We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Advice on fund

dont_use_vistaprint

Posts: 990 Forumite

Can I get some advice on this please how does it compare to short term money markets & funds like VLS80 in terms of risk and returns outlook . Does investing large one off amount in it now pose any additional risks

INVESCO BOND INCOME PLUS LIMITED (BIPS)

INVESCO BOND INCOME PLUS LIMITED (BIPS)

The greatest prediction of your future is your daily actions.

0

Comments

-

You never going to get something for nothing in the financial markets.

Put as simply as I can:

Short term money funds: behave almost like cash, very safe and easy to access. (lowest risk)

BIPS: Is an Investment Trust behaves much more like a higher‑risk, higher‑income bond fund.

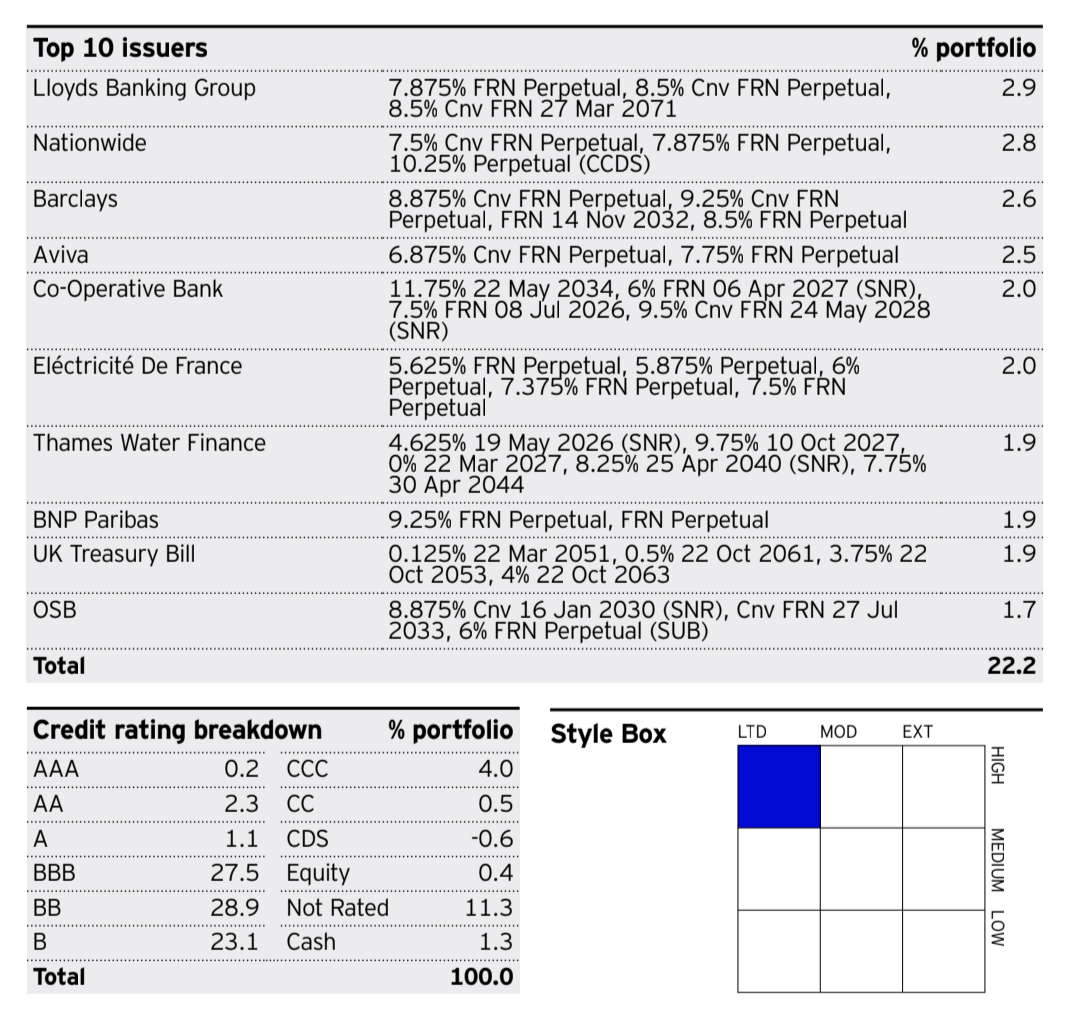

Credit risk: Around two‑thirds of the portfolio is typically in sub‑investment‑grade bonds, carrying higher default risk than investment‑grade debt.

Interest‑rate risk: (bond prices fall when yields rise).

Premium/discount risk: As a listed Investment Trust, its share price can trade at a premium or discount to underlying net asset value (NAV); buying at a premium adds another layer of price risk.

VLS 80: Open‑ended multi‑asset fund with about 80% in global equities and 20% in bonds, aiming for long‑term growth with high equity exposure. So main risk is the equity markets. Hence the most risky of the three.

No one can foretell the future, so no one can tell what will give you the best return.

Rule of thumb: The higher the risk, the higher the expected return(but that's not guaranteed).

PS. To give financial advice in the UK requires having the appropriate qualifications. All you will get here & elsewhere is guidance & information.1 -

I already did before I posted it. I'm interested in the comments from real people as well. But thank you for the offer, appreciated, I'm quite good with prompting, probably too good. I hit my daily limit in the first hour or so each day and get downgraded for the rest of the day :-) I also regularly agree with the full engine what information it is allowed to save about me and it has all the key things you mentioned (plus many more) I find this much more useful than having to contextualise prompts each time, not just for finance, but for a range of things,EdSanRo said:I just discussed this fund with ChatGPT. I suggest you do the same. Even on the free model it will give you ample answers.

It can run comparisons for you as well. Even before you hit your daily limit with the app.

You can feed the app with your personal situation. Age, work, health, your outlook, your aim, amounts etc. and it will give you a quite solid picture.

General rule of thumb: I would not come here for advice. It is a very personal thing. What works for me, does not have to work for you. There are so many variables to take into account, that there is almost no golden answer.

You can run the same questions past other LLMs. That will give you a more allround look.

You can send me a DM and I am happy to help you with some prompts.

Happy holidays.The greatest prediction of your future is your daily actions.0 -

General rule of thumb: I wouldn't recommend posters take discussions offline by resorting to DMs, which aren't available for others to scrutinise, whereas comments visibly shared in public can be seen and discussed....EdSanRo said:General rule of thumb: I would not come here for advice. It is a very personal thing. What works for me, does not have to work for you. There are so many variables to take into account, that there is almost no golden answer.

You can run the same questions past other LLMs. That will give you a more allround look.

You can send me a DM and I am happy to help you with some prompts.13 -

Thanks so what's the perspective on this Considering the recent and potential future interest rate cuts in the UK and the US, does this trend make it favourable right now?Eyeful said:You never going to get something for nothing in the financial markets.

Put as simply as I can:

Short term money funds: behave almost like cash, very safe and easy to access. (lowest risk)

BIPS: Is an Investment Trust behaves much more like a higher‑risk, higher‑income bond fund.

Credit risk: Around two‑thirds of the portfolio is typically in sub‑investment‑grade bonds, carrying higher default risk than investment‑grade debt.

Interest‑rate risk: (bond prices fall when yields rise).

Premium/discount risk: As a listed Investment Trust, its share price can trade at a premium or discount to underlying net asset value (NAV); buying at a premium adds another layer of price risk.

VLS 80: Open‑ended multi‑asset fund with about 80% in global equities and 20% in bonds, aiming for long‑term growth with high equity exposure. So main risk is the equity markets. Hence the most risky of the three.

No one can foretell the future, so no one can tell what will give you the best return.

Rule of thumb: The higher the risk, the higher the expected return(but that's not guaranteed).

PS. To give financial advice in the UK requires having the appropriate qualifications. All you will get here & elsewhere is guidance & information.

Yeah I've got the discounting thing and see it's maybe not the most favourable time to buy right now but certainly not the worst time.But then is waiting for discounting pretty much the same as waiting for a stock price to go low? Like trying to time the market? Or is this fundamentally different?The greatest prediction of your future is your daily actions.0 -

dont_use_vistaprint said:Can I get some advice on this please how does it compare to short term money markets & funds like VLS80 in terms of risk and returns outlook . Does investing large one off amount in it now pose any additional risks

INVESCO BOND INCOME PLUS LIMITED (BIPS)

A simple Google search against BIPS gave rise to the following ( unprompted ) summary :

'' For INVESCO BOND INCOME PLUS LIMITED (BIPS), the greatest risks are generally considered to be credit (default) risk and the risks associated with the use of financial leverage (gearing), which are inherent to its investment strategy focused predominantly on high-yield bonds "

Frankly if you have neither knowledge of the investment trust sector ( BIPS is not a unit trust fund), or of corporate bonds in particular then you really should not be exploring purchasing shares of this nature without extensive personal research and learning.

As regard default risks , well worth noting 2% of BIPs is held in various Thames Finance loan notes and other sundry debt issued by that business. One of the key shareholders in Thames Water consider the entire business valueless.

Needless to say BIPS have nothing in common with short term money market funds or VLS80 and it would be entirely spurious to attempt a side by side comparison of these disparate investment options.

In passing, I can see from your previous threads ( example below) that you are trying to settle on an appropriate investment strategy for your Sipp over the next 10 years

https://forums.moneysavingexpert.com/discussion/6627343/accumulation-vs-distribution#latest

Seems to me your understanding of the technical aspects of investing is still developing, which is hampering your current decision making process.4 -

Some clarity on your goals, current situation and timelines might be useful. As mentioned, the assets serve very different purposes. If you are trying to avoid risk then going for junk bonds is an interest choice as they don't really diversify much from equities.0

-

I've had it since 2016 when it was Invesco Perpetual Enhanced Income Limited (IPE)You can read the nuts and bolts elsewhere but it's an out and out income fund. It couldn't be much further from a MM or multi-asset fund like VLS80 if you tried. If either of those suit your objectives then this almost certainly won't. It would be a poor bedfellowIt has a place as part of a dedicated income portfolio at the higher risk/yield end but I'm sensing this isn't you0

-

Having secure names fill most of the top ten spaces of a fund which is 70% junk looks, to me, like a bit of window dressing.

1 -

The fund mainly invests in corporate (issued by companies) bonds with a time to maturity < 10 years and so higher risk than short term MM funds and short dated gilt funds but you can find funds that are higher risk and return higher interest. Currently the interest is about 7%. Again this is indicative of a moderately risky bond fund.dont_use_vistaprint said:Can I get some advice on this please how does it compare to short term money markets & funds like VLS80 in terms of risk and returns outlook . Does investing large one off amount in it now pose any additional risks

INVESCO BOND INCOME PLUS LIMITED (BIPS)

The downside is that being a bond fund any growth beyond that generated by reinvesting the interest will be small and could be negative. Hence it is probably only appropriate if you are looking for a steady-ish income stream.

Something like VLS80 which invests mostly in company shares will be riskier but could be expected to give a higher return, mostly in the form of increasing price. The risk means that it is only really suitable for investing for longer than say 10 years.

Short term MM funds are similar in a way to bond funds in that they generate interest rather than capital growth but are much more stable than BIPS and not surpisingly generate much less interest. They are probably only appropriate for the short term.

Note that risk here does not mean the danger of losing all your money which is is virtually zero for both funds barring the collapse of the global economy. Rather it means price volatility. VLS80 could well drop by 40% in crash or rise by a similar amount in a couple of years though the long term trend would be upwards. BIPS is very unlikely to be anything like as volatile.

So the funds are very different and you need to consider which is the more appropriate for your needs.0 -

1. When I was into Investment Trusts, I just stuck to those that invested world wide and where cheap, such as, F&C, Alliance.dont_use_vistaprint said:

Thanks so what's the perspective on this Considering the recent and potential future interest rate cuts in the UK and the US, does this trend make it favourable right now?Eyeful said:You never going to get something for nothing in the financial markets.

Put as simply as I can:

Short term money funds: behave almost like cash, very safe and easy to access. (lowest risk)

BIPS: Is an Investment Trust behaves much more like a higher‑risk, higher‑income bond fund.

Credit risk: Around two‑thirds of the portfolio is typically in sub‑investment‑grade bonds, carrying higher default risk than investment‑grade debt.

Interest‑rate risk: (bond prices fall when yields rise).

Premium/discount risk: As a listed Investment Trust, its share price can trade at a premium or discount to underlying net asset value (NAV); buying at a premium adds another layer of price risk.

VLS 80: Open‑ended multi‑asset fund with about 80% in global equities and 20% in bonds, aiming for long‑term growth with high equity exposure. So main risk is the equity markets. Hence the most risky of the three.

No one can foretell the future, so no one can tell what will give you the best return.

Rule of thumb: The higher the risk, the higher the expected return(but that's not guaranteed).

PS. To give financial advice in the UK requires having the appropriate qualifications. All you will get here & elsewhere is guidance & information.

Yeah I've got the discounting thing and see it's maybe not the most favourable time to buy right now but certainly not the worst time.But then is waiting for discounting pretty much the same as waiting for a stock price to go low? Like trying to time the market? Or is this fundamentally different?

2. Most active managers cannot, after charges & fees are deducted, consistently outperform a simple Major World Index like ACWI

So I see no reason to try to compete with the professionals with their vast resources or to give them my custom.

3. From what you post, we seem to be very different as far as investing is concerned.

I do not listen to "financial noise", I just do what interests me. So I no longer have a "perspective" to give you.

I now just do "Simple Investing" and am happy with the result it achieves.

You might like to give it a try.

4. SIMPLE INVESTING IN DETAIL (advantages, easy to understand & implement)(a) First watch this: https://www.kroijer.com/(b) Then read these:1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards