We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

So....April 6th

Comments

-

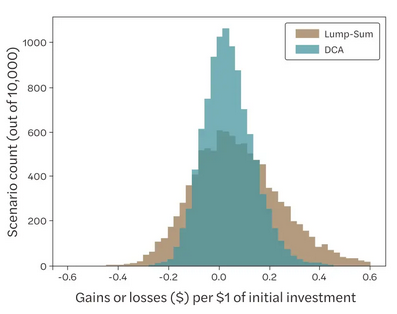

This thread seems to be a journey into how to discredit the correct answer using specious data and questionable authorities.Vanguard regularly publishes informative and data-driven articles on this subject, for example: https://corporate.vanguard.com/content/dam/corp/research/pdf/cost_averaging_invest_now_or_temporarily_hold_your_cash.pdfThere are also others who have done similarly, e.g. https://ndvr.com/pdf/documents/journal/NDVR-TimeInVsTimingTheMarket-October2023.pdfI don't think there is really any disagreement that in most scenarios lump sum outcome is better than cost averaging, but that isn't really the point. The argument is that cost averaging narrows the range of outcomes to avoid the very worst (and as a consequence the very best). Here's a plot of the distribution of outcomes over a year for investing a lump sum at the start vs daily cost averaging over the year:

You can see that the lump-sum approach gives a broader range of outcomes, while the DCA approach has a much tighter distribution around its median, reflecting its lesser exposure to the riskier asset due to it being held for a shorter duration.Advocates of DCA are looking to avoid the left tail of the distribution, but in doing so, they need to give up the right-tail of distributions, which is wider and has a greater area. They are more likely to get an outcome close to the average outcome, but this average is slightly lower than the average outcome from investing a lump sum. They have a relatively low chance of getting one of those >20% return outcomes on the right tail of the distribution. That is the price for the reduced risk. A similar effect is seen when someone decides to reduce risk in a constant manner by holding a lower percentage in equities.Most of the available data into DCA vs lump sum is based on simulations of historic market data without consideration for the start point. Markets are often at all time highs, so these averages will reflect that. If markets have already fallen, then the case for DCA will be weaker. For example, when a market has already fallen 15% from its previous high, the chances of it falling significantly further are much diminished compared with a market at an all time high, and the chance of significant positive returns over the following few months is greater.6

You can see that the lump-sum approach gives a broader range of outcomes, while the DCA approach has a much tighter distribution around its median, reflecting its lesser exposure to the riskier asset due to it being held for a shorter duration.Advocates of DCA are looking to avoid the left tail of the distribution, but in doing so, they need to give up the right-tail of distributions, which is wider and has a greater area. They are more likely to get an outcome close to the average outcome, but this average is slightly lower than the average outcome from investing a lump sum. They have a relatively low chance of getting one of those >20% return outcomes on the right tail of the distribution. That is the price for the reduced risk. A similar effect is seen when someone decides to reduce risk in a constant manner by holding a lower percentage in equities.Most of the available data into DCA vs lump sum is based on simulations of historic market data without consideration for the start point. Markets are often at all time highs, so these averages will reflect that. If markets have already fallen, then the case for DCA will be weaker. For example, when a market has already fallen 15% from its previous high, the chances of it falling significantly further are much diminished compared with a market at an all time high, and the chance of significant positive returns over the following few months is greater.6

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards