We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Maximising Isa income

Comments

-

It's the same as with company shares and ETFs, you just need to hold it on the ex-dividend date so you could buy it the day before and you'll receive the distribution. Technically it'll be split, paid as part capital and part dividend or interest but you'll receive the distribution. You can then sell it and move on to the next fund. I don't understand the magic money tree aspect but from a mechanical POV I can understand what the OP's doing.Linton said:

I have a significant income fund ISA portfolio....Luvcricket said:Well all I know is that from £215,000 invested, I am due over £7,200 tax free this month.

Therefore I am expecting a possible £85,000 tax free, over the year 2025.

I think that is pretty good income, to add to our pensions!!

Switching between funds wont help because to be paid a dividend you must be holding the fund a significant time (eg 2 moinths) before the payment date. ISTM that by the time you get a payout from your switched-to fund you will have missed the chance to switch back again to get the dividend from your original fund.

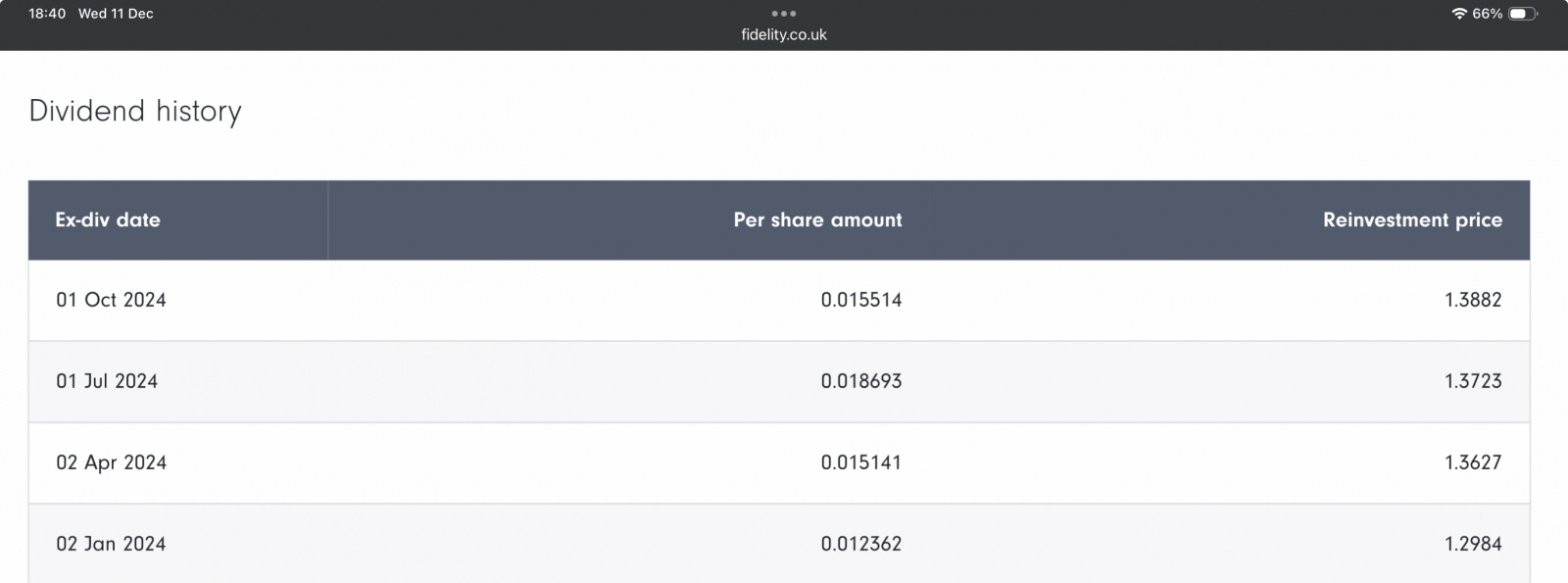

E.g., Liontrust Income C Inc OEIC:

https://www.fidelity.co.uk/factsheet-data/factsheet/GB00B8L7B355-liontrust-income-c-inc/dividends

0 -

Yes you are right that income funds can yield 7% or more.

If you take the 4 quarterly funds alone and research the past dividends (not guaranteed for the future I know)

All 4 funds can each make over £12,000 p.a., based on my amount invested.

Using all 4 quarterly funds could therefore, make approximately £50,000 p.a.

I know the income is not guaranteed, but we'll see how it goes!

As far as my claimed 30% income p.a. is concerned, I don't think that is too far out.

I am also using monthly income funds, as well as the 4 quarterly funds.

Last year using just one quarterly fund (not one I'm using now) I received £9,500 in income.

I have since maxed my Isa allowance since April.

Now that my switching is fully up and running ( it takes around 2 months or so to get full income)

I will be getting over £13,000 just for November & December alone!

As I have already stated I know the risks, but the income is so good.

0 -

But that logic is flawed - if a given fund returns (not really 'makes') £12K pa from a certain balance, then it doesn't follow that rotating that capital around three other similar funds will net four times that amount! The fact that you'd regularly be selling funds immediately after the dividend payments means that each time you'd be failing to benefit from any meaningful capital appreciation, so you simply end up depleting the capital and paying yourself the income, except for those infrequent and unpredictable occasions where it's shooting up like hockey sticks, in which case you'd still be gaining heavily even without your switching wheeze....Luvcricket said:If you take the 4 quarterly funds alone and research the past dividends (not guaranteed for the future I know)

All 4 funds can each make over £12,000 p.a., based on my amount invested.

Using all 4 quarterly funds could therefore, make approximately £50,000 p.a.

I know the income is not guaranteed, but we'll see how it goes!

Edit: just to amplify this point with some rough numbers:

Let's say you're investing £200K into a hypothetical fund that generates a gross annual 10%, of which they distribute 6% (your £12K) as dividend income and the other 4% increases the unit price, so at the end of the year you have £12K income in your bank and £208K remaining invested.

If during the year you rotate that same £200K around a total of four funds, each with the same 10% annual growth profile, the total growth over the year would still be that same £20K, but four lots of 6% would be distributed as dividend income, so you would indeed now end up with £48K in your bank but you'd only be left with £172K invested.1 -

It's not the fact that they pay out interest and you're chopping and changing, it's just that you've invested in tons of low investment grade and junk bonds that have had a good run this year. If you'd followed the same strategy in 2021 you'd be crying right now, or at least less than you would have been in October 2022.Luvcricket said:So I am using 3 quarterly funds ( all with a dividend date of the 1st of relevant month)

Schroder Income Maximiser class L - income

Royal London Sterling Extra Yield Bond class Y - income. } These 3 funds cover the 12 months yearly.

Invesco High Yield class Z - income

PLUS a switch early Feb, May, Aug and Nov. to Artemis High Income class i - income ( divi dates : 8th)

Also Monthly income funds as follows:

Legal & General Active Global High Yield class i - income ( divi dates 8th each month) [to use on the 8 months when not using Artemis fund]

Schroder High Yield class Z - income ( divi dates 16th each month)

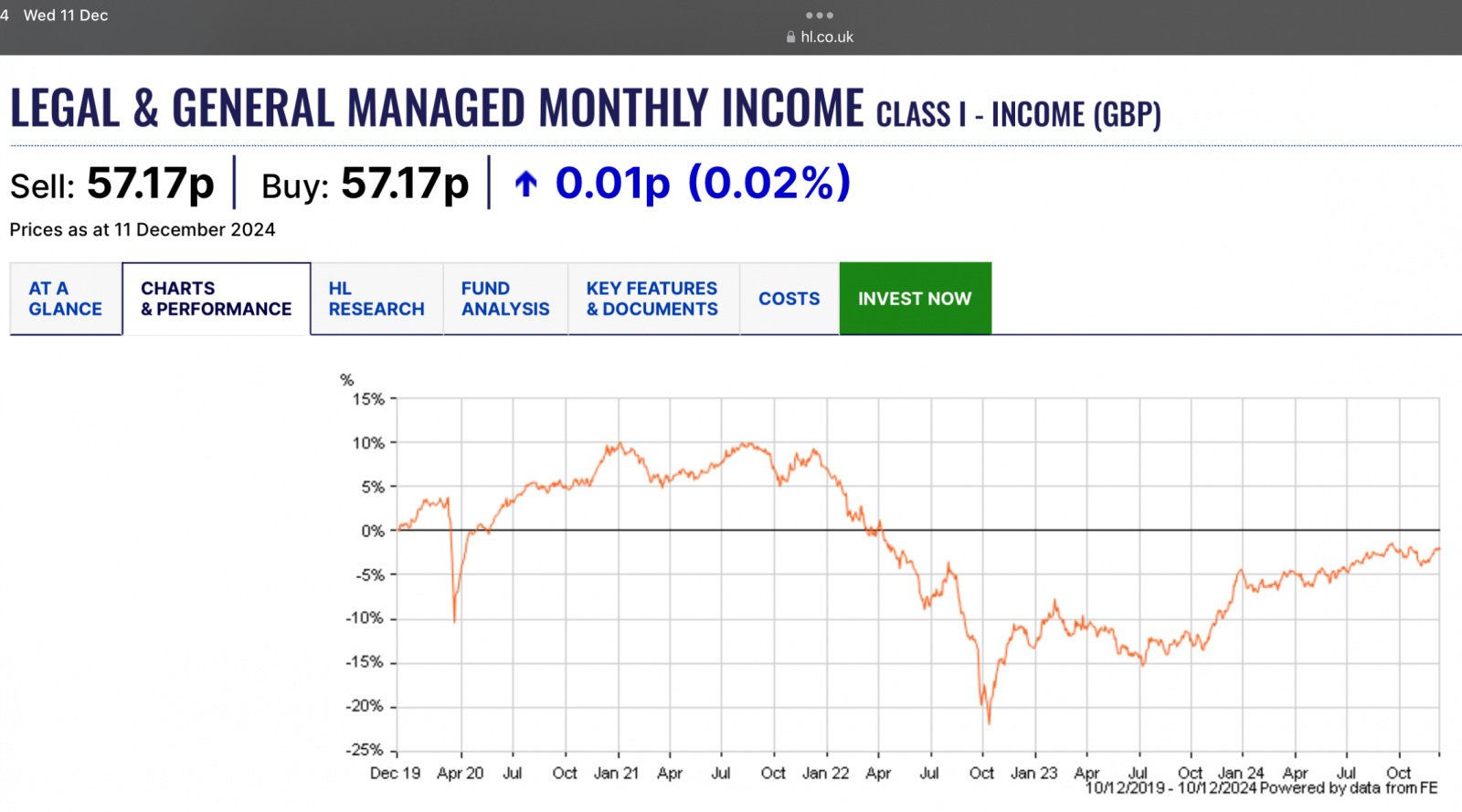

Legal & General Managed Monthly Income class i - income ( divi dates 22nd each month)

As switching between funds only takes 2 days, all 7 funds can be used.

0 -

If you genuinely think this tactic works you could move from share to share every trading day and get an annual yield in the hundreds of per cent, never mind a different quarterly fund a month.Sadly, what you're doing is just the equivalent of the farmer eating some of the corn as he plants, and thinking he's getting a free meal. The value drops when the dividend is declared. You buy £100 with a 5% dividend, the next day you have a £95 holding and a £5 dividend pending.Funds aren't stupid, none of them offer you both the dividend and the maintenance of the price you paid to acquire the right to the dividend - or, in the case of a 5% dividend paid once a year, an AER of 5,421,184,158%...

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards