We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

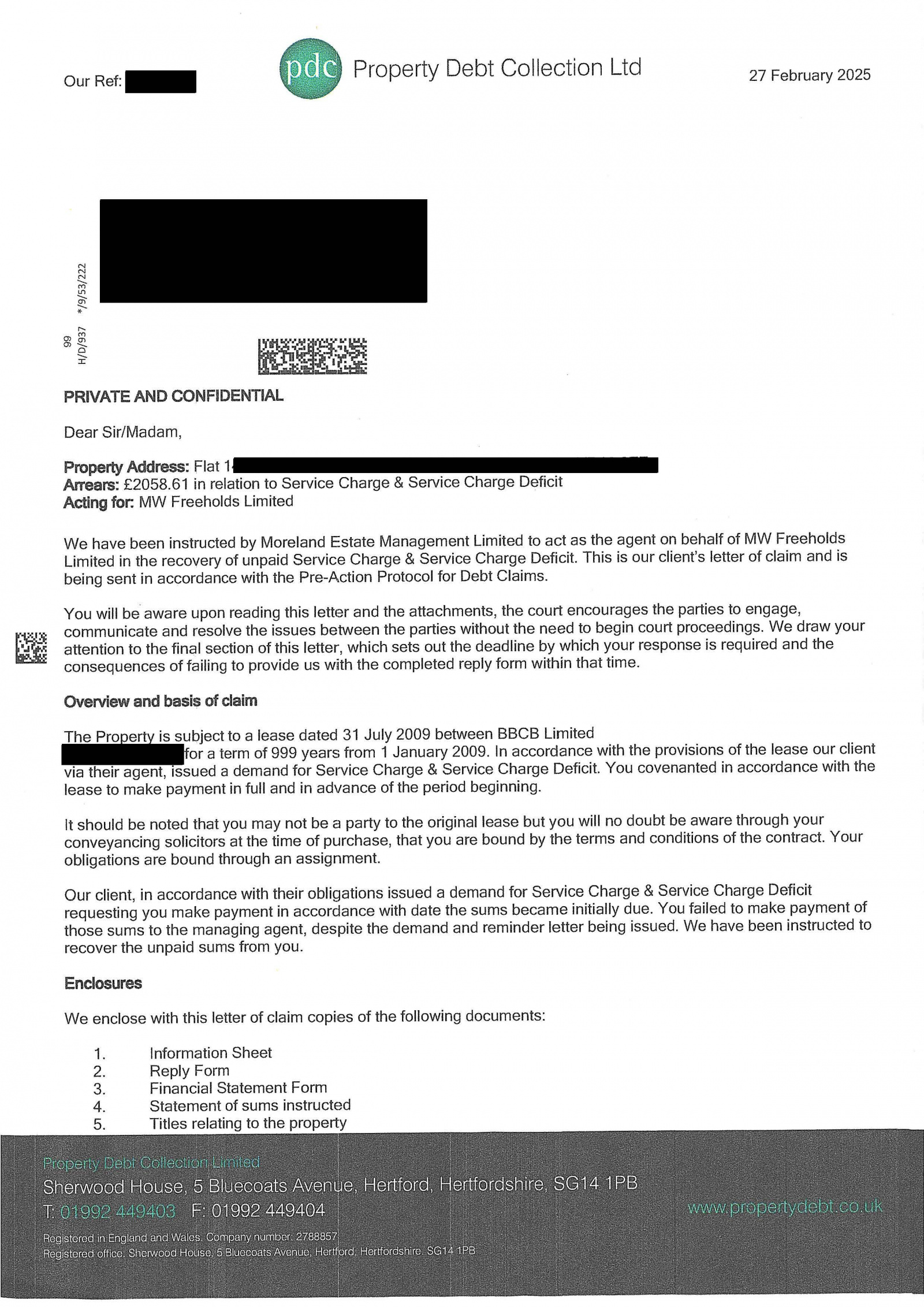

Being chased for a statute-barred debt by Property Debt Collection Ltd for Moreland / MW Freeholds

Hi all

Hope this is in the right part of the forum.

I bought a BTL flat in Cornwall in 2009 and, along with the

other leaseholders, exercised our Right To Manage (RTM) in 2014. I have

duly continued paying the ground rent yearly to the freeholders MW

Freeholds, however their in-house management co Moreland Estate

Management, who we got rid of in 2014, have continued sending us monthly

'Applications For Payment' relating to demands for service charge that they

continued to make after the RTM took effect but have never answered any

requests for clarification of how these service charges were calculated (which

is why we haven't paid them).

I have written about this previously - Statute-barred

debts — MoneySavingExpert Forum - and one way or another it appeared that the

situation was effectively a stable 'frozen conflict' inasmuch as Moreland

Estate Management can’t sue a leaseholder but CAN get them to pay up by MW Freeholds refusing to give freeholder's consent if they want to sell

a flat.

That was until Tuesday this week when I arrived back in London

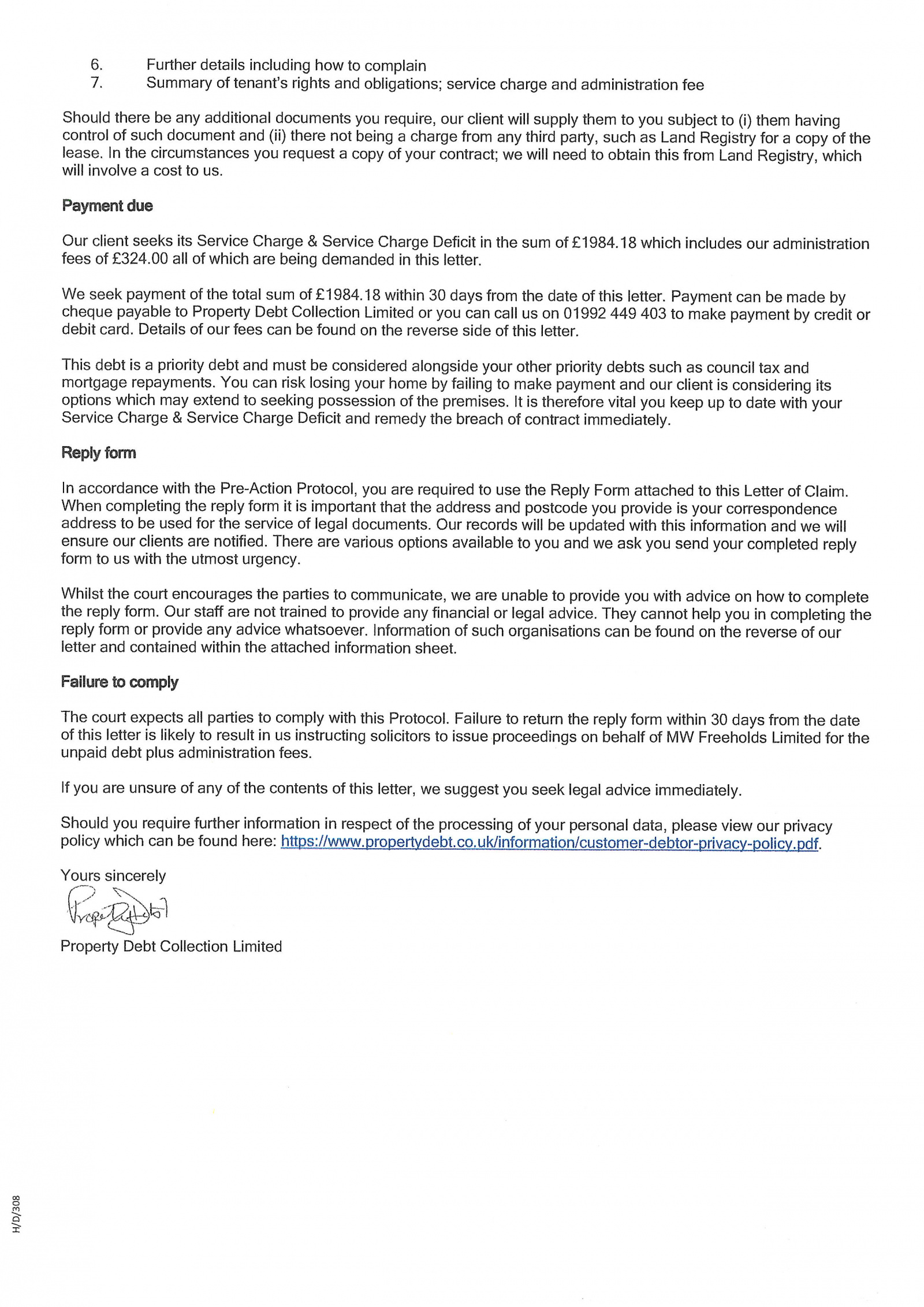

after 2 ½ weeks away and found these 2 letters waiting for me. And

see how they’re a week apart with different amounts (and when the latest

‘Application for Payment’ dated 23 Feb had said £1084.18)

Has anyone else had this situation or similar and, if so, how have you dealt

with it?

Any advice / suggestions gratefully received.

Thanks

R

Comments

-

Hi all

My first post in MSE for some time. I hope this is in the right part of the forum - if anyone thinks it is not then pls feel free to advise where it SHOULD go.

My question: is time barred debt legally enforceable if the creditor has been requesting payment from before the 6 years expired? What happened is that in 2009 I bought a buy-to-let flat in a block in Cornwall and in 2010 the original owners sold the freehold to a faceless bunch of money-grubbing sharks (Moreland Estates in case anyone's heard of them). Moreland supposedly have an in-house property management division and, as freeholders, they replaced the original Cornish property managers in favour of their own in-house team (Moreland Estate Management).

As you can probably guess, the service charge promptly ballooned and the quality of service did the opposite. London-based Moreland had no Cornish connections whatsoever and repeatedly we the leaseholders asked Moreland to show how these service charges were calculated and why they had suddenly shot up, when conversely the cleaning of the common areas and any other services that a management co would normally do had stopped the moment Moreland took over, to be met only with a deafening silence from Moreland (accompanied by regular demands for ££)

So, in 2014 the leaseholders clubbed together and exercised their Right To Manage. This involved getting rid of Moreland in favour of a management co of our choosing and everything has been good since.

Good, that is, except for the fact that Moreland Estate Management has continually, between 2014 and now, been chasing the leaseholders for management fees supposedly owed for the period between when we gave notice to Moreland Estate Management that we were changing to another management co, and the date this took effect a few months later. Every month, they send each of us an 'Application For Payment' with these management fees PLUS various 'late fees' / 'admin charges' and so on. Once they tried suing one of us for unpaid management fees and, tellingly, the action got struck out when the County Court asked Moreland to show how these supposedly unpaid management fees were calculated and Moreland did not do so.

Irritatingly some of the leaseholders have tried selling their flats over the years and, when the conveyancers acting for the incoming buyers have discovered these supposedly outstanding management fees, they have insisted that these fees be settled before the sale could proceed. Result? The outgoing leaseholders have had no choice but to pay Moreland what Moreland say they are owed.

On the face of it this should not be happening because these supposedly outstanding management fees date from 2014 ie a period well over 6 years. However it has been suggested that, because Moreland has been chasing the fees since before the 6 years expired, the 6 years limit does not apply and the alleged debt remains legally enforceable.

Hence my question: is time barred debt legally enforceable if the creditor has been requesting payment from before the 6 years expired?

Looking forward to hearing any thoughts anyone may have on this.

Cheers0 -

Best to read through this on Debt Camel

Statute barred debt - common questions · Debt Camel

But these seem to be the crucial bits...Think of a timer that runs for 6 years – which can be reset

A good way to think of statute barring is that there is a 6 year timer. This is set running when the creditor has a cause of action. The sand takes 6 years to drain slowly through… at the end, your debt is statute barred.

But if you make a payment to the debt or acknowledge it in writing during the six years, the clock is reset back to start at 6 years again.

--

How can I tell if my debt is statute-barred?

Unsecured debts, including most loans, credit cards, catalogues and overdrafts will normally be statute-barred in England and Wales if you can say YES to all the following four points:

- it had been more than six years since you last made a payment; and

- the creditor has a cause of action more than six years ago; and

- you haven’t acknowledged the debt in writing during this time; and

- the creditor hasn’t already gone to court for a CCJ.

--

Acknowledging the debt has to be in writing. If you haven’t done this, it doesn’t matter if the creditor has written to you, or you have discussed the debt on the phone – this won’t stop the debt being statute barred.

I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅🏅0 -

Assuming you are in England or Wales, a "service charge" is nothing more than a simple contract debt, and will fall under section 5, limitation act, 1980.

In this case, the "cause of action" date would have been when these charges became due, they then had 6 years in which to chase these debts, after which time, if no payment or written acknowledgement has been made by the debtors, the debt becomes what is termed "statute barred".

However, in a quirk of fate permissible only in English law, the debt still exists, its just that time has run out for the creditor to use legal action to collect it.

So they can still ask for payment, they just can`t force you to pay.

That is unless you live in Scotland, or are governed by Scottish law, the law is more debtor friendly, and the same debt there would become "prescribed" after 5 years, and is then extinguished, and cannot ever be chased under threat of prosecution.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

All

Many thanks for this - V helpful.Brie said:But if you make a payment to the debt or acknowledge it in writing during the six years, the clock is reset back to start at 6 years again.

This comment by Brie has now prompted another thought in my mind: although I haven't ever said to Moreland 'i accept I owe you this money' , i HAVE OTOH acknowledged it implicitly in that I asked them to show how it was calculated (and did not say 'I don't owe you this money'). That said, I need to look up when I asked for this information as I believe I asked for it well over 6 years ago.

Based on what you have said, Brie, that suggests to me that if a debt is (let's say) 8 years old but the debtor acknowledged it 5 years and 9 months ago (and hasn't said anything to the creditor, nor had any response from them, since), the creditor has another 3 months to pursue it. Is that correct?

Mark

0 -

If the debt was last acknowledged 5years and 9 months ago, the creditor has another 3 months to take enforcement action (England and Wales).ripofflondon said:All

Many thanks for this - V helpful.Brie said:But if you make a payment to the debt or acknowledge it in writing during the six years, the clock is reset back to start at 6 years again.

This comment by Brie has now prompted another thought in my mind: although I haven't ever said to Moreland 'i accept I owe you this money' , i HAVE OTOH acknowledged it implicitly in that I asked them to show how it was calculated (and did not say 'I don't owe you this money'). That said, I need to look up when I asked for this information as I believe I asked for it well over 6 years ago.

Based on what you have said, Brie, that suggests to me that if a debt is (let's say) 8 years old but the debtor acknowledged it 5 years and 9 months ago (and hasn't said anything to the creditor, nor had any response from them, since), the creditor has another 3 months to pursue it. Is that correct?

Mark

A lot depends exactly how you made the request for calculation? A Letter might be a problem, on the phone wouldn't be. And exactly how the request was worded. The Prove it letter here is worded so it avoids any acknowledgement of liability, for example.If you've have not made a mistake, you've made nothing0 -

They would have another three months to start a court claimripofflondon said:All

Many thanks for this - V helpful.Brie said:But if you make a payment to the debt or acknowledge it in writing during the six years, the clock is reset back to start at 6 years again.

This comment by Brie has now prompted another thought in my mind: although I haven't ever said to Moreland 'i accept I owe you this money' , i HAVE OTOH acknowledged it implicitly in that I asked them to show how it was calculated (and did not say 'I don't owe you this money'). That said, I need to look up when I asked for this information as I believe I asked for it well over 6 years ago.

Based on what you have said, Brie, that suggests to me that if a debt is (let's say) 8 years old but the debtor acknowledged it 5 years and 9 months ago (and hasn't said anything to the creditor, nor had any response from them, since), the creditor has another 3 months to pursue it. Is that correct?

Mark

0 -

All - many thanks for this - been a few days since I last logged in. Take care!

KR, Mark0 -

Unfortunately, I think this advice that you were given in your previous thread in Jan 2024 is incorrect...sourcrates said:Assuming you are in England or Wales, a "service charge" is nothing more than a simple contract debt, and will fall under section 5, limitation act, 1980.

In this case, the "cause of action" date would have been when these charges became due, they then had 6 years in which to chase these debts, after which time, if no payment or written acknowledgement has been made by the debtors, the debt becomes what is termed "statute barred".

Leases are generally executed as deed, not as a simple contract. So it's section 8 of the Limitation act that applies, not section 5.

So the time limit is 12 years for taking action for service charge arrears (not 6 years).

Generally, the standard advice with Service Charge bills is...- Pay the full amount of the bill - saying that you are paying under protest

- Challenge the bill at a tribunal

Here's the Leasehold Advisory Service's flowchart for dealing with Service Charge disputes: https://www.lease-advice.org/files/2021/12/Service-Charges-Dispute-Resolution-Flowchart.pdf

Here's a template letter of protest: https://www.lease-advice.org/template-document/15-leaseholders-letter-objecting-to-demand-for-service-charges-payment-under-protest/

FWIW, it looks like...- The Admin fees in the letter dated 19 Feb were £324

- The Admin fees in the letter dated 27 Feb were £396 (i.e. £72 more)

It's very possible that the extra £72 is the fee for sending a second letter. The law specifically allows the management co to charge fees for sending letters like this.

(There's seems to be an additional increase of £2.43 - maybe that's interest)

If you don't pay the full amount, the management co can continue to charge you £72 for further letters, plus solicitors fees etc (which might amount to hundreds or even thousands of pounds).

That's why it's best to pay (under protest) - to stop further charges being added, and to stop other legal action.

0 -

Just an update on this thread...

The advice in this thread doesn't seem to be generally correct.

The OP has posted a follow up on this in the Housing, Renting and Selling board...

https://forums.moneysavingexpert.com/discussion/6594533/being-chased-for-a-statute-barred-debt-by-property-debt-collection-ltd-for-moreland-mw-freeholds#latest

Leases are generally executed as a deed, in which case section 8 of the Limitation Act applies to service charge debts (not section 5).

So the creditor generally has 12 years (not 6) to take action for unpaid service charges (in England and Wales)

For more background info, here's what a few solicitors' websites say:The 12 year limitation period

Charges that are not rent or reserved as rent (or an estate rent charge) and which are payable under a deed/lease, are in most cases (but not all) subject to a 12 year limitation period by s.8 Limitation Act 1980.

Link https://www.kdllaw.com/legal-updates/how-far-back-can-service-charges-and-rent-be-recoveredService Charge Arrears RecoverySo, providing that these four conditions below are met, you will be able to recover service charge arrears accrued up to 12 years ago:

- The long residential lease was executed as a deed, not a contract

- The service charge is not recoverable as rent

- The original service charge demands were issued correctly and in accordance with the lease, and

- The demands were made within 18 months of the costs being incurred

However, the lease will have been executed as a deed. This means that it will be sealed and witnessed when completed. As a consequence of that, the timeframe the Limitation Act 1980 provides for the limitation period is 12 years. This is because a deed is a “specialty” for the purpose of the Limitation Act 1980 and a specialty has a limitation period of 12 years rather than 6 years. Therefore, so long as the arrears accrued within the last 12 years the landlord will be able to pursue legal action against the leaseholder.

Link: https://www.devonshires.com/ask-the-expert-recovery-of-historic-service-charge-arrears/

1 -

Thanks for responses.

Oh dear. I may be clutching at straws here, but does it make any difference that the charges we are talking about are NOT ground rent to the freeholders (which I have paid every year without fail) but monthly ones to the management company for things like cleaning of the common areas etc?

And doesn't sending 2 letters a week apart like that look something like an abuse of process?

It's not like they sent the first letter then waited two months before sending the second one.

While on the abuse of process theme (and I wish I'd spotted this before) each letter has in fact added TWO admin charges each in the '£00s - the detail of this is in the Statement Of Sums Instructed which I apologise for overlooking but will scan and upload to this thread as soon as I get access to the physical papers on Monday.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards