We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Asset Allocations by Country and Asset Type

Comments

-

I'm not sure why my action is attracting so much scrutiny and debate, it's simple enough. I sold my US tracker, because I no longer wanted to hold a US only index tracker. I bought the HSBC AW fund because I believed that the dilution effect would better be lower risk, I'm now trying to undertstand if the move achieved the results I expected and how it relates to the bottom line, during the recent Trump/Greenland blip, and subsequent recovery period. If there was no measurable benefit from switching, I made a mistake and shouldn't have done so. If there was, I want to understand it. None of this is about getting lucky, nor is it about making a comparison of two like funds.masonic said:The reason I suggested comparing equivalent funds that share a valuation point is that it’s the only way to get an intellectually honest result using fund prices.If you only want to compare the L&G US Index and the HSBC All-World, you have to look past the wrapper of the fund and at the indices they actually track. Both of these funds are simply tracking an index that is valued more than once per day and can be compared like for like.The difference you saw isn't a real performance difference in the underlying assets, it's a reporting lag. Because the L&G fund prices 3 hours later, it captured part of relevant global markets' movement that the HSBC fund missed. To see if your US dilution actually worked in the short term, you have to look at the indices themselves over a synchronised period. If you compare the FTSE USA Index against the FTSE All-World Index for that same period, you will see the true difference. That removes the timing mirage created by the fund providers' different valuation points. Until you synchronise the timeframes by looking at the indices, you aren't comparing the performance of your move you’re just comparing performance over different periods. It is like trying to demonstrate your back garden is cooler than your front garden by checking the thermometer in the front at midday and at the back at 3pm.Whereas if you are just trying to demonstrate you got lucky (or otherwise) by effectively being out of the market during the switch, then indeed that is part and parcel of switching between funds. But that would concern relative performance on T-1 day and T-2 days.0 -

chiang_mai said:

I'm not sure why my action is attracting so much scrutiny and debate, it's simple enough. I sold my US tracker, because I no longer wanted to hold a US only index tracker. I bought the HSBC AW fund because I believed that the dilution effect would better be lower risk, I'm now trying to undertstand if the move achieved the results I expected and how it relates to the bottom line, during the recent Trump/Greenland blip, and subsequent recovery period. If there was no measurable benefit from switching, I made a mistake and shouldn't have done so. If there was, I want to understand it. None of this is about getting lucky, nor is it about making a comparison of two like funds.masonic said:The reason I suggested comparing equivalent funds that share a valuation point is that it’s the only way to get an intellectually honest result using fund prices.If you only want to compare the L&G US Index and the HSBC All-World, you have to look past the wrapper of the fund and at the indices they actually track. Both of these funds are simply tracking an index that is valued more than once per day and can be compared like for like.The difference you saw isn't a real performance difference in the underlying assets, it's a reporting lag. Because the L&G fund prices 3 hours later, it captured part of relevant global markets' movement that the HSBC fund missed. To see if your US dilution actually worked in the short term, you have to look at the indices themselves over a synchronised period. If you compare the FTSE USA Index against the FTSE All-World Index for that same period, you will see the true difference. That removes the timing mirage created by the fund providers' different valuation points. Until you synchronise the timeframes by looking at the indices, you aren't comparing the performance of your move you’re just comparing performance over different periods. It is like trying to demonstrate your back garden is cooler than your front garden by checking the thermometer in the front at midday and at the back at 3pm.Whereas if you are just trying to demonstrate you got lucky (or otherwise) by effectively being out of the market during the switch, then indeed that is part and parcel of switching between funds. But that would concern relative performance on T-1 day and T-2 days.No one is scrutinising the logic of your move. You have a rational argument for further reducing US exposure.The debate is simply about the measurement that led you to conclude it was "definitely a good move" based on performance data. During the Greenland blip, the US markets dropped 2% on Tuesday. Because the L&G fund prices at 3:00 PM, it captured some of that US sell-off a day earlier than the HSBC fund, which was still valued at prices from noon.You’ve been provided with two alternative ways to measure the relative performance of All-World vs. USA that don't rely on these stale prices. Either compare two equivalent funds with the same valuation time or compare the underlying indices. If you are unwilling to look beyond the flawed measure of daily snapshots at different times, which even you have acknowledged introduces a large discrepancy, then you are deliberately choosing for the true short term result of your move to remain a mystery to you. You are essentially looking at two clocks set three hours apart and wishing there was some way you could make them strike midnight at the same time.I'd put it to you that the jury is still out on whether you'll get a benefit, and will be for quite some time (this is the first method suggested: synchronised daily priced fund pair vs continuously priced ETF pair, the latter more up to date)...

0

0 -

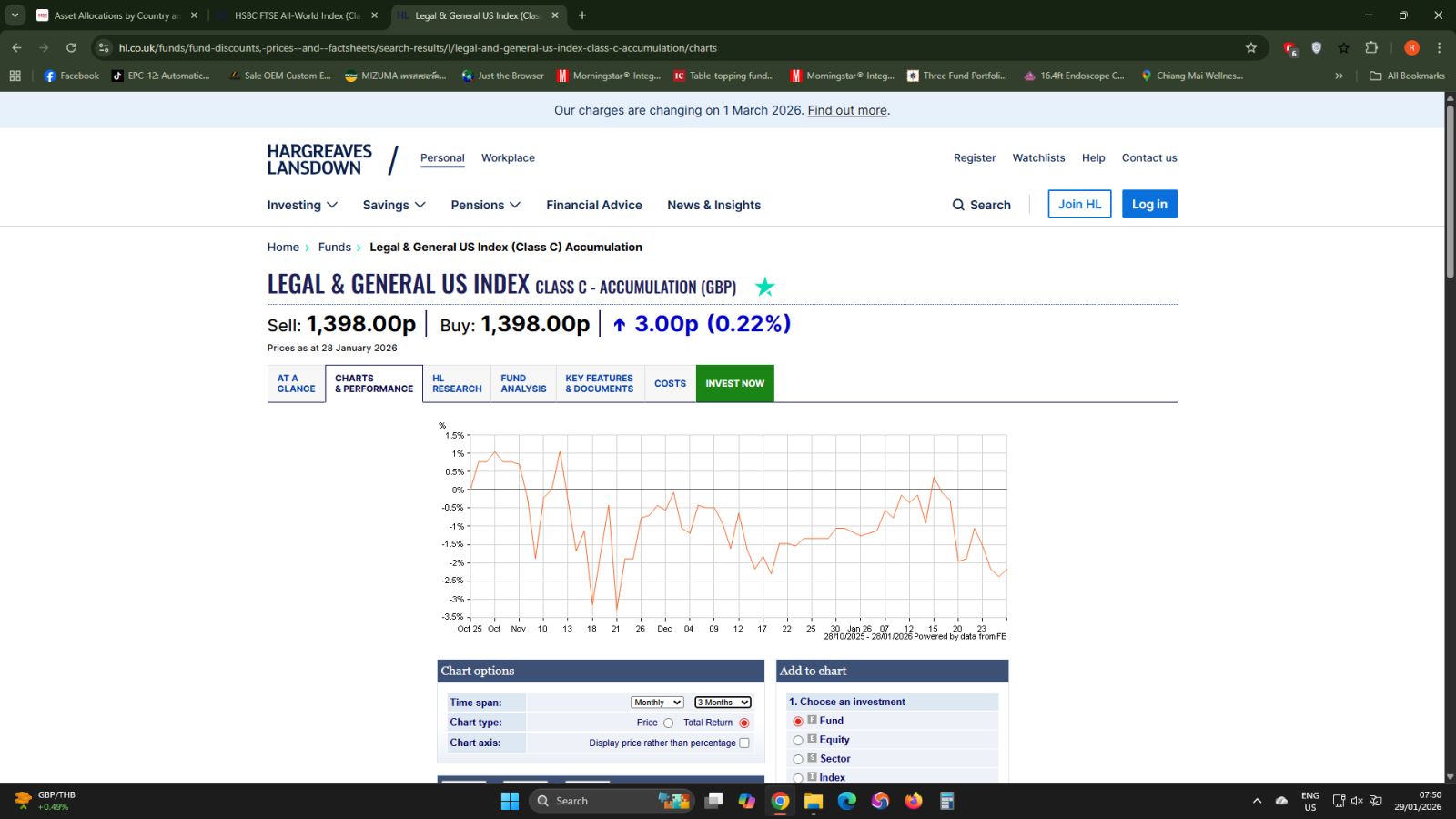

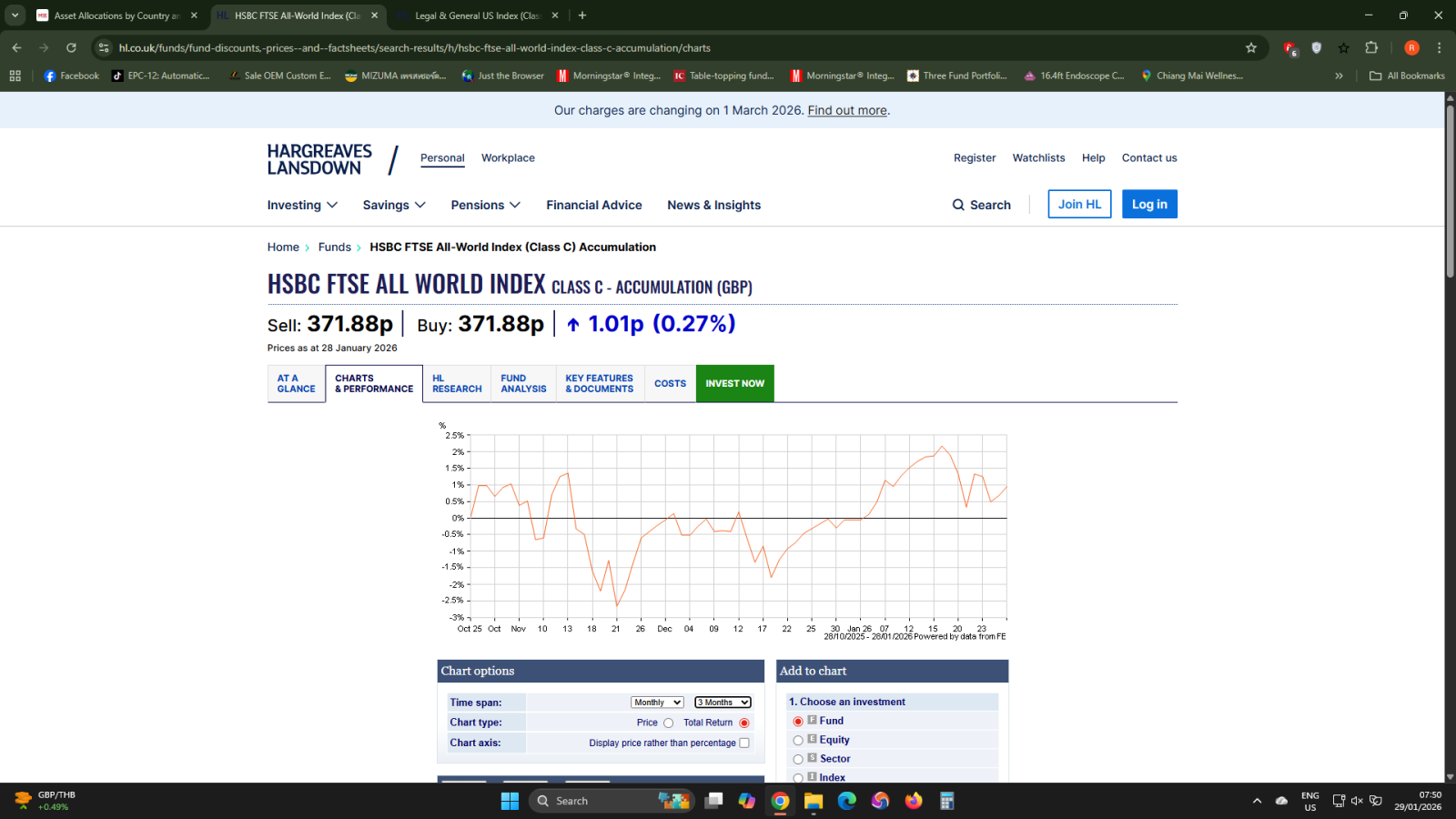

Further to our recent discussion about whether or not a FTSE All World Index tracker, with its diluted US component, would perform better or worse than a straight forward L&G US only Index tracker:

1

1 -

A meaningful difference. Do you have comments?

I imagine the recent weakening USD will explain much of that difference.

0 -

I'm afraid not, but I'm sure others will be along shortly to explain it. Call me niave or a simpleton if you wish but the logic seems evident. A 63% US allocation, combined with 37% non US assets, will be more cushioned in both directions, than a 100% US allocation. Unless of course you believe that all markets move in tandem, in the same direction, which would mean geographic diversification is impossible.

1 -

If you look at the currency chart, the turning point was October 2022:

Then compare with a comparison chart:

Indeed the US index fund underperformed global during the weakening phase up to early 2023, then gained a lot in the lead-up to the Trump Tariff correction, and then lost ground again during 2025 (and has underperformed global over 1m, 3m, 6m, and 1y).

Currency effects will tend to be temporary in nature, because you have underlying multinational businesses being valued on their cashflows, which will tend to adapt to the new monetary environment. This is not fixed interest where the cashflows are fixed for the lifetime of your investment in a particular currency.

1 -

My understanding is that neither of the two standard offering of those funds is hedged back to Sterling.

This should mean that the currency impact on both funds is the same, only the volume or scale changes.

The standard, HSBC FTSE All-World Index Fund (often used by UK investors, such as the Class C Acc - GB00BMJJJF91) is not hedged back to Sterling (GBP)

Based on the Legal & General (L&G) fund offerings, the standard "L&G US Index Trust" is

not hedged back to sterling. It is an unhedged fund that tracks the FTSE USA Index, meaning your returns are affected by the exchange rate between US Dollars (USD) and British Pounds (GBP

.

0 -

The funds are not hedged back to sterling. However, the impact of a weakening dollar will be different for an index of companies listed on US exchanges vs a broader group of companies listed worldwide. This will cause one index to move differently to the other in response to currency movements (accepting that one is a very large constituent of the other).

The companies adversely impacted have the option to reprice their goods and services to restore the real value of their revenue. Provided they have a sufficiently captive customer base and/or aren't put at a disadvantage vs international competitors.

For the above reason, "currency hedging" equity exposure doesn't really achieve what it sets out to. It is a collateralised and slightly leveraged bet on exchange rate movements (given you get some benefit already by merely holding productive businesses with pricing power).

1

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards