We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is II a no brainer

Comments

-

That's good as the wife's ISA is still with HL so can get this moved over.Pat38493 said:

I only managed to get the details this morning, but yes it seems so. For those of us who only have a SIPP with II today, the price is actually going up, but we will get "free" S&S ISA and GIA accounts whereas before we would have had to pay an extra £9 per month.michaels said:

The SIPP only price is increasing from 11.99 to 14.99?Pat38493 said:Also I have seen posts today that II are just about to change their pricing strategy which will result in a reduction in the fixed fee for most investors. It was quoted that the cost for a SIPP and ISA combo will go down from 21.99 per month to 14.99 per month. I have not received an email from them yet, maybe because I only have a SIPP with them at the moment. They have been sending out messages to existing customers today but I don't see any announcement on their website.

Still - keep in mind that there are a few platforms that offer S&S ISA with no fees at all e.g. T212 (but you can only use ETFs).0 -

Of course you can have a split of funds in a notional split.

As long as you know the amounts you can do it.

I have AJ Bell that’s 70% crystallised, I have half in a Short term cash fund and half in a Global tracker.

When the time comes to take income, I will most likely sell the cash fund, unless my equity fund has done exceptionally well and I sell some of that too.

What you sell to cash determines what you take and I imagine you can choose taxable drawdown or UFPLS etc.1 -

You can of course have a split, but the overall growth of your pot is shared proportionally between crystallised and uncrystallised based on your notional split. The cash allocation will dilute your annual gains in good years and reduce your losses in bad years.SVaz said:Of course you can have a split of funds in a notional split.

As long as you know the amounts you can do it.

I have AJ Bell that’s 70% crystallised, I have half in a Short term cash fund and half in a Global tracker.

When the time comes to take income, I will most likely sell the cash fund, unless my equity fund has done exceptionally well and I sell some of that too.

What you sell to cash determines what you take and I imagine you can choose taxable drawdown or UFPLS etc.3 -

Then I have just come to the horrible realisation that I should have transferred to Fidelity or HL instead because I’m not protected in the way I thought I was if there is a crash.I assumed having nearly 5 years in a STMMF meant that I’m covered for completely tax free income for 4 of those years.I am so, so annoyed.0

-

Ah, that kind of makes sense - thanks. I'm not bothered about separate investments for crystalised versus uncrystallised pots. so of no importance to me.MallyGirl said:

They definitely don't have separate pots - just a notional split. This means that you can't hold, for example, higher risk funds in uncrystallised and lower risk in crystallisedsausage_time said:

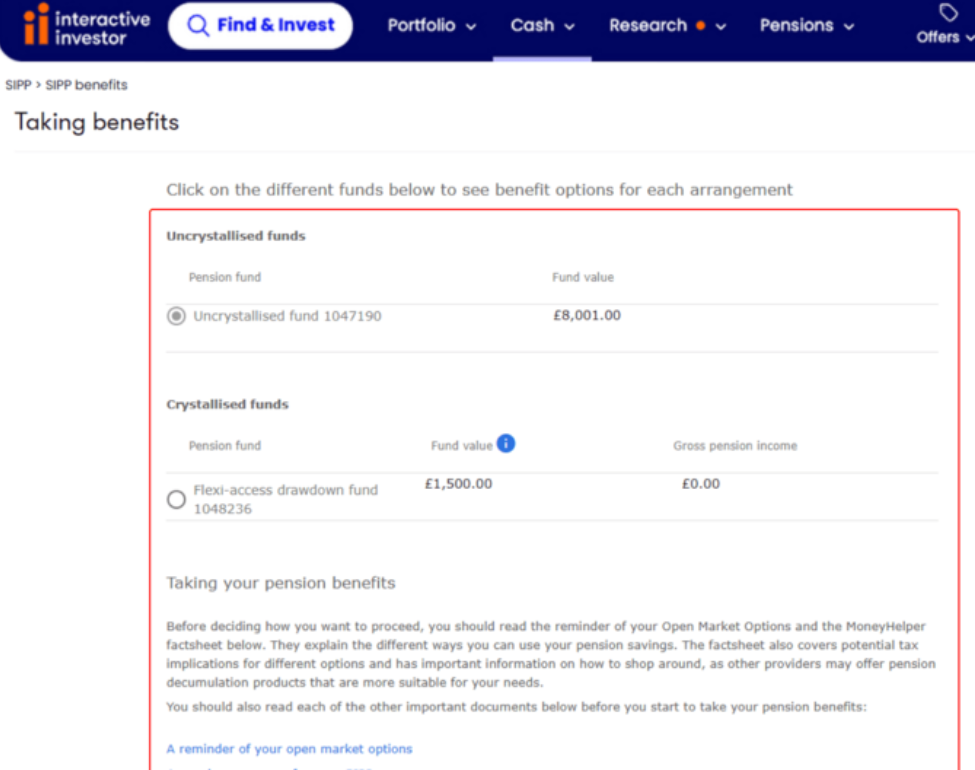

Can you perhaps clarify this? I have not yet taken anything from my ii pension, but the worked example on the web clearly shows two separate pots for crystallised and uncrystallised. (These are not my figures, just those in the on-line help),michaels said:II don't let you seperate crystalised and uncrystallised funds. Myself and another person I know have had real issues with the amount of time ii transfers take and that you can't drawdown whilst waiting for them to be finalised.

Am probably moving to AJ bell and putting same holdings in ETFs and bonds directly to minimise fees as they also let you trade linkers online.

I'm SIPP only so the increase in fees is not welcome. The "free" GIA and ISA is of no use to me - my T212 and Scottish Widows accounts are already free. But against that it looks like the new trading fees are flat. Before >£100k trades were £40 but it looks like that has gone? Not that I have many trades of that size!") I’m a Forum Ambassador and I support the Forum Team on the Credit Cards, Savings & investments, and Budgeting & Bank Accounts boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

I’m a Forum Ambassador and I support the Forum Team on the Credit Cards, Savings & investments, and Budgeting & Bank Accounts boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

I was paying a "employer negotiated" platform percentage fee of 0.16% on my 500k Aviva fund that was crazy and amounted to £67 per month PLUS inflated fund fees. I moved it to II for their flat rate fee of £12.99 - now increased to £14.99. I still have to pay fund fees and transaction fees but the latter are few and far between. I am quids in.3

-

Yeah this'll hit me too, going from £12.99 to £14.99, though they haven't sent me an email or message yet regarding this.

I use T212 for my ISA so so I won't be taking advantage of theirs.

I'm not complaining too much however, as I received the £1500 cashback, plus some Quidco (for transferring from Aviva) into my current account earlier this year.0 -

I doubt it will make a huge difference in the long run. I am in a similar situation as I just transferred an uncrystalized pot into an II drawdown.SVaz said:Then I have just come to the horrible realisation that I should have transferred to Fidelity or HL instead because I’m not protected in the way I thought I was if there is a crash.I assumed having nearly 5 years in a STMMF meant that I’m covered for completely tax free income for 4 of those years.I am so, so annoyed.

0 -

Regarding the uncrystallised and crystalised question, ii have this page where they also include several examples of how their notional split works:

ii.co.uk/ii-accounts/sipp/income-drawdown/notional-split0 -

thats helpful maxmarioxx and easier than I first thought. In reality I am unlikely to be overly actively dealing with the 2 elements so having a notional rather than actual split sort of works for me although I can see maybe not for others. Does that make sense?

Separate question and I know folk haven't a crystal ball but does the panel think there are likely to be inducements in the new year to move. A 1500 quid bribe sounds good if the product is already the one favoured0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards