We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Newbie Pension Help.

Comments

-

GAR rates not gender neutral - can they insist on the lower rates for female policyholders as annuity rates are gender neutral since about December 2012.dunstonh said:The policy is an old legacy Co-Op product, that has moved across to royal London. So presumably subject to the awful GARs. I found the following in this years paper work. Must confess, I wouldn’t know if this is good or bad ?I had a gut feeling it was, which is why I mentioned them by name.

The contracted out of SERPs part get the lower figures on that page. Any personal contributions get the upper part.

Current annuity rates on the open market pretty much match those GARs. So, they are not particularly of value.i have checked, if the policy reaches £30 K. I will need IFA before claiming. I understand this advice to be expensive ?It's not a transaction that most IFAs will like to do. Especially on relatively low fund values. So, often it is priced to put you off.0 -

Hi there, sorry to jump on the OPs post but I thought my question might be useful to them too. I have a pension with cis in two parts personal and serps and I was wondering if you were trying to get a better annuity than what cis are offering , would that make a difference when approaching an IFA to try and transfer when you reach retirement and looking to take your pension ? I realise that it is a high risk to the IFA but I am not trying to get out of the annuity just trying to procure a better one. Many thanks0

-

If an IFA was to arrange a lifetime annuity that was better than the GAR (which is possible as I did one a few months back), then its not high risk for the IFA. It is only when the transfer is for flexible benefits that the risk exists.Macncheese said:Hi there, sorry to jump on the OPs post but I thought my question might be useful to them too. I have a pension with cis in two parts personal and serps and I was wondering if you were trying to get a better annuity than what cis are offering , would that make a difference when approaching an IFA to try and transfer when you reach retirement and looking to take your pension ? I realise that it is a high risk to the IFA but I am not trying to get out of the annuity just trying to procure a better one. Many thanksI am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Thank you for the quick reply , that is good to know that it is possible. What would the ballpark figure be for such a transaction ? I know there is a lot of work involved ?0

-

Sorry should have said the pension would be around £160000 thank you0

-

Thank you for all the reply’s.

I think the best option for my circumstances is to take my pot as a lump sum. Or more specifically, series of lump sums in order to minimise the tax burden.

warmest regards.0 -

Have you had an interview with Pension Wise?

https://www.moneyhelper.org.uk/en/pensions-and-retirement/pension-wise

0 -

Yes, if the GAR rates were set before the requirement to price on a gender equal basis.FIREDreamer said:

GAR rates not gender neutral - can they insist on the lower rates for female policyholders as annuity rates are gender neutral since about December 2012.dunstonh said:The policy is an old legacy Co-Op product, that has moved across to royal London. So presumably subject to the awful GARs. I found the following in this years paper work. Must confess, I wouldn’t know if this is good or bad ?I had a gut feeling it was, which is why I mentioned them by name.

The contracted out of SERPs part get the lower figures on that page. Any personal contributions get the upper part.

Current annuity rates on the open market pretty much match those GARs. So, they are not particularly of value.i have checked, if the policy reaches £30 K. I will need IFA before claiming. I understand this advice to be expensive ?It's not a transaction that most IFAs will like to do. Especially on relatively low fund values. So, often it is priced to put you off.1 -

Morning All.

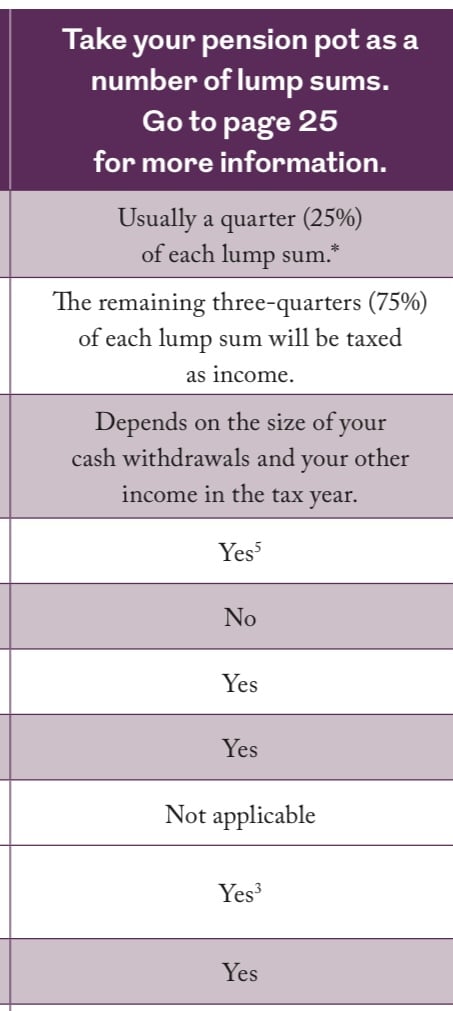

could I quickly resurrect my post for a moment. I decided that my best option, was to take my £27K pot in two lump sums. Over two tax years in order to minimise the tax burden.

I studied the options information from Royal London, and to me it seemed clear that each lump sum would be 25% Tax free. Following initial consultation today. I have been informed that only the first drawdown would be 25% tax free ? I have included a snap shot of the paperwork, to me it states each lump sum would be 25% tax free. Have i read this wrong ?Many thanks , appreciate your thoughts… 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards