We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Fund Selection

Comments

-

Sorry chiang_mai but I find your approach a bit complicated. This is what I do:

1. Cash: I have some cash in interest bearing bank accounts, some in premium bonds. Simple is good.

2. Gilt ladder: I have some gilts that get redeemed regularly to fund my monthly pension. My SIPP provider won't sell anything to pay my pension so the gilt redemptions / coupons mean I get my pension without doing anything. The ladder pretty much goes up to when I get my state pension in ten years time. I could improve returns by, for example, using money market funds. But I choose not to.

3. Equities: I'm not clever enough to beat the average, choose someone to beat the average for me, or to know what area / sector is going to do particularly well or not. So I have a single well diversified, low-cost, developed world, large company tracker. The only time I use a second tracker is when I think about the 30-day tax bed and breakfasting rules. This second one is pretty much the same as the first. Every now and then, when I think that the performance looks pretty good, I sell some equities and buy some more gilts for my ladder.

Unfortunately, I don't read investor magazines, have no gold, and only see stars on the mornings I do an early dog walk. I've not checked any PE ratios or betas and don't use an expected utility model based on prospect theory (although if I was not to old to learn something, it would probably be how to do that). In terms of bitcoin, the only thing I know is to put the phone down when someone tells me they have found my old account. Sorry. But it seems to work for me.

2 -

And that's just fine, there's no problem with that, for many years I did similar. For me, it was a gradual process that evolved slowly. I dound myself wondering what P/E ratio's meant and after I found out, realised it was sensible to use them and check them. Next it was capitalisation, so I checked that, after which I'd picked up on sectors and over concentration. Eventually, I got to a point where I was checking most things, quite naturally and quite easilty and quickly. The results are that checking these things is not a big overhead but I do now feel that I understand what I own and I sleep much better. I'm also better able to tilt my holdings and to find replacements and upgrades more easily. I'm now much better able to look at a potential fund and know what the writer is talking about and to spot danger and funds that are non-straters. It workks for me.Dead_keen said:Sorry chiang_mai but I find your approach a bit complicated. This is what I do:

1. Cash: I have some cash in interest bearing bank accounts, some in premium bonds. Simple is good.

2. Gilt ladder: I have some gilts that get redeemed regularly to fund my monthly pension. My SIPP provider won't sell anything to pay my pension so the gilt redemptions / coupons mean I get my pension without doing anything. The ladder pretty much goes up to when I get my state pension in ten years time. I could improve returns by, for example, using money market funds. But I choose not to.

3. Equities: I'm not clever enough to beat the average, choose someone to beat the average for me, or to know what area / sector is going to do particularly well or not. So I have a single well diversified, low-cost, developed world, large company tracker. The only time I use a second tracker is when I think about the 30-day tax bed and breakfasting rules. This second one is pretty much the same as the first. Every now and then, when I think that the performance looks pretty good, I sell some equities and buy some more gilts for my ladder.

Unfortunately, I don't read investor magazines, have no gold, and only see stars on the mornings I do an early dog walk. I've not checked any PE ratios or betas and don't use an expected utility model based on prospect theory (although if I was not to old to learn something, it would probably be how to do that). In terms of bitcoin, the only thing I know is to put the phone down when someone tells me they have found my old account. Sorry. But it seems to work for me.1 -

That sounds a bit incongruent with:chiang_mai said:

... for many years I did similar. For me, it was a gradual process that evolved slowly. I dound myself wondering what P/E ratio's meant and after I found out, realised it was sensible to use them and check them. Next it was capitalisation, so I checked that

But I don't have a banking background so what do I know! Anyway, this aspect is the very important so keep going:chiang_mai said:

I come from a financial services, Big 4 and banking background so this kind of effort is not new to me.

0 -

I am simply interested in the information and thinking processes in Chiang_Mai’s posts. I recognise that I have a very rudimentary understanding of investing and I very much appreciate the insights that their posts offer. There is nothing dangerous in being an interested and engaged beginner who welcomes a generously offered discussion.Bostonerimus1 said:

If you think that such detailed analysis will help you then go ahead. I've concluded that it's just as likely to hurt as help. People love to hang onto the idea that they can beat the markets in some deterministic way and we get many posts from people who have excellent returns. However, we seldom see posts from people who's analysis and active management have caused them to lag the markets; they certainly exist but might be embarrassed. Long ago I decided that the only statistics to use when investing are long term and even they are backwards looking so proceed with caution. It's good to have an understanding of funds at a basic level, but beware of over interpretation and using dubious mathematics to reinforce your assumptions and desires.ShinyStarlight1 said:

Speaking as someone who understands very little about investing, and am unfamiliar with most of the terminology, I really appreciate the clarity and detail of Chiang_Mai’s posts. They are helping me to learn by demystifying the decision-making process. I enjoy the opportunity of looking under the bonnet and gradually teasing out the tangle beneath it. I also appreciate the effort and generosity that such detailed posts require.Bostonerimus1 said:

Many people struggle with percentages, compound interest and the difference between tax-free and tax deferred. It's good that you are sharing your approach, but it will be too much for most peoplechiang_mai said:

Your analogies are a bit extreme but I get your point. Whether or not it's approppriate to tilt more towards being a nerd, depends on how comforrtable they are putting all their trust and faith in one or two trackers and handing all control and responsibility for your financial future, to the likes of Vanguard et al. But I suppose that approach has always worked well in the past so it must continue to work well in the future, right!Bostonerimus1 said:

Yes it's good to understand what's in the black box, but for most people they simply don't need to and most importantly don't want to understand the workings of their funds. For those reasons we have multi-asset funds and "Lazy Portfolios". There will be some nerds, and I use the term with admiration and affection, that do want to understand all the "nuts and bolts", but that's simply not appropriate for most people. It's like some one buying a drone and needing or wanting to know the PID/PDF servo control on the propeller motors. Or someone with diabetes wanting to understand the PI3K/AKT pathway.chiang_mai said:I don't know why you'd be so astonished, it's an obvious conclusion to draw! Forums such as these are often prone to members trying to maintain their "expert" status without ever putting forth anything really useful. And to be clear, I'm not courting views, it's more that I'm curious to see who actually understands what! It's easy enough to buy a global tracker or three and using the right lingo, say you understand it all. On the other hand, the likes of Morningstar gives us all these metrics and analytical data, it seems counter productive not to at least understand what it all means and wherever possible, use it. Of course you don't have to do that and chances are you may even obtain the same result, more easily, if you take the simple approach. But there again you may not. My experience is that it's better to understand the mechanics of what's under the hood, at a detail level, in whatever I do in life and investing is no different, it helps when you break down in the middle of nowhere.0 -

I can see where you might think that. Financial Services and banking is a huge sector, being in it doesn't mean that everyone employed in it is an investment guru. My work background is in IT/Systems/technology and management consulting, in the Financial services sector....I managed a US banks IT department for many years, my experience is far removed from traditional banking and finance. But I am accustomed to analysis, being around numbers and the terminology.Dead_keen said:

That sounds a bit incongruent with:chiang_mai said:

... for many years I did similar. For me, it was a gradual process that evolved slowly. I dound myself wondering what P/E ratio's meant and after I found out, realised it was sensible to use them and check them. Next it was capitalisation, so I checked that

But I don't have a banking background so what do I know! Anyway, this aspect is the very important so keep going:chiang_mai said:

I come from a financial services, Big 4 and banking background so this kind of effort is not new to me.

I started investing eight years ago as a hobby here in Thailand. An expat friend is a real mainstream banker and ex CFO of a major bank, he taught me some of the basics and was available to ask questions. The catalyst for getting involved in the first place was the realisation thjat I had been conned by a UK IFA during a work assignement there 16 years ago. He sold me a SIPP and was paid for his work both by me and the platform. Two years later he sold his business and didn't tell me. The buyer, a big Fin Serv conmpany, let my small SIPP fall into a black hole, unattended. Five years had passed before I twigged what was happening and whilst I giot some compensation from them, I decided then that I needed to take control of matters. It took a while longer before I realised that the platform didn't really allow retail investors, only IFA's and was ripping me off once again. At that point I discovered Hargreaves and made the switch.0 -

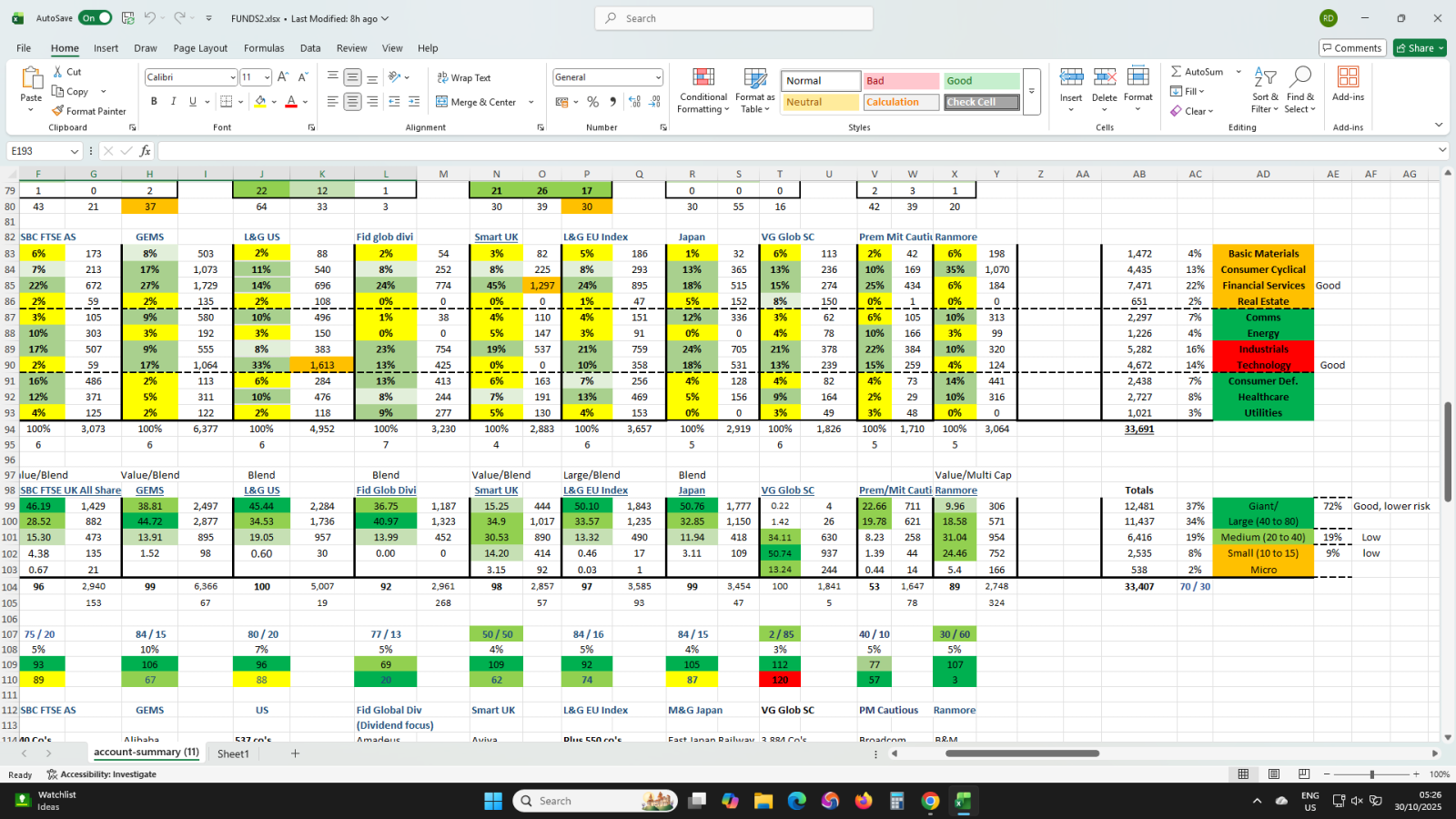

A short note about investment sectors.

There are eleven investment sectors and these are shown for every equities fund in Morningstar profiles, along with the percentage invested in each of them, by the relevant fund. Yahoo Finance reports daily volumes and activity in each sector https://finance.yahoo.com/sectors/

Three or four of the sectors aren't used very much and are under utilised by most funds, perhaps because they are specialist, seasonal or there may be another reason. From my perspective, I tend to mostly disregrd Real Estate, Basic Materials, Utilities and Energy and focus on the remaining sectors. I try to ensure that funds I buy are spread acrosss those remaining seven sectors and not concentrated or too low. That involves constructing a spread sheet with eleven rows and entries for each fund....it's simple and quick enough to do. When you're finished you'll see what the overall portfolio view looks like and which sectors are overloaded or need rto be smoothed out. Below is a screen shot of one such effort from one of my portfolio's which I update monthly or so, The problem is that not all sectors are equall. If, for example, all the profit is being made in say Financial Services and you're invested in Consumer Cyclical, you're not going to make very much. Ditto if all the losses are in say Technology and you're overweight in that sector, you're going to get burned. Sector Investing is a style of investing in its own right but I don't recommend using sectors alone as a guide, it's just one of the many tools or factors you can utilise.

1 -

This is a brain dump for interested beginners, just to provide a starting point of some basics. More experienced and knowledgable investers can of course jump in and correct or add to, as required.

The style boxes used by Morningstar on their funds pages are really useful. You can see at a glance what investment style is being used by the fund in equities or bond funds, eg Value Growth or Blend. The other set of numbers on the same page show the capitalization ratio of the fund, eg, Percentage invested in Giant, Large, Medium and Small companies.

Giant and Large companies are less volatile than Medium and Small companies but Medium and Small companies are where the big money can be made. The trade off here should be obvious….if you want low risk and greater stability, go for Giant and Large companies but be prepared to see lower returns. If you want to make money then you have to take a risk and that means medium and small companies.

Exactly how you divide your investment between the two very distinct sizes of company, will require some thought and analysis….damn, there’s that word again, I’m sorry but you just have to think about how much risk you are prepared to take, versus the return you want to make. If you’re older, you probably want stability and certainty, if you’re younger you may be prepared to take more risk because you have the years ahead of you to recover if things turn sour. Everyone else is in-between.

As you can see from the spreadsheet, I’m at 72% Giant and Large, 19% Medium and 9% small. I can tweak those figures easily by buying and selling what I already own, just by looking at the fund sector allocation tables.

Choosing between Value, Blend or Growth companies once again requires some thought and analysis, what do you want, what’s your risk profile and tolerance? Value investments are those that go in search of companies to exploit existing opportunities, eg monetize and release value from existing products and services. Perhaps a company has a product that is new to the market that the Fund Manager believes will really take off, once people see it. Growth on the other hand is the often slow lumbering process of getting bigger by doing business every day and also includes growth through merger and acquisition. Blend is a combination of those two types.

Here’s a style box example from a Morningstar fund:

Artemis SmartGARP UK Eq C Acc GBP Fund Portfolio Review | Morningstar UK

Just underneath the above, on the same page, see also Market Cap and the capitalisation ratio’s.

1 -

It's good to learn, but don't be seduced by mathematical metrics. Many PhDs have tried and failed to play the markets. If you want to do well it's better to maximize your probability of success rather than trying to maximize your return and that is done with a portfolio that has a sensible balance of risk and return and too much "user intervention" can greatly increase risk.ShinyStarlight1 said:

I am simply interested in the information and thinking processes in Chiang_Mai’s posts. I recognise that I have a very rudimentary understanding of investing and I very much appreciate the insights that their posts offer. There is nothing dangerous in being an interested and engaged beginner who welcomes a generously offered discussion.Bostonerimus1 said:

If you think that such detailed analysis will help you then go ahead. I've concluded that it's just as likely to hurt as help. People love to hang onto the idea that they can beat the markets in some deterministic way and we get many posts from people who have excellent returns. However, we seldom see posts from people who's analysis and active management have caused them to lag the markets; they certainly exist but might be embarrassed. Long ago I decided that the only statistics to use when investing are long term and even they are backwards looking so proceed with caution. It's good to have an understanding of funds at a basic level, but beware of over interpretation and using dubious mathematics to reinforce your assumptions and desires.ShinyStarlight1 said:

Speaking as someone who understands very little about investing, and am unfamiliar with most of the terminology, I really appreciate the clarity and detail of Chiang_Mai’s posts. They are helping me to learn by demystifying the decision-making process. I enjoy the opportunity of looking under the bonnet and gradually teasing out the tangle beneath it. I also appreciate the effort and generosity that such detailed posts require.Bostonerimus1 said:

Many people struggle with percentages, compound interest and the difference between tax-free and tax deferred. It's good that you are sharing your approach, but it will be too much for most peoplechiang_mai said:

Your analogies are a bit extreme but I get your point. Whether or not it's approppriate to tilt more towards being a nerd, depends on how comforrtable they are putting all their trust and faith in one or two trackers and handing all control and responsibility for your financial future, to the likes of Vanguard et al. But I suppose that approach has always worked well in the past so it must continue to work well in the future, right!Bostonerimus1 said:

Yes it's good to understand what's in the black box, but for most people they simply don't need to and most importantly don't want to understand the workings of their funds. For those reasons we have multi-asset funds and "Lazy Portfolios". There will be some nerds, and I use the term with admiration and affection, that do want to understand all the "nuts and bolts", but that's simply not appropriate for most people. It's like some one buying a drone and needing or wanting to know the PID/PDF servo control on the propeller motors. Or someone with diabetes wanting to understand the PI3K/AKT pathway.chiang_mai said:I don't know why you'd be so astonished, it's an obvious conclusion to draw! Forums such as these are often prone to members trying to maintain their "expert" status without ever putting forth anything really useful. And to be clear, I'm not courting views, it's more that I'm curious to see who actually understands what! It's easy enough to buy a global tracker or three and using the right lingo, say you understand it all. On the other hand, the likes of Morningstar gives us all these metrics and analytical data, it seems counter productive not to at least understand what it all means and wherever possible, use it. Of course you don't have to do that and chances are you may even obtain the same result, more easily, if you take the simple approach. But there again you may not. My experience is that it's better to understand the mechanics of what's under the hood, at a detail level, in whatever I do in life and investing is no different, it helps when you break down in the middle of nowhere.

There are whole magazines and websites dedicated to "Seeking Alpha" with people anxious to beat some benchmark and the people who do best out of it all are the people selling the methods and schemes. Coming from a maths background I've read a lot of the papers on "efficient markets" and then the collapse of Long Term Capital Management and reading the simple application of "Modern Portfolio Theory" advocated by Bogleheads convinced me to stick to simple index investing. I see the uncertainties of active investing and getting too wrapped up in the details of companies and funds as a negative, not a positive. So definitely learn, but be careful how you apply that knowledge.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

I agree with those sentiments.....let me reinforce that this is not about trying to beat the markets, it's about understanding the products and markets we are invested in, why and how, either a little bit or a lot. From my perspective, a person can only adopt, "a portfolio that has a sensible balance of risk and return", if they understand what it contains and why. The alternative is to put blind faith in the people you are buying products from and hope that it will be OK. There are some highly educated and trained Fund Managers out there who are very capable managers of funds. It's worth reading the bio's of the the various FM's as a part of the fund selection process. It has already been agreed that no FM beats the market 100% of the time but that's not the objective nor a requirement.Bostonerimus1 said:

It's good to learn, but don't be seduced by mathematical metrics. Many PhDs have tried and failed to play the markets. If you want to do well it's better to maximize your probability of success rather than trying to maximize your return and that is done with a portfolio that has a sensible balance of risk and return and too much "user intervention" can greatly increase risk.

There are whole magazines and websites dedicated to "Seeking Alpha" with people anxious to beat some benchmark and the people who do best out of it all are the people selling the methods and schemes. Coming from a maths background I've read a lot of the papers on "efficient markets" and then the collapse of Long Term Capital Management and reading the simple application of "Modern Portfolio Theory" advocated by Bogleheads convinced me to stick to simple index investing. I see the uncertainties of active investing and getting too wrapped up in the details of companies and funds as a negative, not a positive. So definitely learn, but be careful how you apply that knowledge.0 -

I agree that it's easy to compare individual funds.chiang_mai said:

I'm not sure I understand. Every fund already has its own benchmark, against which its performance is measured and reported every which way by a number of sites....Trustnet is particularly useful in this respect. The relevant benchamrk can always be found in the funds document.leosayer said:Measuring the performance of your own fund selection and comparing to one or many benchmarks is not a trivial exercise as it requires a level of record keeping that is more than most are willing or able to do.

I'm thinking more of comparing your own portfolio performance against that of a benchmark, particularly if you want to track different slices such as fixed income and equity portions.

To do so requires keeping records of all holdings, transactions and values over time.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards