We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Equities exposure when approaching retirement age

Comments

-

Just checking my understanding of your analysis. If the market is down 25% in year 1 you reduce your drawdown by the same percentage and top up from the cash pot? The period in your graph would mean your cash pot would last beyond the point of positive returns as the maximum negative point is 45%? Would taking your withdrawals quarterly help smooth things during volatile times? I am just thinking that if you increase the cash pot to cover say 5 years (total) expenditure you could survive a ‘poor’ decade especially early on in retirement.Alexland said:

If you are 100% equities then a 20% drop that quickly recovers is a walk in the park compared to a 50% drop that takes more years than you have cash to recover. Below is the FTSE World with divi reinvestment from 2000-2010.ader42 said:My approach is to have 2 to 3 years income in cash, the rest 100% in equities with the intention of using guard rails (thereby reducing withdrawals) if necessary. Some use 3 buckets, I just use the two.

It’s not a matter of if there’ll be crashes during retirement, it will happen to all of us. But over time I’ve gotten used to yawning and doing nothing through biggish drops (20%).

Dragging out your 2-3 years of cash to last 6-7 years (while not knowing when the market will recover - it's still quite bad 4 years in) sounds like a pretty miserable period of retirement.

Then just after recovering from the dotcom bubble the GFC hits you.

The just over 30% gain at the end is spoilt by the 23% inflation during the decade and I was paying around 0.7% pa fund manager fees at the time so even if you managed to preserve the capital the spending power wouldn't have improved - a horrible and completely lost decade for the 100% equities investor.

A 10 year conventional gilt bought at the start of 2000 would have yielded 5.31% pa - a little more than now.

I have taken some of the recent gains from my global funds and invested in Investment Trusts with good long term dividend records. Their value will fall in a market crash but I am hoping will continue their payouts.0 -

Vanguard did an interesting research paper on Dynamic Spending a hybrid of the 2 that @OldScientist mentioned where modest affordable adjustment to the drawdown rate within single digit limits based on market performance improved portfolio longevity.Linton said:

Most expenditure is fixed in advance, you cant simply raise and lower it directly in response to movements in the market.

https://www.vanguard.co.uk/content/dam/intl/europe/documents/en/whitepapers/sustainable-spending-rates-in-turbulent-markets-uk-en-pro.pdf1 -

Sorry the graph was to highlight the problems with going 'all in' on equities (except for a very limited cash buffer) during a bad few years rather than proposing workarounds. In my mind it's pretty undesirable to sell any assets when their valuation is down and if you don't have any bonds it's a missed opportunity to get advantage from rebalancing (or over-rebalancing if you are so inclined).Just checking my understanding of your analysis. If the market is down 25% in year 1 you reduce your drawdown by the same percentage and top up from the cash pot? The period in your graph would mean your cash pot would last beyond the point of positive returns as the maximum negative point is 45%? Would taking your withdrawals quarterly help smooth things during volatile times? I am just thinking that if you increase the cash pot to cover say 5 years (total) expenditure you could survive a ‘poor’ decade especially early on in retirement.

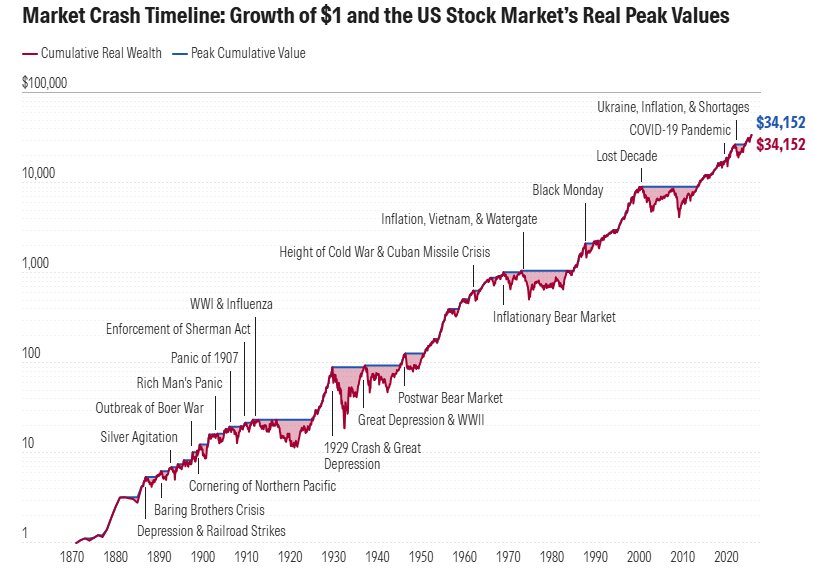

Here's a zoomed out, inflation adjusted, version highlighting how the bad periods for US equities happen quite frequently.

https://www.morningstar.com/economy/what-weve-learned-150-years-stock-market-crashes1 -

I have looked at the paper. Just a quick look made more difficult by doing it within the limitations of an iPad mini. So I may well have missed something but…Alexland said:

Vanguard did an interesting research paper on Dynamic Spending a hybrid of the 2 that @OldScientist mentioned where modest affordable adjustment to the drawdown rate within single digit limits based on market performance improved portfolio longevity.Linton said:

Most expenditure is fixed in advance, you cant simply raise and lower it directly in response to movements in the market.

https://www.vanguard.co.uk/content/dam/intl/europe/documents/en/whitepapers/sustainable-spending-rates-in-turbulent-markets-uk-en-pro.pdf

a) The analysis seems to be based on the great COVID crash of 2020. Does anyone in drawdown at that time remember it? Did you rethink your drawdown strategy and cut your expenditure, perhaps by immediately turning the central heating down by a degree? Or did you just carry on regardless? The 2000 .com crash could have been a better test case.

b) It is not clear to me by how much expenditure should have been cut and when.

The assumption seems to be that one is living a hand to mouth existence, withdrawing a predetermined amount of money after selling investments each month and spending it all. In practice if one manages one’s finances on the basis of a predetermined budget, one is likely to over-estimate the amount required and, if prudent, save the excess. Changing things by a single digit % is well within normal expenditure variability and the bounds of accuracy of the whole model.

0 -

My dividend income flow was hit hard by Covid-19 falling in 2020 to 60% of year end 2019 total and was nigh back up by end 2021. I've not got the records for 2008 but remember a raft of dividend cuts taking several yeas to recover. A cash pot of 2 years of expenditure could survive a 50% cut taking 3+ years to recover - that's as much of a disaster as I've planned. Inflation out pacing income growth is a risk too, my current plan is to take an income of ~10% more than my budgeted expenditure, if I end up with a surplus philanthropy, teats or more bonds/stocks.

If it is all merde I'll be forced to economise but I think the plan is sound and hope I don't.1 -

My experience was similar though less severe - the 2019 income fell by about 10% during 2020 and by a further 5% in 2021. However this was also a time during which there was a major reorganisation of the portfolio which could have led to missing out on some income. My income portfolio is 50% bonds and so was protected from the full effect on equities.kempiejon said:My dividend income flow was hit hard by Covid-19 falling in 2020 to 60% of year end 2019 total and was nigh back up by end 2021. I've not got the records for 2008 but remember a raft of dividend cuts taking several yeas to recover. A cash pot of 2 years of expenditure could survive a 50% cut taking 3+ years to recover - that's as much of a disaster as I've planned. Inflation out pacing income growth is a risk too, my current plan is to take an income of ~10% more than my budgeted expenditure, if I end up with a surplus philanthropy, teats or more bonds/stocks.

If it is all merde I'll be forced to economise but I think the plan is sound and hope I don't.

The mini crash did not have any affect on my expenditure since that was fully covered by my close to cash holdings. All income is paid into these holdings and all expenditure taken from them. So over time with income generally exceeding expenditure they increase in value. The near to cash holdings also pay for one-offs but COVID prevented any major holidays or house improvements.0 -

It's not that memorable for me compared to the Dotcom and GFC. Of course in accumulation with each crash the money at risk gets more significant. I do recall shortly before the covid lockdowns there were days when I noticed my accounts had dropped in one day more than I spent in a whole year which gave me pause for thought. I was heavy in equities at the time as cash was near zero return, the price of bonds was ready to pop and we weren't taking @DiggerUK seriously on gold.. For someone doing a heavy equities drawdown strategy and with no means to earn more money it might have given a few sleepless nights.Linton said:

The analysis seems to be based on the great COVID crash of 2020. Does anyone in drawdown at that time remember it?0 -

Reflecting on your earlier point I've never taken an Uber but the nearest I can think of is that Rachel Reeves thinks now is a good time for ISA investors to be encouraged to put their money in the stock market. Maybe that's a sign?Secret2ndAccount said:It will burst when your Uber driver is saying “Just buy anything because everything just goes up every day”, and I don’t think we’re there yet.

1 -

To link to the original topic, if one adopts the income based strategy there needs be no explicit derisking at retirement, just a reconfiguration to generate the income. The money not required to produce income can be left as 100% equity since it is not needed for short or medium term expenditure.

1 -

kempiejon said:My dividend income flow was hit hard by Covid-19 falling in 2020 to 60% of year end 2019 total and was nigh back up by end 2021. I've not got the records for 2008 but remember a raft of dividend cuts taking several yeas to recover. A cash pot of 2 years of expenditure could survive a 50% cut taking 3+ years to recover - that's as much of a disaster as I've planned. Inflation out pacing income growth is a risk too, my current plan is to take an income of ~10% more than my budgeted expenditure, if I end up with a surplus philanthropy, teats or more bonds/stocks.

If it is all merde I'll be forced to economise but I think the plan is sound and hope I don't.That's why I've based our retirement equity income on the AIC dividend heroes. We weren't investing in them before Covid, let alone the GFC. But the portfolio we now hold had a net increase in dividend income during both GFC and Covid. The increases didn't keep pace with inflation during those peirods, especially not in 2020-22, but every year the portfolio would have increased payments.Past performance is no guide to the future, etc, and we are giving up some current income for the expectation that future downturns won't affect us badly, but these investment trusts have a massive incentive to provide at least small annual increases - and means to do so - that individual companies or funds do not.But we also have substantial cash / gilt holdings that would fund us for many years even if dividend income fell dramatically - belts and braces!

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards