We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Fixed rate ISA - monthly or annual interest?

WindfallWendy

Posts: 254 Forumite

I have a lump sum of £15k I want to fix for 2 years. An account offers Annual interest at 4.4%, or monthly interest payments but at just 4.3%

Is this because of the cummulative effect, and the monthly payment will ultimately pay the equivalent of the annual rate? Or is it genuinely just a worse offer?

Since it's tax free, I don't really care when I get interest, so think annual will be fine. I guess if I choose/need to withdraw it, I would loose out with the annual interest.... 🤔 Would I?

Still quite new to this. Apologies for basic question.

Is this because of the cummulative effect, and the monthly payment will ultimately pay the equivalent of the annual rate? Or is it genuinely just a worse offer?

Since it's tax free, I don't really care when I get interest, so think annual will be fine. I guess if I choose/need to withdraw it, I would loose out with the annual interest.... 🤔 Would I?

Still quite new to this. Apologies for basic question.

0

Comments

-

If the AER is the same, then you'll get the same interest over each year if you don't add or withdraw from the ISA.If you close early, then you'll get a few pennies more out of the annual interest option, but may have to pay those pennies back in a penalty.0

-

@WindfallWendy No need to apologise at all! - we've all been new to this money saving thing at some point in the past and we would've then been asking very similar questions to the ones you've just asked now.WindfallWendy said:I have a lump sum of £15k I want to fix for 2 years. An account offers Annual interest at 4.4%, or monthly interest payments but at just 4.3%

Is this because of the cummulative effect, and the monthly payment will ultimately pay the equivalent of the annual rate? Or is it genuinely just a worse offer?

Since it's tax free, I don't really care when I get interest, so think annual will be fine. I guess if I choose/need to withdraw it, I would loose out with the annual interest.... 🤔 Would I?

Still quite new to this. Apologies for basic question.

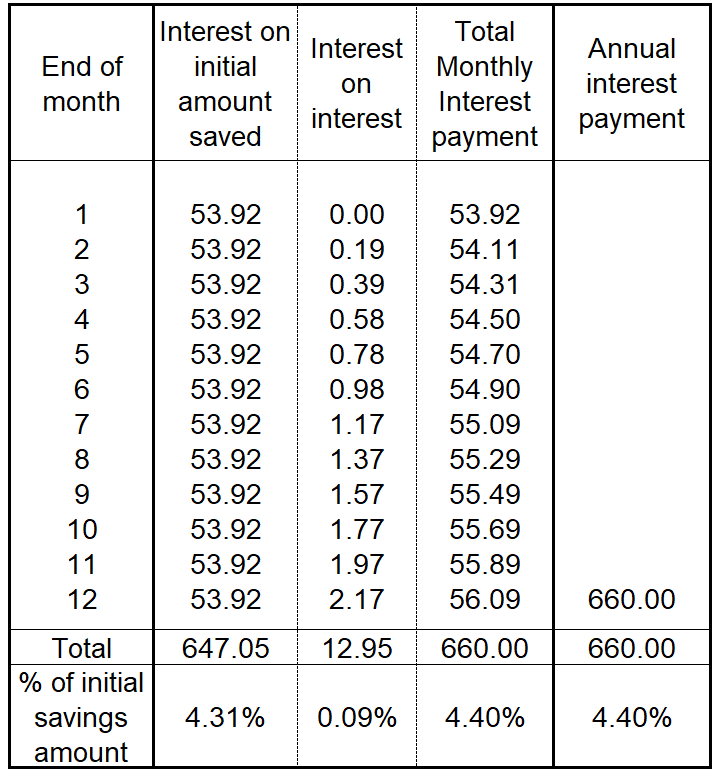

The reason monthly interest payments are only 4.3% whereas the annual interest payment is 4.4% is because the monthly interest compounds from month to month during each of the two 12 month periods that are included within the 2 year fix's lifespan. In other words, at the end of the very first month you receive a monthly interest amount of (£15k x 4.3%) / 12 = £53.75 which is added to the £15k to give you £15053.75. At the end of the 2nd month you receive a monthly interest amount of (£15053.75 x 4.3%) / 12 = £53.94 giving you now £15107.69. And so on. So each month you're getting interest on both the lump sum and the interest already received from previous months. After 12 months your new lump sum if you like will be very close to £15660 (it may be slightly more or less than this but only slightly) which is exactly the amount you would end up with if you opt for annual interest i.e. (£15k x 4.4%) + £15k.

After the 2nd year with annual interest at 4.4% your final total lump sum would be £16349.04 (= £15k + £1349.04 total interest) and, due to the compounding process explained above, monthly interest at 4.3% would give you a very similar final amount (again it may be slightly more or less that this but the difference will be very marginal). So yes the monthly payment does ultimately pay the equivalent of the annual rate (within a pound or two at the very most) as long as the monthly interest payments are left in the account to compound rather than being taken out of the account each month as a form of income. If the latter happens then there will be no compounding effect as you can't then earn new interest on the previous interest and so over two years you will have only earned a total of (£15k x 4.3%) x 2 = £1290 total interest i.e. exactly £59.04 less than the total amount of interest earned over 2 years with annual interest at 4.4%.

With the vast majority of fixed term, fixed interest rate accounts (annual or monthly interest) no withdrawals will be allowed during the lifespan of the fix other than monthly interest payments to an external account in the case of fixed term accounts that pay monthly interest (the majority of fixes currently available do not pay monthly interest btw). But as you mention it's tax free I assume you're considering a fixed rate ISA:- here the ISA regulations insist that withdrawals are permitted but, because of this, banks / building societies will charge a very substantial penalty for each withdrawal, which usually for a 2 year fix is the equivalent of 180 days interest on the amount being withdrawn. So I'm afraid you would unfortunately lose out significantly regardless of whether the interest was being paid to you monthly or annually. It is therefore usually not advisable to place a lump sum of money into any type of fixed term account (either a fixed rate cash ISA or a non ISA such as a fixed rate bond) unless you are pretty certain that you will not need to make a withdrawal from this lump sum during the lifetime of the fix!3 -

You just need to compare AER rather than the gross rate because AER takes into account the affect of compounding.Looking over the first year for example you can see in the table below that the interest on interest when interest is paid monthly accounts for the difference between 4.3%pa gross paid monthly and 4.4%pa gross paid annually. I've assumed annual interest is paid on the anniversary. Either route you end up with about £660 interest after the first year. And the same logic can be applied to the second year.Ignore the fact that to 2 decimal places 4.4% annual is equivalent to 4.31% paid monthly rather than 4.3%, it makes a trivial difference.

There are some nuances if you don't run the account the full term but with a fixed rate account you shouldn't be doing that because of the early exit penalties.I came, I saw, I melted1

There are some nuances if you don't run the account the full term but with a fixed rate account you shouldn't be doing that because of the early exit penalties.I came, I saw, I melted1 -

masonic said:If the AER is the same, then you'll get the same interest over each year if you don't add or withdraw from the ISA.If you close early, then you'll get a few pennies more out of the annual interest option, but may have to pay those pennies back in a penalty.It's a bit esoteric and the pragmatic approach would be to ignore it but you are right and I tend to usually opt for annual interest rather than monthly on any account (especially easy access accounts) where I don't want interest paid out because it just might on average give me a few £s of extra interest.If we imagine in my example above it was a single £15,000 payment into an easy access account paying 4.4% AER instead. And let's assume that the unrounded monthly AER is exactly equal to the unrounded annual AER, and that annual interest is calculated on the n/365 basis for an annual account closed at the end of different months of the year. Then there could be an up to about £3.50 difference (330 - 326.45) if annual interest was chosen and the £15,000 was withdrawn and the account closed after 6 months rather than if monthly interest was paid and the account closed after the month 6 interest payment. See the last 2 columns of the extended table below.

I don't know if savings institutions are still required to use the n/365 approach. It's an archaic approach from before modern computers came on the scene.There can be other considerations for taxed accounts in choosing before monthly and annual interest particularly in relation to which tax year the interest falls,I came, I saw, I melted3

I don't know if savings institutions are still required to use the n/365 approach. It's an archaic approach from before modern computers came on the scene.There can be other considerations for taxed accounts in choosing before monthly and annual interest particularly in relation to which tax year the interest falls,I came, I saw, I melted3 -

Most accounts calculate interest on the basis of n/365 x gross rate, whether paying monthly or annually, so I wouldn't describe as archaic. AER is computed using the equation at https://en.wikipedia.org/wiki/Effective_interest_rate and is an artificial figure that doesn't take into account the vagaries of different length months etc. YMMV depending on what date you open the account and whether it is a leap year.SnowMan said:masonic said:If the AER is the same, then you'll get the same interest over each year if you don't add or withdraw from the ISA.If you close early, then you'll get a few pennies more out of the annual interest option, but may have to pay those pennies back in a penalty.It's a bit esoteric and the pragmatic approach would be to ignore it but you are right and I tend to usually opt for annual interest rather than monthly on any account (especially easy access accounts) where I don't want interest paid out because it just might on average give me a few £s of extra interest.If we imagine in my example above it was a single £15,000 payment into an easy access account paying 4.4% AER instead. And let's assume that the unrounded monthly AER is exactly equal to the unrounded annual AER, and that annual interest is calculated on the n/365 basis for an annual account closed at the end of different months of the year. Then there could be an up to about £3.50 difference (330 - 326.45) if annual interest was chosen and the £15,000 was withdrawn and the account closed after 6 months rather than if monthly interest was paid and the account closed after the month 6 interest payment. See the last 2 columns of the extended table below.I don't know if savings institutions are still required to use the n/365 approach. It's an archaic approach from before modern computers came on the scene.There can be other considerations for taxed accounts in choosing before monthly and annual interest particularly in relation to which tax year the interest falls,

Interest is still fundamentally based on practices like inter-bank overnight lending (SONIA) and interest on retail mortgages and loans accruing daily, so I've not come across any accounts that use continuous compounding ( AER = e^i -1 ), although Trading212 does daily compounding ( AER = (1 + i/365)^365 -1 )

2 -

Blimey, you lot are awesome, thank you!! I did have in mind to do a spreadsheet and work through the compound interest etc. but hoped the answer might be at the tip of some fingertips on here. I wasn't wrong!!

So, the lock-in is fine. I'm not going to need the money, I just need it to be somewhere tax free. Given the AERs are the same, why WOULD anyone pick one version over the other? Kind of a rhetorical question, but curious if there are reasons.1 -

Monthly interest can often be paid away to a current account so you might choose it if you need the cashflow.WindfallWendy said:Blimey, you lot are awesome, thank you!! I did have in mind to do a spreadsheet and work through the compound interest etc. but hoped the answer might be at the tip of some fingertips on here. I wasn't wrong!!

So, the lock-in is fine. I'm not going to need the money, I just need it to be somewhere tax free. Given the AERs are the same, why WOULD anyone pick one version over the other? Kind of a rhetorical question, but curious if there are reasons.4 -

I get interest paid anually to provide me with an income.Some do it to work tax in their favour.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards