We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Bonds via funds

Comments

-

It doesn't stipulate how the received interest is to be distributed though....only that it is distributed.Could the explanation be that interest received is only taxed if it's not distributed, and that outgoing distribution of received interest can be as an outgoing dividend or as an outgoing interest payment (which depends on the equity content of the fund).Likewise, on the flip side, dividends from equities are distributed as interest where the equity content of the fund is below 40%.0

-

MK62 said:It doesn't stipulate how the received interest is to be distributed though....only that it is distributed.Could the explanation be that interest received is only taxed if it's not distributed, and that outgoing distribution of received interest can be as an outgoing dividend or as an outgoing interest payment (which depends on the equity content of the fund).Likewise, on the flip side, dividends from equities are distributed as interest where the equity content of the fund is below 40%.Then why is £3.3m of corporation tax being deducted from the income before it gets distributed as a dividend (line 7 below)? This doesn't happen for a simple bond fund where interest income is paid out in interest distributions. The net tax in that case is zero.HSBC Global Strategy Balanced:

HSBC Corporate Bond:

HSBC Corporate Bond: Edit: To complete the picture, I've just taken a look at HSBC Global Strategy Cautious. This is still a fund of funds, but distributes interest as it is 20% bonds. There is still some corporation tax being charged:

Edit: To complete the picture, I've just taken a look at HSBC Global Strategy Cautious. This is still a fund of funds, but distributes interest as it is 20% bonds. There is still some corporation tax being charged: and, broken down, some income was exempt, but most was not:

and, broken down, some income was exempt, but most was not: So you may well be correct that the type of distribution is irrelevant. But why then is some of the distributed income net of corporation tax in both of the fund of funds, but not the simple fund?1

So you may well be correct that the type of distribution is irrelevant. But why then is some of the distributed income net of corporation tax in both of the fund of funds, but not the simple fund?1 -

Is it helpful to distinguish between notional and actual distribution? Perhaps OEICs are treated differently to individuals in this respect. The Global Strategy Portfolios are predominantly accumulation share classes whereas the Corporate Bond Fund might be expected to be mainly income share class. I’m doubting whether being a minority income shareholder in Global Strategy would be beneficial as the tax could affect the whole Fund rather than just certain share classes. It might be preferable to have an income-designated fund of funds with no accumulation class rather than these Funds giving both options. What could be examined, with an emphasis on low cost index tracking?

0 -

masonic said:MK62 said:It doesn't stipulate how the received interest is to be distributed though....only that it is distributed.Could the explanation be that interest received is only taxed if it's not distributed, and that outgoing distribution of received interest can be as an outgoing dividend or as an outgoing interest payment (which depends on the equity content of the fund).Likewise, on the flip side, dividends from equities are distributed as interest where the equity content of the fund is below 40%.Then why is £3.3m of corporation tax being deducted from the income before it gets distributed as a dividend (line 7 below)? This doesn't happen for a simple bond fund where interest income is paid out in interest distributions. The net tax in that case is zero.So you may well be correct that the type of distribution is irrelevant. But why then is some of the distributed income net of corporation tax in both of the fund of funds, but not the simple fund?Perhaps only a corporation tax expert can answer this.........from the figures, it does look as if interest received by the fund from bonds in the GS fund is taxed upfront, regardless of how much of that is subsequently distributed.......this does appear at odds with how it works in the bond fund......more digging on this is needed I think.......1

-

You can see from the information provided that all of the net income was distributed in the case of the fund of funds, and all of the gross income wss distributed in the case of the simple fund. OEICs have to distribute all of their income. That's why there is never Excess Reportable Income in the case of distributing classes of OEICs.MK62 said:masonic said:MK62 said:It doesn't stipulate how the received interest is to be distributed though....only that it is distributed.Could the explanation be that interest received is only taxed if it's not distributed, and that outgoing distribution of received interest can be as an outgoing dividend or as an outgoing interest payment (which depends on the equity content of the fund).Likewise, on the flip side, dividends from equities are distributed as interest where the equity content of the fund is below 40%.Then why is £3.3m of corporation tax being deducted from the income before it gets distributed as a dividend (line 7 below)? This doesn't happen for a simple bond fund where interest income is paid out in interest distributions. The net tax in that case is zero.So you may well be correct that the type of distribution is irrelevant. But why then is some of the distributed income net of corporation tax in both of the fund of funds, but not the simple fund?The implication then, is that HSBC Corporate Bond is operating tax free.........I very much doubt that's the case, but perhaps only a corporation tax expert can explain this fully, but to me it just looks like there is no tax because everything which was liable to tax was distributed, but in the case of the GS funds, it was not.

1 -

Compound_2 said:

Is it helpful to distinguish between notional and actual distribution? Perhaps OEICs are treated differently to individuals in this respect. The Global Strategy Portfolios are predominantly accumulation share classes whereas the Corporate Bond Fund might be expected to be mainly income share class. I’m doubting whether being a minority income shareholder in Global Strategy would be beneficial as the tax could affect the whole Fund rather than just certain share classes. It might be preferable to have an income-designated fund of funds with no accumulation class rather than these Funds giving both options. What could be examined, with an emphasis on low cost index tracking?

In the HSBC Corporate Bond fund we previously looked at the Acc unit class was almost three times the size of the Inc unit class. It paid zero net corporation tax. It is almost unheard of for OEICs not to offer an Acc unit class as they are so popular with investors.I think I'm back at the theory that it is related to the statement in the annual report that: "Where a Fund holds an investment in any other onshore or offshore fund that during the Fund’s accounting period is broadly greater than 60% invested, directly or indirectly (through similar funds or derivatives) in cash, bonds or derivatives linked to similar assets, any amounts accounted for as income will be taxable income of the Fund for the period concerned."This would mean that investing in fund of funds that include bond sub-funds instead of direct bond holdings is tax inefficient and it would be better to get your bond exposure separately via a simple fund. After some further digging around, multi-asset funds from other providers, whether OEICs or UTs, are the same. However, the single asset class fund of funds, HL Multi-Manager Strategic Bond Trust (a UT), is in the non-corporation tax paying camp.1 -

I've explored a range of funds to see if it would help explain the differences in taxation. Here is a summary of the results:

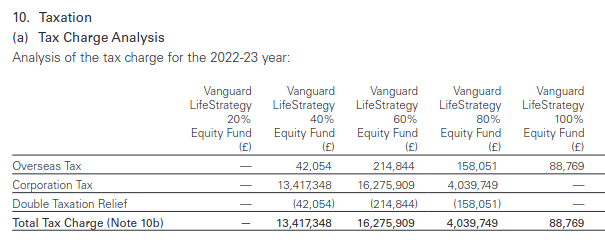

HL Multi-Index Cautious paid no corporation tax, but only made notional distributions as it only has Acc units, so the theory about physical distribution of income can be discounted.The L&G annual reports showed a breakdown for taxation and included overseas tax. I thought for a moment that some of the other funds might have been listing overseas tax as "corporation tax", but L&G Multi Index 3 showed separate amounts for overseas tax and corporation tax.One further thing that is interesting is that the amount in equities vs fixed interest seems to matter. VLS 20 paid no corporation tax, but VLS 40-80 did. The same trend is seen for HL Multi-Index, but not L&G Multi-index or HSBC Global Strategy. Perhaps the lowest equity version of these was still over a %-equities threshold for some or all of the year in question? The latter series are volatility managed, not fixed %-equities.Given that there are examples of pure bond funds of funds and very low equity mixed asset funds of funds that did not pay corporation tax, it seems to be the asset mix rather than the fact they are funds of funds that is important.I think the most striking thing is the comparison between VLS 20 and VLS 40. These are pretty much identical in all respects other than the weightings of the holdings. One paid corporation tax and the other did not.

HL Multi-Index Cautious paid no corporation tax, but only made notional distributions as it only has Acc units, so the theory about physical distribution of income can be discounted.The L&G annual reports showed a breakdown for taxation and included overseas tax. I thought for a moment that some of the other funds might have been listing overseas tax as "corporation tax", but L&G Multi Index 3 showed separate amounts for overseas tax and corporation tax.One further thing that is interesting is that the amount in equities vs fixed interest seems to matter. VLS 20 paid no corporation tax, but VLS 40-80 did. The same trend is seen for HL Multi-Index, but not L&G Multi-index or HSBC Global Strategy. Perhaps the lowest equity version of these was still over a %-equities threshold for some or all of the year in question? The latter series are volatility managed, not fixed %-equities.Given that there are examples of pure bond funds of funds and very low equity mixed asset funds of funds that did not pay corporation tax, it seems to be the asset mix rather than the fact they are funds of funds that is important.I think the most striking thing is the comparison between VLS 20 and VLS 40. These are pretty much identical in all respects other than the weightings of the holdings. One paid corporation tax and the other did not. 2

2 -

Thanks, masonic for all your work investigating this.Would the situation be the same for bonds in pension funds via the so-called 'insured units' being discussed on another thread?0

-

Well there are lots of different pension funds, including those that mirror OIECs and UTs, house funds, those that are funds of funds, etc. I don't think the information will be as readily available as it is for retail investment funds. I don't recall seeing annual reports for pension funds I have held in the past. All of my pension holdings are currently in SIPPs and invested in a mixture of OEICs and ETFs, none of which are multi-asset, so I am not at all familiar with that type of investment.Compound_2 said:Thanks, masonic for all your work investigating this.Would the situation be the same for bonds in pension funds via the so-called 'insured units' being discussed on another thread?

1 -

Of the bond-heavy funds not liable for tax, it seems most have charges that are uncompetitive compared to HSBC Global Strategy. The exception is VLS20 although even this may not win against Global Strategy Cautious on performance.Would we now say a 50:50 split between VLS100 and VLS20 might be better than VLS60? Could combining VLS20 with a standard global tracker be more desirable than Global Strategy Balanced?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards