We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Every month I buy into VWRP (accumulating) index fund at all time highs and I'm sick of it.

Comments

-

OP you need to stop being so emotional about your investing and look at the mathematics. You are doing very well right now. Pull backs will happen, I'm not sure why you want them given your lack of knowledge of the future. but if it makes you happy I'm sure there will be a time when your overall portfolio decreases in value and you'll be able to buy a few more shares with your monthly investment.And so we beat on, boats against the current, borne back ceaselessly into the past.1

-

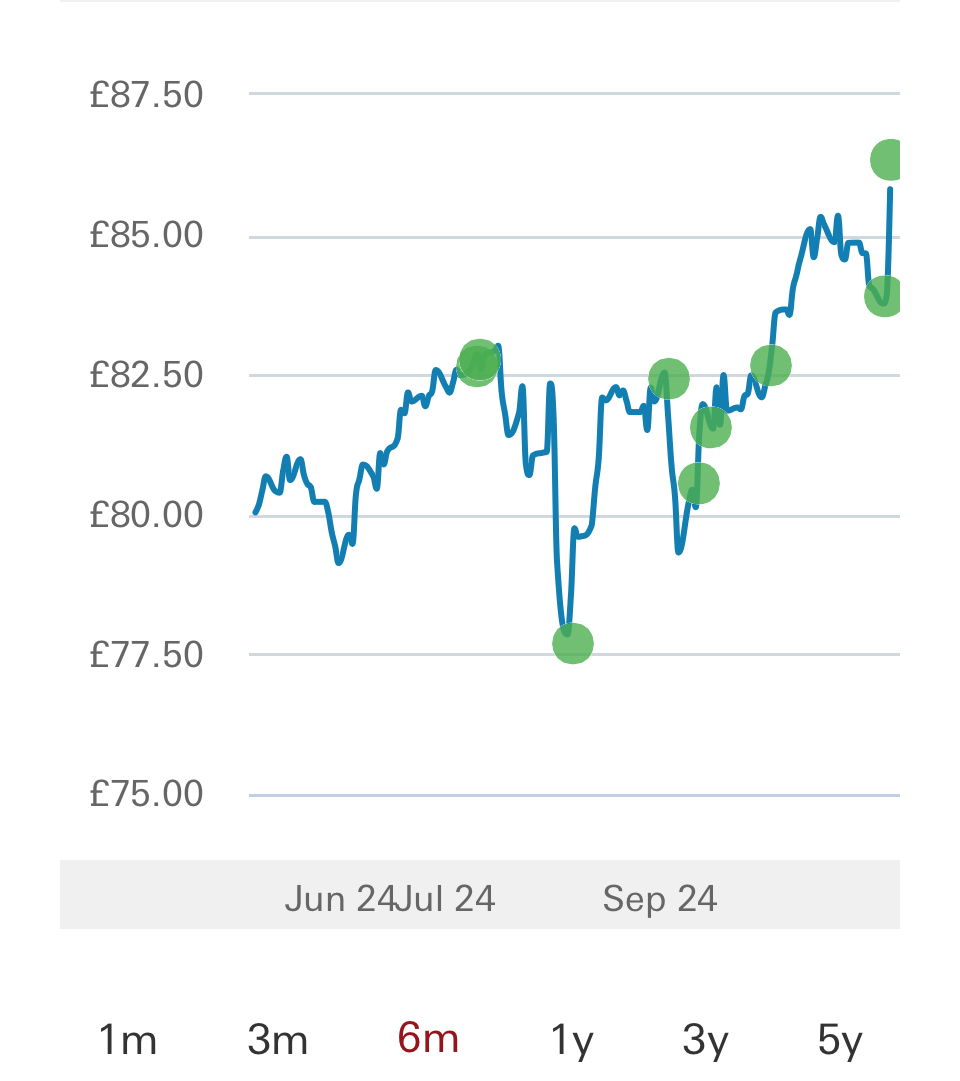

Have you been looking at your green dot graph on Vanguard?

0

0 -

Sounds like the OP missed out on 20220

-

Damn these cursed things that keep going up in value.

I am one of the Dogs of the Index.1 -

Swipe said:Sounds like the OP missed out on 2022Well he/she did say they had been investing for 2 years, so yes they would have missed out on most of 2022. But I also suspect they are being very selective in their recollection. If their next investment is tomorrow and they invest monthly then presumably all their purchases have been on or around the 8th of the month. In which case the idea that they have always purchased at temporary highs simply doesn't fit the facts.To the OP, I would say to ignore the details for at least the next 10 years given your investing timespan. Looking at the headline total value figure once a year for the next ten years is as much as you should do. There will inevitably be spells when it feels like you are always investing at the 'wrong' (*) time but there will also be spells when you seem to do pretty well at investing at the 'right' time. What matters is that you are making regular investments.* - the only 'wrong' time to invest is never and the only 'right' time is now.0

-

Your post is very good evidence (along with lots of others) that time in the market by investing as much as you can as soon (or simply a lump sum) beats drip feeding.

If you’re investing as much as you can afford to invest each month, then I don’t see why you’re complaining as there’s nothing you can do about it (assuming you’re investing as much as you can afford to do so)."If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” Warren Buffett

Save £12k in 2025 - #024 £1,450 / £15,000 (9%)1 -

[Deleted User] Is VWRP your only investment ?0

-

Drip feeding? You mean pound / dollar cost averaging? Isn't that the way you're meant to invest long term?george4064 said:Your post is very good evidence (along with lots of others) that time in the market by investing as much as you can as soon (or simply a lump sum) beats drip feeding.

If you’re investing as much as you can afford to invest each month, then I don’t see why you’re complaining as there’s nothing you can do about it (assuming you’re investing as much as you can afford to do so).

When I started this journey I set aside a portion of my money in a high interest cash ISA which is currently paying 5.1%, this is my emergency fund and doesn't get touched.

The remaining money I lump summed into VWRP and then with each proceeding pay check I took what I had left after rent, bills, food etc and bought as many shares as I could.

I have done this since exactly 14th June 2022. And since that time the market is up 39% but because I've been consistently buying at ever higher prices, my average return has been less, currently 22%.

This is the point I'm making... Because the market is constantly going up it drags my average UP, which I know is to be expected but I would like to at least have 6 months or 1 year where I'm buying low so my average feels more like the average.

It's like going shopping for food or clothing right? I think most people would like to walk into a store and see their food or clothes at a 20% discount rather than full price. That's all I'm saying...0 -

Yes, I'm not smart enough or comfortable enough to risk picking individual stocks. So I just buy a global index fund.Hoenir said:[Deleted User] Is VWRP your only investment ?0 -

[Deleted User] said:

Drip feeding? You mean pound / dollar cost averaging? Isn't that the way you're meant to invest long term?george4064 said:Your post is very good evidence (along with lots of others) that time in the market by investing as much as you can as soon (or simply a lump sum) beats drip feeding.

If you’re investing as much as you can afford to invest each month, then I don’t see why you’re complaining as there’s nothing you can do about it (assuming you’re investing as much as you can afford to do so).It is if the money you are investing is coming to you as a monthly income. That's the fastest way to get your money invested.It does seem odd, looking at the YTD price chart that you've missed all of the dips (August and September for example), but even if you did, in 20 years, the difference between £109 and £90 isn't going to seem significant. If you've been continuously buying at new all-time highs, then you'll have bought low in the first year. Your issue seems to be disbelieving your average price is your average price. 1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards