We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Fund Selection

Comments

-

I think the issue is that we aren't going to be able to figure out what will work well in the future, however much research we do. The most we can do is make a plan that will survive a wide range of eventualities. Making appropriate choices between asset classes at different stages of life is a very large part of that, and this can be fulfilled by the various multi-asset funds that are out there, albeit it does require an occasional move between them. There are ways you can finesse the approach, such as buying individual gilts matched to your specific needs instead of a bond fund, but the case for this is arguable and depends on the economic climate of the time. The big failure case of course was for those in very "low risk" multi-asset funds around the time interest rates started rising. That was something that could have been avoided through understanding of the asset class.chiang_mai said:

Your analogies are a bit extreme but I get your point. Whether or not it's approppriate to tilt more towards being a nerd, depends on how comforrtable they are putting all their trust and faith in one or two trackers and handing all control and responsibility for your financial future, to the likes of Vanguard et al. But I suppose that approach has always worked well in the past so it must continue to work well in the future, right!Bostonerimus1 said:

Yes it's good to understand what's in the black box, but for most people they simply don't need to and most importantly don't want to understand the workings of their funds. For those reasons we have multi-asset funds and "Lazy Portfolios". There will be some nerds, and I use the term with admiration and affection, that do want to understand all the "nuts and bolts", but that's simply not appropriate for most people. It's like some one buying a drone and needing or wanting to know the PID/PDF servo control on the propeller motors. Or someone with diabetes wanting to understand the PI3K/AKT pathway.chiang_mai said:I don't know why you'd be so astonished, it's an obvious conclusion to draw! Forums such as these are often prone to members trying to maintain their "expert" status without ever putting forth anything really useful. And to be clear, I'm not courting views, it's more that I'm curious to see who actually understands what! It's easy enough to buy a global tracker or three and using the right lingo, say you understand it all. On the other hand, the likes of Morningstar gives us all these metrics and analytical data, it seems counter productive not to at least understand what it all means and wherever possible, use it. Of course you don't have to do that and chances are you may even obtain the same result, more easily, if you take the simple approach. But there again you may not. My experience is that it's better to understand the mechanics of what's under the hood, at a detail level, in whatever I do in life and investing is no different, it helps when you break down in the middle of nowhere.1 -

My last post for the day, a quick word about indicies falling faster than managed funds.

The Artemis Smartgarp European Equities fund (for example) has an upside capture ratio of 109 and a downside capture ratio of -9.

The L&G Europe index fund (for example) has an upside of 92 and a downside of 74."Upside Capture Ratio measures a manager's performance in up-markets relative to the index. A value over 100 indicates that an investment has outperformed the benchmark during periods of positive returns for the benchmark.

Downside Capture Ratio measures the manager's performance in down-markets relative to the index. A value of less than 100 indicates that an investment has lost less than its benchmark when the benchmark has been in the red".

1 -

I've never put much stock in horoscopes, numerology or the attempts of people to read the tea leaves of the markets.chiang_mai said:My last post for the day, a quick word about indicies falling faster than managed funds.

The Artemis Smartgarp European Equities fund (for example) has an upside capture ratio of 109 and a downside capture ratio of -9.

The L&G Europe index fund (for example) has an upside of 92 and a downside of 74."Upside Capture Ratio measures a manager's performance in up-markets relative to the index. A value over 100 indicates that an investment has outperformed the benchmark during periods of positive returns for the benchmark.

Downside Capture Ratio measures the manager's performance in down-markets relative to the index. A value of less than 100 indicates that an investment has lost less than its benchmark when the benchmark has been in the red".

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

These are mathematical performance measurements, not guess work!Bostonerimus1 said:

I've never put much stock in horoscopes, numerology or the attempts of people to read the tea leaves of the markets.chiang_mai said:My last post for the day, a quick word about indicies falling faster than managed funds.

The Artemis Smartgarp European Equities fund (for example) has an upside capture ratio of 109 and a downside capture ratio of -9.

The L&G Europe index fund (for example) has an upside of 92 and a downside of 74."Upside Capture Ratio measures a manager's performance in up-markets relative to the index. A value over 100 indicates that an investment has outperformed the benchmark during periods of positive returns for the benchmark.

Downside Capture Ratio measures the manager's performance in down-markets relative to the index. A value of less than 100 indicates that an investment has lost less than its benchmark when the benchmark has been in the red".

1 -

Whilst I broadly agree with the sentiment, I do think there may be a middle ground between blindly accepting a tracker solution and becomming totally nerd like and analysing every metric. At a minimum:masonic said:

I think the issue is that we aren't going to be able to figure out what will work well in the future, however much research we do. The most we can do is make a plan that will survive a wide range of eventualities. Making appropriate choices between asset classes at different stages of life is a very large part of that, and this can be fulfilled by the various multi-asset funds that are out there, albeit it does require an occasional move between them. There are ways you can finesse the approach, such as buying individual gilts matched to your specific needs instead of a bond fund, but the case for this is arguable and depends on the economic climate of the time. The big failure case of course was for those in very "low risk" multi-asset funds around the time interest rates started rising. That was something that could have been avoided through understanding of the asset class.

1)Ensure there is no sector concentration, that at least 50% of all sectors are represented in a fund and that no sector has more than say 25% (?) invested in it.

2) The ratio of small medium, and large caps is planned portfolio wide, rather than just being accepted for what it turns out to be.

3) Geographic percentages are established in advance, rather than accepted defacto.

4) Risk levels are understood, using whatever risk measurements you prefer and that portfolio's are measured overall.

Thereafter it's a matter of personal preference as to how much more time and energy you want to spend researching metrics and crunching numbers.

1 -

...and our disagreement on the value of such "mathematical performance measurements" is the reason why we approach investing differently.chiang_mai said:

These are mathematical performance measurements, not guess work!Bostonerimus1 said:

I've never put much stock in horoscopes, numerology or the attempts of people to read the tea leaves of the markets.chiang_mai said:My last post for the day, a quick word about indicies falling faster than managed funds.

The Artemis Smartgarp European Equities fund (for example) has an upside capture ratio of 109 and a downside capture ratio of -9.

The L&G Europe index fund (for example) has an upside of 92 and a downside of 74."Upside Capture Ratio measures a manager's performance in up-markets relative to the index. A value over 100 indicates that an investment has outperformed the benchmark during periods of positive returns for the benchmark.

Downside Capture Ratio measures the manager's performance in down-markets relative to the index. A value of less than 100 indicates that an investment has lost less than its benchmark when the benchmark has been in the red".

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

We don't necessarily disagree, I have already said that if the tracker approach is what makes you happy, I have no issue with that. But I do object to anyone equating upside/dopwnside capture ratio's, and any other mathematical measurement, with reading tea leaves, that is a gross misreprentation of the facts.Bostonerimus1 said:

...and our disagreement on the value of such "mathematical performance measurements" is the reason why we approach investing differently.

These are mathematical performance measurements, not guess work!

I've never put much stock in horoscopes, numerology or the attempts of people to read the tea leaves of the markets.1 -

We do disagree. I won't tell you what to do, but I believe that your approach is not appropriate for most people and can be misleading.chiang_mai said:

We don't necessarily disagree, I have already said that if the tracker approach is what makes you happy, I have no issue with that. But I do object to anyone equating upside/dopwnside capture ratio's, and any other mathematical measurement, with reading tea leaves, that is a gross misreprentation of the facts.Bostonerimus1 said:

...and our disagreement on the value of such "mathematical performance measurements" is the reason why we approach investing differently.

These are mathematical performance measurements, not guess work!

I've never put much stock in horoscopes, numerology or the attempts of people to read the tea leaves of the markets.And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

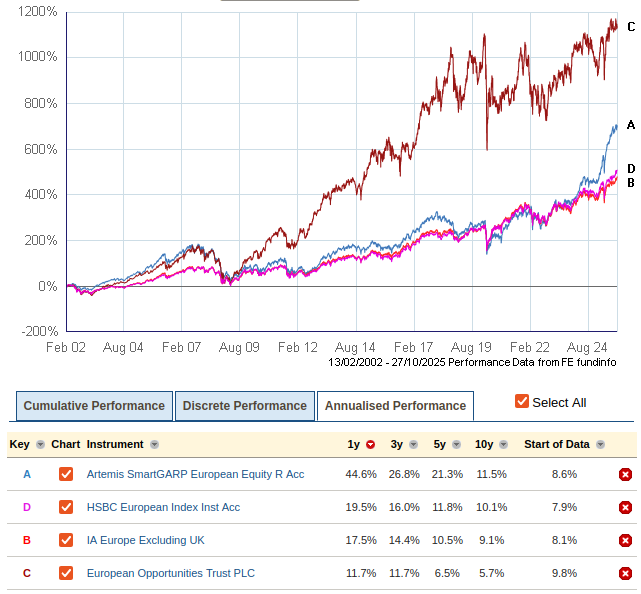

On the subject of capture ratios, I've realised that I've been quite remiss in not mentioning a key part of my process, which is to put contender funds up on a performance chart zoomed out to show as much history as possible:

Please forgive the switch from the L&G tracker fund to HSBC's equivalent, but this is the only one I'm aware of that's been around long enough to make the comparison.One issue I've found when looking at various metrics is that they are often quoted over short timeframes and are therefore embedded with recency bias. A key example is the "3 year volatility" measure found on Trustnet's comparison report. Such a measure is only really informative if it coincides with a period where the VIX index includes one of its periodic spikes. Otherwise, volatility when markets are generally calm and optimistic can be very misleading. I wonder if something similar has happened for the capture ratios quoted above.When I look at the long term performance of the SmartGARP fund, the first thing that strikes me is that it goes through periods of exuberant growth, followed by periods of decline that knock it back to the level of the less volatile index tracking fund or just above. A good thing about such a fund is that it is a largely mechanical and constant selection process going on under the hood, so manager risk is low. It is not going to change its style or try to second guess the market. I would liken it to a tracker in some respects, but it is making its own index, not too dissimilar to the smart beta ETFs one could buy. There is some evidence that it may not entirely give up its gains when held from trough to trough, but there seems to be a 20 year period starting from Feb 2022 (the earliest timepoint I could zoom out to) where it underperformed the tracker fund with greater overall volatility (I cannot see how this can be reconciled with a downside capture ratio of -9). From 2022 to present, it appears to have entered another of its periods of exuberance, and so if the pattern repeats, this is likely to be followed by another low performance period. Perhaps this is a good time to exit this fund or at least rebalance to lock in short term gains, which history teaches us are not retained by the fund over the long term.For comparison, I thought I'd throw in a similar fund I held in the past EOT, which was JEO in my day. Very similar performance between the Dotcom crash to global financial crisis, but this one really soared coming out of that. I held for most of the 2010s, but as my attitude to risk evolved I gradually rebalanced this into an index fund, completing that move before it changed its name in 2019. I think I got a lucky break as its 10 year performance has been quite dire. But this is an example of the sort of fund that someone who is young with a large appetite and capacity for risk could opt for, when managing the £10ks rather than £100ks later in life where capital preservation becomes a greater goal. I'm not at a stage of my life where that is attractive to me any longer, but don't see any issue with someone pursuing such a strategy at the appropriate time and with their eyes wide open.Turning attention to the annualised performance, one only needs to look at the 1 year vs long-term return to see that we are a localised high growth part of the cycle, and this is most extreme in the SmartGARP fund, whereas EOT seems to have lost its way recently, significantly underperforming both tracker and sector average over 1, 3, 5 and 10 years. Going to show that getting a good outcome from such funds is largely reliant on market timing and therefore luck. At this point, I'm happy to capture the ~8% long term return of the market as opposed to something slightly higher with a wilder ride.1

Please forgive the switch from the L&G tracker fund to HSBC's equivalent, but this is the only one I'm aware of that's been around long enough to make the comparison.One issue I've found when looking at various metrics is that they are often quoted over short timeframes and are therefore embedded with recency bias. A key example is the "3 year volatility" measure found on Trustnet's comparison report. Such a measure is only really informative if it coincides with a period where the VIX index includes one of its periodic spikes. Otherwise, volatility when markets are generally calm and optimistic can be very misleading. I wonder if something similar has happened for the capture ratios quoted above.When I look at the long term performance of the SmartGARP fund, the first thing that strikes me is that it goes through periods of exuberant growth, followed by periods of decline that knock it back to the level of the less volatile index tracking fund or just above. A good thing about such a fund is that it is a largely mechanical and constant selection process going on under the hood, so manager risk is low. It is not going to change its style or try to second guess the market. I would liken it to a tracker in some respects, but it is making its own index, not too dissimilar to the smart beta ETFs one could buy. There is some evidence that it may not entirely give up its gains when held from trough to trough, but there seems to be a 20 year period starting from Feb 2022 (the earliest timepoint I could zoom out to) where it underperformed the tracker fund with greater overall volatility (I cannot see how this can be reconciled with a downside capture ratio of -9). From 2022 to present, it appears to have entered another of its periods of exuberance, and so if the pattern repeats, this is likely to be followed by another low performance period. Perhaps this is a good time to exit this fund or at least rebalance to lock in short term gains, which history teaches us are not retained by the fund over the long term.For comparison, I thought I'd throw in a similar fund I held in the past EOT, which was JEO in my day. Very similar performance between the Dotcom crash to global financial crisis, but this one really soared coming out of that. I held for most of the 2010s, but as my attitude to risk evolved I gradually rebalanced this into an index fund, completing that move before it changed its name in 2019. I think I got a lucky break as its 10 year performance has been quite dire. But this is an example of the sort of fund that someone who is young with a large appetite and capacity for risk could opt for, when managing the £10ks rather than £100ks later in life where capital preservation becomes a greater goal. I'm not at a stage of my life where that is attractive to me any longer, but don't see any issue with someone pursuing such a strategy at the appropriate time and with their eyes wide open.Turning attention to the annualised performance, one only needs to look at the 1 year vs long-term return to see that we are a localised high growth part of the cycle, and this is most extreme in the SmartGARP fund, whereas EOT seems to have lost its way recently, significantly underperforming both tracker and sector average over 1, 3, 5 and 10 years. Going to show that getting a good outcome from such funds is largely reliant on market timing and therefore luck. At this point, I'm happy to capture the ~8% long term return of the market as opposed to something slightly higher with a wilder ride.1 -

I agree with regard to Smartgarp Europe, it has been very volatile at times and I also agree that it does tend to spike. It was for those reasons that I very recently came out of the European fund, in favour of the L&G Europe tracker. I continue to hold the Smartgarp UK and GEMS funds though. If you are prepared to put in the effort and time, there are periods of over performance that can be rewarding, albeit hard work at times. I've generally come down in favour of preservation at this time and have conciously lowered my risk levels across the board and Smartgarp Europe was a prime candidate in that cull.masonic said:On the subject of capture ratios, I've realised that I've been quite remiss in not mentioning a key part of my process, which is to put contender funds up on a performance chart zoomed out to show as much history as possible:Please forgive the switch from the L&G tracker fund to HSBC's equivalent, but this is the only one I'm aware of that's been around long enough to make the comparison.One issue I've found when looking at various metrics is that they are often quoted over short timeframes and are therefore embedded with recency bias. A key example is the "3 year volatility" measure found on Trustnet's comparison report. Such a measure is only really informative if it coincides with a period where the VIX index includes one of its periodic spikes. Otherwise, volatility when markets are generally calm and optimistic can be very misleading. I wonder if something similar has happened for the capture ratios quoted above.When I look at the long term performance of the SmartGARP fund, the first thing that strikes me is that it goes through periods of exuberant growth, followed by periods of decline that knock it back to the level of the less volatile index tracking fund or just above. A good thing about such a fund is that it is a largely mechanical and constant selection process going on under the hood, so manager risk is low. It is not going to change its style or try to second guess the market. A would liken it to a tracker in some respects, but it is making its own index, not too dissimilar to the smart beta ETFs one could buy. There is some evidence that it may not entirely give up its gains when held from trough to trough, but there seems to be a 20 year period starting from Feb 2022 (the earliest timepoint I could zoom out to) where it underperformed the tracker fund with greater overall volatility (I cannot see how this can be reconciled with a downside capture ratio of -9). From 2022 to present, it appears to have entered another of its periods of exuberance, and so if the pattern repeats, this is likely to be followed by another low performance period. Perhaps this is a good time to exit this fund or at least rebalance to lock in short term gains, which history teaches us are not retained by the fund over the long term.For comparison, I thought I'd throw in a similar fund I held in the past EOT, which was JEO in my day. Very similar performance between the Dotcom crash to global financial crisis, but this one really soared coming out of that. I held for most of the 2010s, but as my attitude to risk evolved I gradually rebalanced this into an index fund, completing that move before it changed its name in 2019. I think I got a lucky break as its 10 year performance has been quite dire. But this is an example of the sort of fund that someone who is young with a large appetite and capacity for risk could opt for, when managing the £10ks rather than £100ks later in life where capital preservation becomes a greater goal. I'm not at a stage of my life where that is attractive to me any longer, but don't see any issue with someone pursuing such a strategy at the appropriate time and with their eyes wide open.Turning attention to the annualised performance, one only needs to look at the 1 year vs long-term return to see that we are a localised high growth part of the cycle, and this is most extreme in the SmartGARP fund, whereas EOT seems to have lost its way recently, significantly underperforming both tracker and sector average over 1, 3, 5 and 10 years. Going to show that getting a good outcome from such funds is largely reliant on market timing and therefore luck. At this point, I'm happy to capture the ~8% long term return of the market as opposed to something slightly higher with a wilder ride.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards