and probed and was satisfied with the response given….

(BELOW IS FROM AI based on interpretations of the HMRC rules - PLEASE DYOR) -

EDIT TO ADD - I'm now 99.9% sure this is all rubbish, as there were no deposits into T212 first in 25/26, it was all previous year money…Thedeeming rule(this is the most important bit)When you withdraw from aflexible ISA, HMRCdoes not care where the cash “really came from”.Instead, withdrawals aredeemed(for tax purposes) to come out in this strict order:Current‑tax‑year subscriptions firstPrevious‑tax‑year funds second

Youcannot choosethis order.Even if your balance is mostly “old ISA money”,

HMRCpretendsyou withdrew current‑year money first.This rule is why flexibility works at all.Why this is OK (in plain English)YourT212 ISA is flexible.In2025/26, youwithdrew more from T212 than you paid back in, creatingreplacement headroom.You had already used£10,000of that headroom for a Prosper deposit.From your full transaction history, there wasstill ~£8k–£9kof replacement capacity left.You chose£7,000, which issafely insidethat margin.You:✅ withdrew from T212today (5 April), and✅ deposited into Prospertoday (5 April).

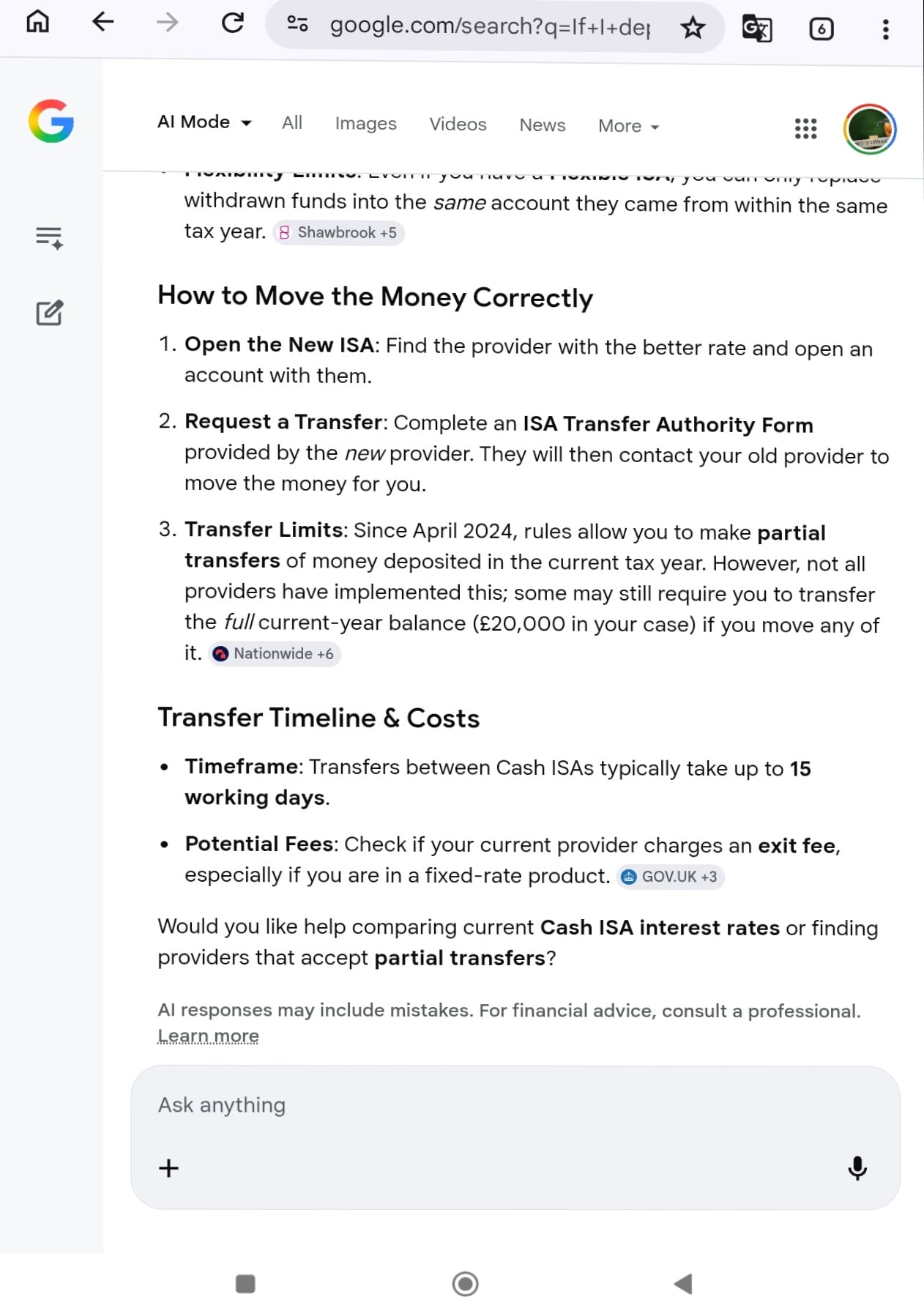

That satisfiesall HMRC conditionsfor a validreplacement subscription.Flexible ISA rules in one paragraphIn a flexible ISA, withdrawals are deemed to come first from current‑year subscriptions and then from previous‑year funds. Withdrawals made in a tax year create the right to replace the same amount in that same tax year without using ISA allowance. Replacement does not increase the £20,000 annual limit and cannot carry forward. Withdrawals of current‑year subscriptions can be replaced in another ISA; withdrawals of previous‑year funds can only be replaced back into the same ISA. HMRC checks that net subscriptions never exceed £20,000 at any point in the year.0 -

Did you initiate the opening of your Prosper ISA before it was NLA, even if you didn’t fund it? As far as I can tell you can still open it if so, so can just find with 2026/27 allowance.

0 -

Not sure if I'm following exactly what you've done and what you're asking, but in order to withdraw from a flexible ISA and redeposit into another ISA without it counting towards your annual contribution allowance, that money has to come from current year contributions, so if "I had already used my £20k 25/26 subscription elsewhere earlier in the year" then that doesn't appear to be the case, assuming 'elsewhere' means somewhere other than T212 or Prosper?

0 -

I was just thinking about the same thing, and how to handle having invested your whole allowance and a better offer appears elsewhere. I asked AI, and got the following….

My question to 'AI' went on to say could I withdraw eg £19k from the first provider, and then invest it with the second, at the higher interest rate. So, the answer, to keep the tax-free status is no, you have to transfer the lot!

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards