We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Advice on fund

Comments

-

I hold BIPS as part of an income equity portfolio, it has, for a number of years, performed as you may expect (I acknowledge and understand all the comments above). I’m happy with it and regularly review, I will almost certainly increase holding in 2026 as recent outcome from this month’s review- as a component of entire portfolio it has been doing exactly as expected- but I hold primarily for regular income for the next 6 ish years until all my DB pensions kick in.Linton said

If your requirement was fairly stable high income:

- capital value bouncing up and down within +/- 15% for almost all of 30 years with no long term falls

- 242 underlying holdings

- about 70% of holdings with duration < 5 years

looks pretty safe to me as anyone buying this fund for income would likely have no intention of selling and so have no concern about temporary mostly small variability in price. In any case a prudent income portfolio would require holdings in a wider range of asset types and should arguably be more geographically spread given the 50% or so dependence on the UK of this fund.

Summarising, in my view the fund looks reasonable for its purpose as part of a wider portfolio - I may even look at it for my income portfolio. Whether it meets the OP's objectives is of course a very different matter.There was a video from the BIPS management on the AJ Bell platform recently -November.(?) which I thought was quite informative , if that’s openly available I’d recommend watching ,

HTH1 -

The Association of Investment Companies that I mentioned, is a very well known website for Investment Trust enthusiasts.dont_use_vistaprint said:

No, I've never heard of that website, but I think you probably knew that anyway before you wrote it 😀Eyeful said:1. If the OP was after dividend payments, I would have thought their first stop would have been to take a look at the S&P Dividend Aristocrats range of funds and ETF's rather going for this risky investment trust.

2. I wonder where he is getting his information from?

Has he even taken time to look at the AIC website?

https://www.theaic.co.uk/

I tend to go with advice from people I know personally who know far more about this stuff than me, sense check it on places like here, but also often just go with things that feel right. I do dial into a few WebEx for quarterly earnings reports of companies I invest in directly, I listen to questions asked by people like Barclays and I read the news

So I am very surprised you have not even heard of it before, .

I wonder why those giving you advice, did not suggest just taking a look at the website, if only to see what is available in the Investment Trust world.0 -

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for incomeThe greatest prediction of your future is your daily actions.0 -

One can bias investment for income, for growth, in undervalued assets or to try and maintain purchasing power. All part of a bigger plan. We should judge income investments, value out investments and those for capital gains by their total return.dont_use_vistaprint said:Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the name

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for income

Personally I think inflation a risk to all funds though more to high income funds who's capital or income don't pace inflation especially for those with a longer horizon. A cap weighted global index is usually more enwealthing than for example a high yield junk bond collective on 6% yield.1 -

That's fine - it's your choice - but it seems clear you don't fully understand what you will be investing in. One of the first rules of investing is not to buy a product you don't understand. That doesn't mean it will go wotsits up - you might do fine with it - but you might get a bad result because of risks you weren't aware you were taking. That said, there are plenty of more risky investments around, so you're not putting you life on the line. Since I started DIYing eight years ago I've bought (and usually quickly sold) a few funds I didn't understand, but at the time I didn't necessarily realise I didn't understand them. I think all of them were bond funds - they are much more complicated to understand than equities. So I wish you good luck but advise you to keep educating yourself about bonds so that you are not relying too much on the advice of people who tell you (who tell you...) they have been investing successfully for 40 years.dont_use_vistaprint said:

Everything I've read on her tell me it's right for me, it came highly recommended from someone I trust on these matters who's been investing successfully for 40 years, but it's always good to get other peoples views and perspectives, I mostly skim read over the expressive language from those with an agenda, but there's some really good advice on this thread as well.Linton said:

If your requirement was fairly stable high income:InvesterJones said:dont_use_vistaprint said:

Yes, of course lots of things are in the picture but this post wasn't about them, or my investment requirements And whether it fits, It was about understanding the characteristics of this particular investmentInvesterJones said:

For me stable would be non-volatile and avoiding capital loss. Many funds did lose capital in 22 as a rare event, but things like junk bonds also lost capital at many other times as you can see from the chart. If you're now not actually concerned with volatility or capital loss then equities should also be in the picture since the trend line is also positive.dont_use_vistaprint said:

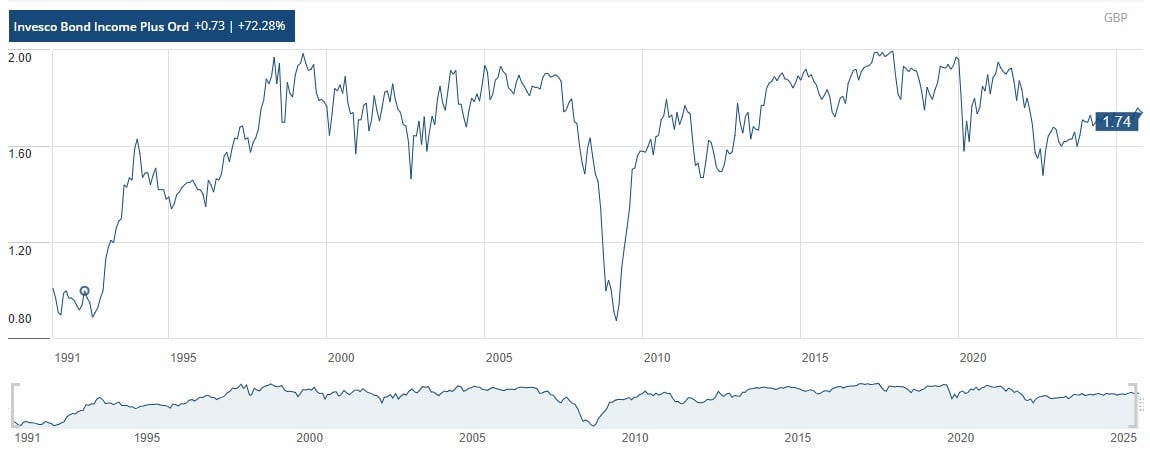

Define stable ? the trend line is going the right way , looks good to me I've seen much worseInvesterJones said:dont_use_vistaprint said:The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.What source are you using for evidence of this long history of being stable? To me it looks like the capital is not at all stable:

Ah OK. So are you clearer now about the characteristics of this fund? It's made up of junk bonds, which are non-stable and do suffer capital loss, and tend to behave more like equities than bonds. As a result, people demand a higher return. This credit spread is currently quite narrow/tight, meaning there's not much compensation for taking on equities-like risk.

- capital value bouncing up and down within +/- 15% for almost all of 30 years with no long term falls

- 242 underlying holdings

- about 70% of holdings with duration < 5 years

looks pretty safe to me as anyone buying this fund for income would likely have no intention of selling and so have no concern about temporary mostly small variability in price. In any case a prudent income portfolio would require holdings in a wider range of asset types and should arguably be more geographically spread given the 50% or so dependence on the UK of this fund.

Summarising, in my view the fund looks reasonable for its purpose as part of a wider portfolio - I may even look at it for my income portfolio. Whether it meets the OP's objectives is of course a very different matter.

I'm definitely not averse to risks & although the risks in this case don't seem that material for my purposes and the income. Opportunity fits nicely as interest rates are dropping.3 -

I prefer a total return approach to income generation with the idea that it spreads the risk across asset classes and would not feel comfortable with the majority of my bond holdings being B rated. But I can see the attraction of the BIPS dividend. The question still remains, why do you want income now? Are you retired?dont_use_vistaprint said:

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for incomeAnd so we beat on, boats against the current, borne back ceaselessly into the past.1 -

Bostonerimus1 said:

I prefer a total return approach to income generation with the idea that it spreads the risk across asset classes and would not feel comfortable with the majority of my bond holdings being B rated. But I can see the attraction of the BIPS dividend. The question still remains, why do you want income now? Are you retired?dont_use_vistaprint said:

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for incomeThe 'total return' question is an interesting one. A friend of mine retired a few years ago and favours income-generating assets; while I was still working/accumulating I thought "surely you want your assets to increase in value as much as possible". Now that I am heading into retirement I understand it; you want to receive a reasonably consistent natural income from interest/dividends and not risk having to sell assets during a downturn. So I have bought a few bond funds that generate good income and have switched a couple of my vanilla equity index funds for income funds (index income in the UK and smart beta income in EM).I expect your responses will be that you are spreading risk across asset classes and so only sell those which have not fallen. However that seems at odds with you telling us, quite often, that you only hold two or three equity and bond index funds in addition to your rental income.0 -

aroominyork said:Bostonerimus1 said:

I prefer a total return approach to income generation with the idea that it spreads the risk across asset classes and would not feel comfortable with the majority of my bond holdings being B rated. But I can see the attraction of the BIPS dividend. The question still remains, why do you want income now? Are you retired?dont_use_vistaprint said:

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for incomeThe 'total return' question is an interesting one. A friend of mine retired a few years ago and favours income-generating assets; while I was still working/accumulating I thought "surely you want your assets to increase in value as much as possible". Now that I am heading into retirement I understand it; you want to receive a reasonably consistent natural income from interest/dividends and not risk having to sell assets during a downturn. So I have bought a few bond funds that generate good income and have switched a couple of my vanilla equity index funds for income funds (index income in the UK and smart beta income in EM).I expect your responses will be that you are spreading risk across asset classes and so only sell those which have not fallen. However that seems at odds with you telling us, quite often, that you only hold two or three equity and bond index funds in addition to your rental income.

Right now I'm around 80/10/10 and the equity portion is growing because I've stopped rebalancing. It is in essentially 4 funds, US equity, International equity and a multi-asset fund for it's bonds...and a MMF for the cash. I'm retired but not investing for income, so I can emphasize growth.

While I don't take income from my investments, if I was relying on them for income I'd probably have a fairly aggressive equity and bond allocation with a substantial cash allocation, maybe something like 60/30/10. I'd probably look for some dividends from the equities as well as growth and keep my bond allocation high quality and with maturities less than 10 years. I'd try to keep my withdrawals to the natural yield and target something like 3%. I base this on the efficient frontier. If I was in the accumulation phase I wouldn't hold as much cash and might emphasize potential growth over dividends, but really both portfolios would be quite similar. Of course your appetite for risk, need for return and the size of you pension pot must also be considered. I'd never own a junk bond fund as I want bonds to be a low volatile part of my portfolio and as an income source I might look at laddering them. But the classic retirement income generator is the annuity.

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Yes I retired at 52 i've just managed to draw a tiny LGPS and to me this makes more sense than chipping away at capital and savingsBostonerimus1 said:

I prefer a total return approach to income generation with the idea that it spreads the risk across asset classes and would not feel comfortable with the majority of my bond holdings being B rated. But I can see the attraction of the BIPS dividend. The question still remains, why do you want income now? Are you retired?dont_use_vistaprint said:

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for income

regarding the comment about inflation risk, personally since retiring I find most of my spend is negative inflation. Inflation is concerning for a certain type of spender/consumer, when you retire your lifestyle completely changesThe greatest prediction of your future is your daily actions.0 -

Bostonerimus1 said:

While I don't take income from my investments, if I was relying on them for income I'd probably have a fairly aggressive equity and bond allocation with a substantial cash allocation, maybe something like 60/30/10. I'd probably look for some dividends from the equities as well as growth and keep my bond allocation high quality and with maturities less than 10 years. I'd try to keep my withdrawals to the natural yield and target something like 3%. I base this on the efficient frontier.aroominyork said:Bostonerimus1 said:

I prefer a total return approach to income generation with the idea that it spreads the risk across asset classes and would not feel comfortable with the majority of my bond holdings being B rated. But I can see the attraction of the BIPS dividend. The question still remains, why do you want income now? Are you retired?dont_use_vistaprint said:

Its effort and having to sell off capital to gain income ? Income assets are just easier for income , I guess that's a clue in the nameBostonerimus1 said:

Nope, just pointing out that a total return approach from something like VLS is a legitimate way to generate income and asking why you want income now and from such a risky source as a junk bond fund.dont_use_vistaprint said:

Are you suggesting this fun now is comparable to the distribution of VLS 80 ? or comparable to a capital growth fund where you just keep selling bits of capital ...... honestlyBostonerimus1 said:

There's an income version of VLS80 that distributes dividends and of course any fund can generate "income" - all you need to do is take some dividends or capital gains. But why do you want income/dividends now?dont_use_vistaprint said:

I have a huge amount of money in VLS80, it's done really well to date , it's grown way beyond my expectation, but it's going to drop & and when it does, I will be buying even more - I'm happy to leave it there for another 5 to 7 if needed but it also does not provide income.Bostonerimus1 said:

There's no guarantee about the future, but past performance can give some clues and in the end it's all the investor has. And it's why I will never invest in single stocks or risky sectors like junk bonds. I would avoid BIPS as you are taking a lot of risk and paying management fees to do it. You mentioned VLS80 and I like that as the vast majority of the bonds it contains are A rated or better and you get exposure to global equities.dont_use_vistaprint said:

so why do people constantly post graphs of past performance to try and back up their statements on here?wmb194 said:

Past performance is no guarantee of future performance.dont_use_vistaprint said:

Yes better balance. Something for regular income to add to a small LGPS & interest from savings to cover alLinton said:

BIPS (or any other investment) could only be recommended in the light of your circumstances and what you want from your investment. It really is a niche fund bought for specific objectives. It is unclear what your objectives are and how your proposed addition fits in with the rest of your portfolio. Do you want more of the same or something to provide a better balance to your current holdings.dont_use_vistaprint said:Thanks for the comments.

So my understanding is it's an an income generating asset, and inside a SIPP it would regularly pay into the cash balance rather than focus on capital growth & you could re-invest that but would pay fees each time so it's more suited to someone drawing those dividends as regular income and it fairly reliable in the income of 6-7% and the capital is generally low risk but don't expect much or even any growth. And look for discounts when timing the initial buy.

Im assuming the dividends it pays inside a SIPP would be treated as uncrystallised currently? and may in future be subject to tax even before drawdown ?

is that about right ?Seems to me it was a very good recommendation

If your SIPP is fully uncrystallised or fully uncrystallised the income from a fund will retain the same status. However, I believe if your portfolio is partially crystalised exactly how income is treated will depend on the platform and whether it treats the crystallised and uncrystallised parts as separate portfolios.

Income within a SIPP wont be subject to tax unless the whole structure of pensions is drastically changed. Drawing down the income from a pension will be taxed exactly in the same way as any other drawdown.

the normal costs and with liquidy if I decide I need it. I have the VLS80 for longer term growth opportunity , money markets and savings for cash but with interest rates falling I'm inclined to keep less in those and so something paying 6-8% seems good.The high capital risks mentioned by some do not add up given its long history of being stable and the discounting looks attractive.no no one ever looks at the graphs of past performance right ? There's absolutely nothing to be learned from them

money markets and savings are going down and This seems to fit nicely in the middle

It's not that risky IMO , the people I know in it make good income and as pointed out its history shows it bouncing around 2% capital it's hardly risky in my view. VLS80 is far more risky with big drops every now and then. If you're using that for income you'd be having to sell in possibly the worst timing. I think vls80 is best for long term capital growth & this fund better for incomeThe 'total return' question is an interesting one. A friend of mine retired a few years ago and favours income-generating assets; while I was still working/accumulating I thought "surely you want your assets to increase in value as much as possible". Now that I am heading into retirement I understand it; you want to receive a reasonably consistent natural income from interest/dividends and not risk having to sell assets during a downturn. So I have bought a few bond funds that generate good income and have switched a couple of my vanilla equity index funds for income funds (index income in the UK and smart beta income in EM).I expect your responses will be that you are spreading risk across asset classes and so only sell those which have not fallen. However that seems at odds with you telling us, quite often, that you only hold two or three equity and bond index funds in addition to your rental income.3% is a low yield and brings us back to the role of higher yielding bond funds in a retirement portfolio. While my equities are mostly index funds, in the corporate bond space there is more potential for active managers to earn their corn. I own four actvely managed bond funds and their average yield over the last three years is:Man Dynamic Income 9.9% (plus 6.8% pa capital growth)Man Sterling Corporate Bond 8.0% (plus 7.8% pa capital growth)Royal London Short Duration Credit 5.6% (plus 2.5% pa capital growth)Artemis Short-Duration Strategic Bond 5.3% (plus 2.5% pa capital growth).Even my gilt fund has yielded 4.3%, although my hedged Vanguard Global Bond Index has yielded your 3.0% (although I do not take income from it). My point is that actively managed corporate bond funds are a good place to look for income when compared to selling equities in a total return strategy, and dividend hero equities do not yield as much.P.S. Just for completeness's sake, BIPS' three year average yield is 7.3% (plus 1.8% pa capital growth).2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards