We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Newbie Pension Help.

Fitzy712

Posts: 6 Forumite

Hi Guys, would appreciate your thoughts.

I am an NHS employee with 34 years service.I am 57 years of age, my plan moving forward is partial retirement at 60. Taking my 1995 pension benefits, whilst continuing with vastly reduced hours and still contributing to my 2015 pension.

I also have an old DC policy (with GAR) This is made up from contracting out of serps and a small amount that I contributed pre 1992. The current transfer value is approx £27,500. My thoughts were to take this as a lump sum. Feeling that the Annuity I could purchase would be small.

I am an NHS employee with 34 years service.I am 57 years of age, my plan moving forward is partial retirement at 60. Taking my 1995 pension benefits, whilst continuing with vastly reduced hours and still contributing to my 2015 pension.

I also have an old DC policy (with GAR) This is made up from contracting out of serps and a small amount that I contributed pre 1992. The current transfer value is approx £27,500. My thoughts were to take this as a lump sum. Feeling that the Annuity I could purchase would be small.

I have been procrastinating a little, due to the amount of tax I would pay. However I now understand that if the pot amounts to £30K. I would need opinion from IFA, before moving forward. Which could amount to £0000’s.

Am I looking at matters correctly ? Anything else I should be considering with this DC policy ?

Am I looking at matters correctly ? Anything else I should be considering with this DC policy ?

Many thanks and warmest regards.

0

Comments

-

Regarding the DC pot, I think you are confused between the rules for DB and DC. It doesn't matter how big the DC pot is, you don't need to take advice on withdrawing it. Even if the pot is a lot bigger than £30k you can take an annuity or not, it's up to you.

Taking the whole lot in one go may not be the best idea. If you can avoid paying too much tax on the withdrawal, even if that means staggering the withdrawal over a few years, this may be the better option.0 -

What you need to ask your DC admins about is whether they do "drawdown". Basically it's taking lumpsums but in small chunks. This was you can access the money over a number of years to avoid losing a lot to income tax. Check also what the tax free percentage is. Normally it's 25% but some schemes may differ so best to check.

I had 2 DC schemes - one did not allow drawdown but it could be transferred out to a private pension and then accessed from there OR transferred to an annuity. The other allowed drawdown but only over 2 consecutive years. It was a bit less than what you have and there was 25% tax free so I got it in 2 payments either side of the new tax year so half in March and the other half in April. I was taxed at source (by the admins) as if I would be receiving a similar payment every month but because my annual income is relatively low I'll get the excess tax back.

Check also to see if this DC scheme or the NHS ones offer any pension guidance. Not advice per se but just have a person telling you a bit more about what you are entitled to and answering general questions. Take advantage of that if it's available. And talk to "pension wise" - again it's a good way to better understand pensions in general.

more info here - Pensions and retirement | Help with pensions and retirement | MoneyHelper

AND very importantly - check out your state pension forecast to ensure you're going to get the maximum or whether you're going to need to buy more years. Link in my signature below.I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅0 -

The GAR is a safeguarded benefit so you may well be right about the £30k cut off. Best to ask the pension provider. Maybe transfer to a more modern scheme while you can?

If the current scheme has a GAR then it is probably in a with profits policy which won't be generating a massive return. Then again it is probably a bit late to go getting too adventurous with the investments.

Does the GAR fall away at any point? eg when you reach 60? If so you could just leave it till then - perhaps see how much annuity it will buy at that time and if you don't like it wait for the GAR to expire and transfer to another scheme to put it into drawdown then. Of course not all GARs expire on your selected retirement date.0 -

El_Torro said:Regarding the DC pot, I think you are confused between the rules for DB and DC. It doesn't matter how big the DC pot is, you don't need to take advice on withdrawing it. Even if the pot is a lot bigger than £30k you can take an annuity or not, it's up to you.

Taking the whole lot in one go may not be the best idea. If you can avoid paying too much tax on the withdrawal, even if that means staggering the withdrawal over a few years, this may be the better option.

Regarding not needing advice on a DC pot - I believe there may be a need for advice if there is a GAR, and the pot is bigger than £30k (not the case here at the moment I know, but....)

0 -

I also have an old DC policy (with GAR) This is made up from contracting out of serps and a small amount that I contributed pre 1992. The current transfer value is approx £27,500. My thoughts were to take this as a lump sum. Feeling that the Annuity I could purchase would be small.Rather than relying on feelings, focus on the facts. What is the GAR? A very good GAR is typically double digits. Whereas at the other end you have ex Co-op plans (now royal london) with awful GARs.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Hi There.dunstonh said:I also have an old DC policy (with GAR) This is made up from contracting out of serps and a small amount that I contributed pre 1992. The current transfer value is approx £27,500. My thoughts were to take this as a lump sum. Feeling that the Annuity I could purchase would be small.Rather than relying on feelings, focus on the facts. What is the GAR? A very good GAR is typically double digits. Whereas at the other end you have ex Co-op plans (now royal london) with awful GARs.

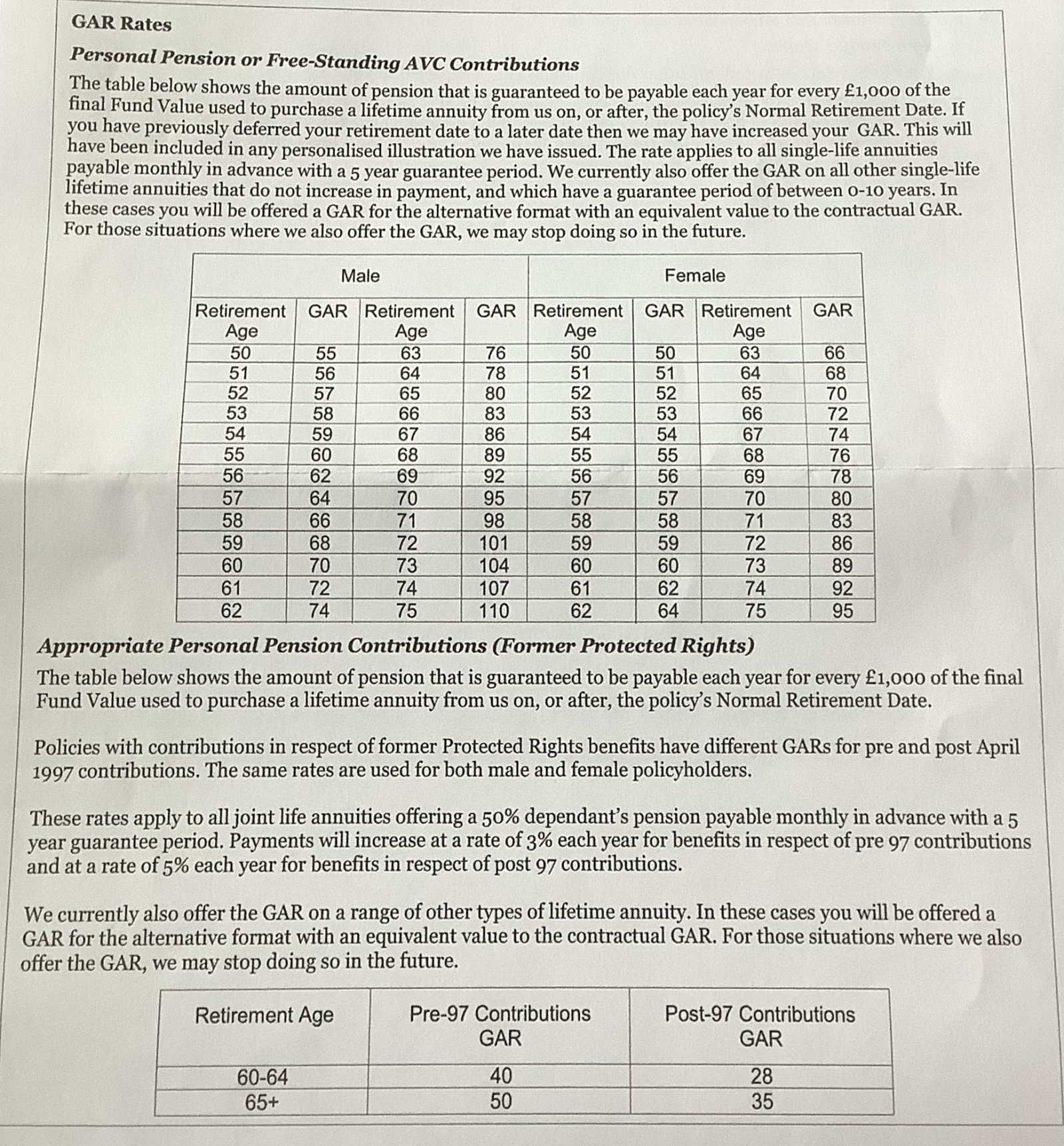

The policy is an old legacy Co-Op product, that has moved across to royal London. So presumably subject to the awful GARs. I found the following in this years paper work. Must confess, I wouldn’t know if this is good or bad ?

thank you

0 -

Hi There.El_Torro said:Regarding the DC pot, I think you are confused between the rules for DB and DC. It doesn't matter how big the DC pot is, you don't need to take advice on withdrawing it. Even if the pot is a lot bigger than £30k you can take an annuity or not, it's up to you.

Taking the whole lot in one go may not be the best idea. If you can avoid paying too much tax on the withdrawal, even if that means staggering the withdrawal over a few years, this may be the better option.

i have checked, if the policy reaches £30 K. I will need IFA before claiming. I understand this advice to be expensive ?Thank you0 -

Generally you need advice if it is >£30k and has safeguarded benefits (such as a GAR) only if you want to transfer it to another provider, not if you just want to claim it. Transfer advice can be £5k and chances are that the advice will be to not transfer.Fitzy712 said:

Hi There.El_Torro said:Regarding the DC pot, I think you are confused between the rules for DB and DC. It doesn't matter how big the DC pot is, you don't need to take advice on withdrawing it. Even if the pot is a lot bigger than £30k you can take an annuity or not, it's up to you.

Taking the whole lot in one go may not be the best idea. If you can avoid paying too much tax on the withdrawal, even if that means staggering the withdrawal over a few years, this may be the better option.

i have checked, if the policy reaches £30 K. I will need IFA before claiming. I understand this advice to be expensive ?Thank youI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

The policy is an old legacy Co-Op product, that has moved across to royal London. So presumably subject to the awful GARs. I found the following in this years paper work. Must confess, I wouldn’t know if this is good or bad ?I had a gut feeling it was, which is why I mentioned them by name.

The contracted out of SERPs part get the lower figures on that page. Any personal contributions get the upper part.

Current annuity rates on the open market pretty much match those GARs. So, they are not particularly of value.i have checked, if the policy reaches £30 K. I will need IFA before claiming. I understand this advice to be expensive ?It's not a transaction that most IFAs will like to do. Especially on relatively low fund values. So, often it is priced to put you off.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Had you considered a transfer of the pension to a modern plan?

Example

https://www.hl.co.uk/pensions/sipp

You could then just draw down when it suits you.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards