We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

HMRC will stop cash-like investments in S&S ISAs

Comments

-

Let's see what happens. I'll not be surprised if cash-like investments (eg, MMF) are included in any interest trap. I'd hope gilt ladders are excluded.zagfles said:

The article does say "cash" not "cash-like". It would be ridiculous if people who'd say built a gilts ladder or used MM funds in a S&S ISA (because you can't buy them in cash ISAs) and who perhaps haven't used the cash ISA allowance at all, or maybe had only used £12k of it, were taxed on interest earned in a S&S ISA from investments that can't even be held in a cash ISA.MeteredOut said:

No big surprise here. Many of us surmised the result would be taxation of interest cash-like assets in S&S.m_c_s said:Leaks are starting to appear from initial talks with ISA providers:

https://www.politico.eu/article/hmrc-to-charge-isa-savers-22-percent-on-cash-interest-under-new-plans/

1. Current view from Government is a 22% flat-rate charge on any interest from cash holdings held in stocks and shares ISAs.

2. HMRC is also considering aligning the charge with income tax bands so could be a little more painful for those in higher rate tax bands.

3. “carve-outs” possible e.g. for cash waiting to be invested.

So it looks like the Government may not actually ban cash in S&S ISAs but rather there will be a sting if you do hold cash like investments.

Still early days but industry also stating the obvious that this is a tax grab in disguise.

But I think it would be grossly unfair if it was a flat rate and any such interest did not get relief under the £1K interest free savings and the £5K Starter Rate For Savings (where applicable).

It would just make it simple to report interest on cash-like savings in S&S ISAs as per non-ISA accounts and people pay tax at their marginal rate as they do today for non-ISA accounts. That would be my bet on where we land, but with a grace period of, say, 30 days, for cash waiting to be investmented.

You make a good point about those not using their £12K cash ISA allowance, and ideally they'd take that into account, but then it starts getting more complicated.1 -

The only cash like gilt in my view are T Bills.

They are not tradeable ( currently) and provide a fixed cash return after relatively short periods of 3 and 6 months ( much like fixed rate BS bonds).

All other gilts by contrast are tradeable. Price oscillates daily ( intra day). If you buy at the wrong price perfectly possible to make a capital loss if held to redemption, similarly can make a gain or loss if traded prior to redemption. Accrued income ( on purchase/sale) is a further complication that can be a hazard for fledgling investors. IL gilts can be particularly complex without guidance.

In fact if corporate bonds ( in general) are not to be caught by the 'cash like' moniker under the new rules ( why should they?), then UK gilts with their inherent ability to make capital losses in different scenarios and their own inherent complexities, have a lot more in common with corporate bonds than a vanilla bank deposit account.0 -

A current example of what could be possibly considered a 'cash like ' gilt -

https://www.hl.co.uk/shares/ipos-and-new-issues/3-month-uk-treasury-bill?lid=41c1klebia9v&campaign_name=Marketing+-+Treasury+Bills+-+Apps+Open+-+20260116+[TBOPEN1]&message_name=Email+[1]&theSource=EOR17&Override=11 -

There are one month (28 day) Treasury bills as well. The previous rules were that gilts and other bonds with less than five years to run on the day of purchase were considered 'cash like' and disallowed in S&S Isas*. IIRC this was to fit with the 5% test where there had to be a risk of at least a 5% capital loss at the time of investment with short durations not considered risky enough. I guess it'll depend on whether or not this test or one like it is reintroduced.poseidon1 said:The only cash like gilt in my view are T Bills.

They are not tradeable ( currently) and provide a fixed cash return after relatively short periods of 3 and 6 months ( much like fixed rate BS bonds).

All other gilts by contrast are tradeable. Price oscillates daily ( intra day). If you buy at the wrong price perfectly possible to make a capital loss if held to redemption, similarly can make a gain or loss if traded prior to redemption. Accrued income ( on purchase/sale) is a further complication that can be a hazard for fledgling investors. IL gilts can be particularly complex without guidance.

In fact if corporate bonds ( in general) are not to be caught by the 'cash like' moniker under the new rules ( why should they?), then UK gilts with their inherent ability to make capital losses in different scenarios and their own inherent complexities, have a lot more in common with corporate bonds than a vanilla bank deposit account.*But in theory were allowed in cash Isas if(!) the extract from Wikipedia below is correct.

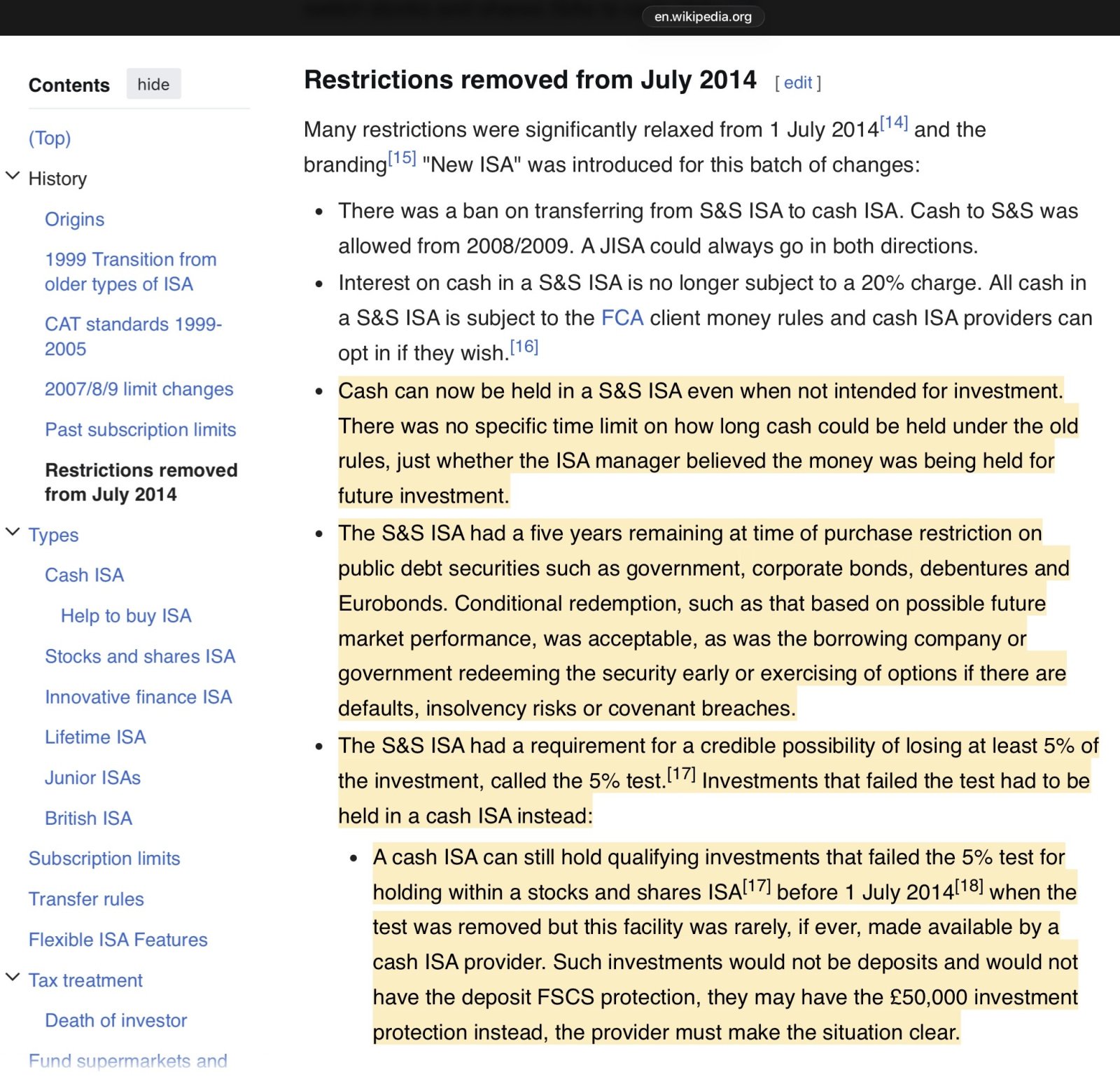

https://en.wikipedia.org/wiki/Individual_savings_account#:~:text=Cash%20can%20now%20be%20held,must%20make%20the%20situation%20clear. 3

3 -

Don't they need to get a wriggle on, if these changes are going to come in for the new tax year?masonic said:Sea_Shell said:I'm assuming from your post that they haven't been published yet.The consultation hasn't even started yet.In response to the earlier post about what to do, if you have a minimum you tend to keep in STMMF, then you can already get a competitive return in a cash ISA, so there's little reason not to partially transfer out if you can. Beyond that, things are unlikely to be worse than they were in the old days of lower limits for cash, where you could buy 5 year duration fixed interest and hold to maturity.A 5 year gilt pays a guaranteed return of 3.95% if held to maturity, and a 5 year index linked gilt pays around RPI+0.8%. What's not to like about that?

What's the latest date that this can start (assuming it still hasn't), and come into force in time?

Will we see the idea dropped, and put in the 'too hard' pile?

Sorry - is this not due to come in until 2027???

How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

The answer to your last question is yes, so that effectively answers the others!Sea_Shell said:

Don't they need to get a wriggle on, if these changes are going to come in for the new tax year?masonic said:Sea_Shell said:I'm assuming from your post that they haven't been published yet.The consultation hasn't even started yet.In response to the earlier post about what to do, if you have a minimum you tend to keep in STMMF, then you can already get a competitive return in a cash ISA, so there's little reason not to partially transfer out if you can. Beyond that, things are unlikely to be worse than they were in the old days of lower limits for cash, where you could buy 5 year duration fixed interest and hold to maturity.A 5 year gilt pays a guaranteed return of 3.95% if held to maturity, and a 5 year index linked gilt pays around RPI+0.8%. What's not to like about that?

What's the latest date that this can start (assuming it still hasn't), and come into force in time?

Will we see the idea dropped, and put in the 'too hard' pile?

Sorry - is this not due to come in until 2027???3 -

I would imagine there will be some time between the consultation and the budget to firm up on the details and give the better part of 6 months for HMRC to produce a revised list of ISA-eligible investments, and for providers to stop supporting S&S to cash ISA transfers.1

-

I'm wondering if they'll introduce the equivalent of Junior ISAs, i.e. Senior ISAs, for the over-65s, which will essentially be the current cash and S&S ones, with £20K annual allowances, unlimited transfers, and unrestricted investment choice within S&S?

A completely new product line (Middle-Aged ISAs?) would then be introduced for the majority, within which these new rules will apply....4 -

Surely they have to allow a couple of weeks of grace for cash. Simply selling a fund and buying another within an S&S ISA can take a few days. It would be harsh to tax that money, even though it would be a fairly small amount.0

-

boingy said:Surely they have to allow a couple of weeks of grace for cash. Simply selling a fund and buying another within an S&S ISA can take a few days. It would be harsh to tax that money, even though it would be a fairly small amount.Under the old regime, tax was deducted at source from interest paid on cash balances regardless of how long the cash was held. This could return. The challenge is that most interest is now paid gross, but there are still exceptions. It would be a pain to have to consider S&S ISAs when adding up taxable interest, especially as consolidated tax certificates are not always available immediately after the end of the tax year.An alternative would be to opt out of interest on cash balances, which I would take up if offered.4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards