We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Delete

Comments

-

Removed as didn't read the screenshot correctly.0

-

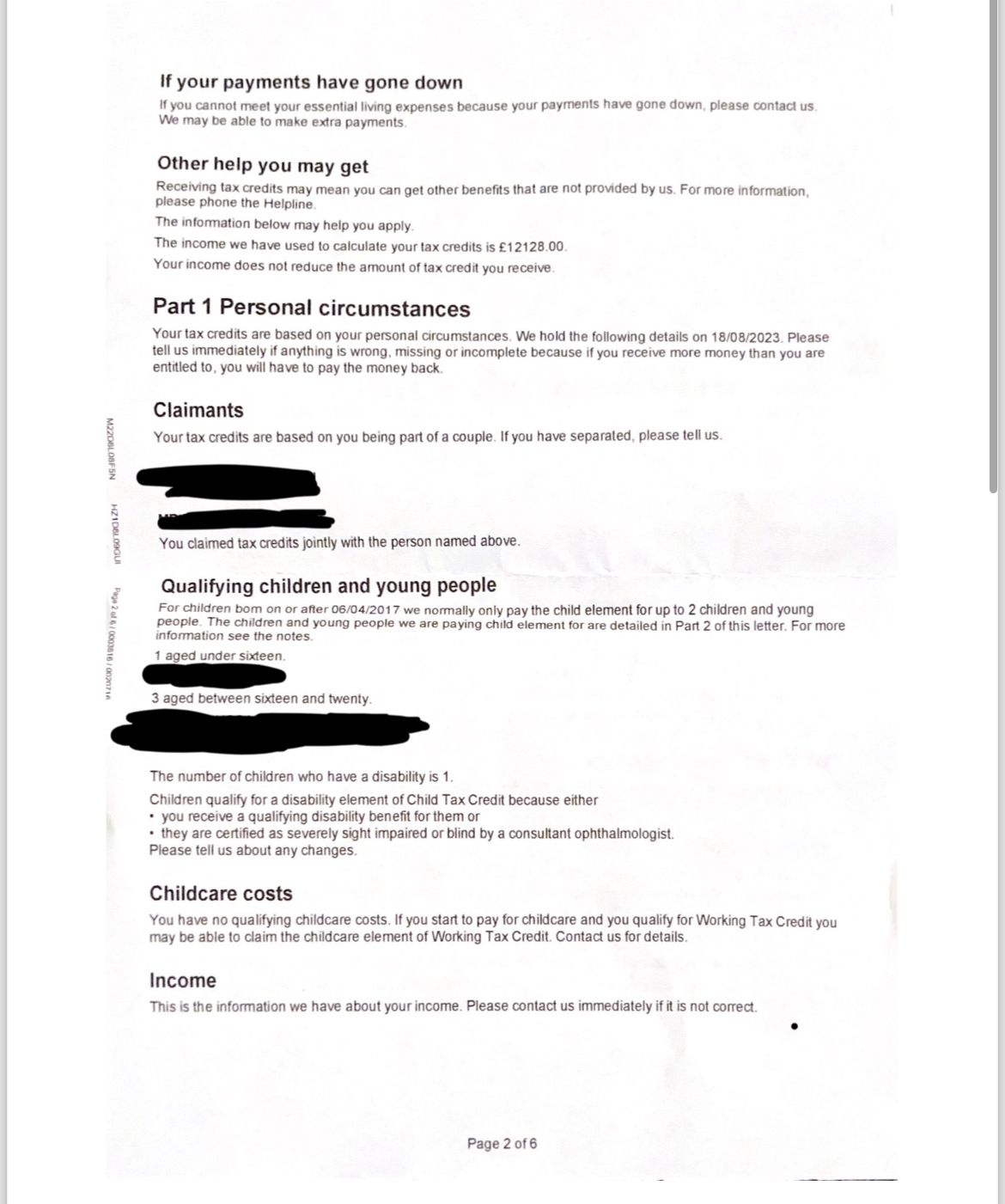

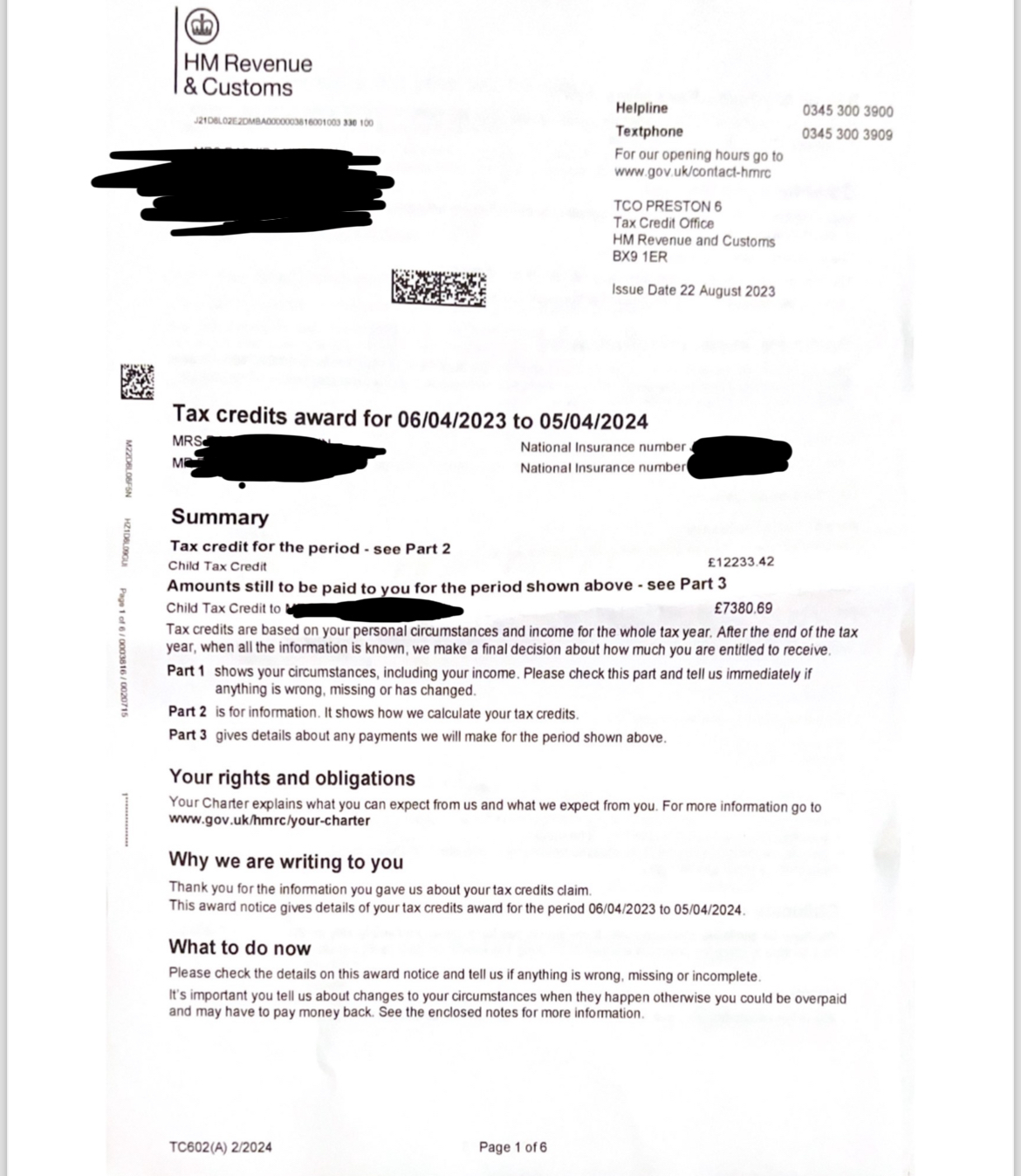

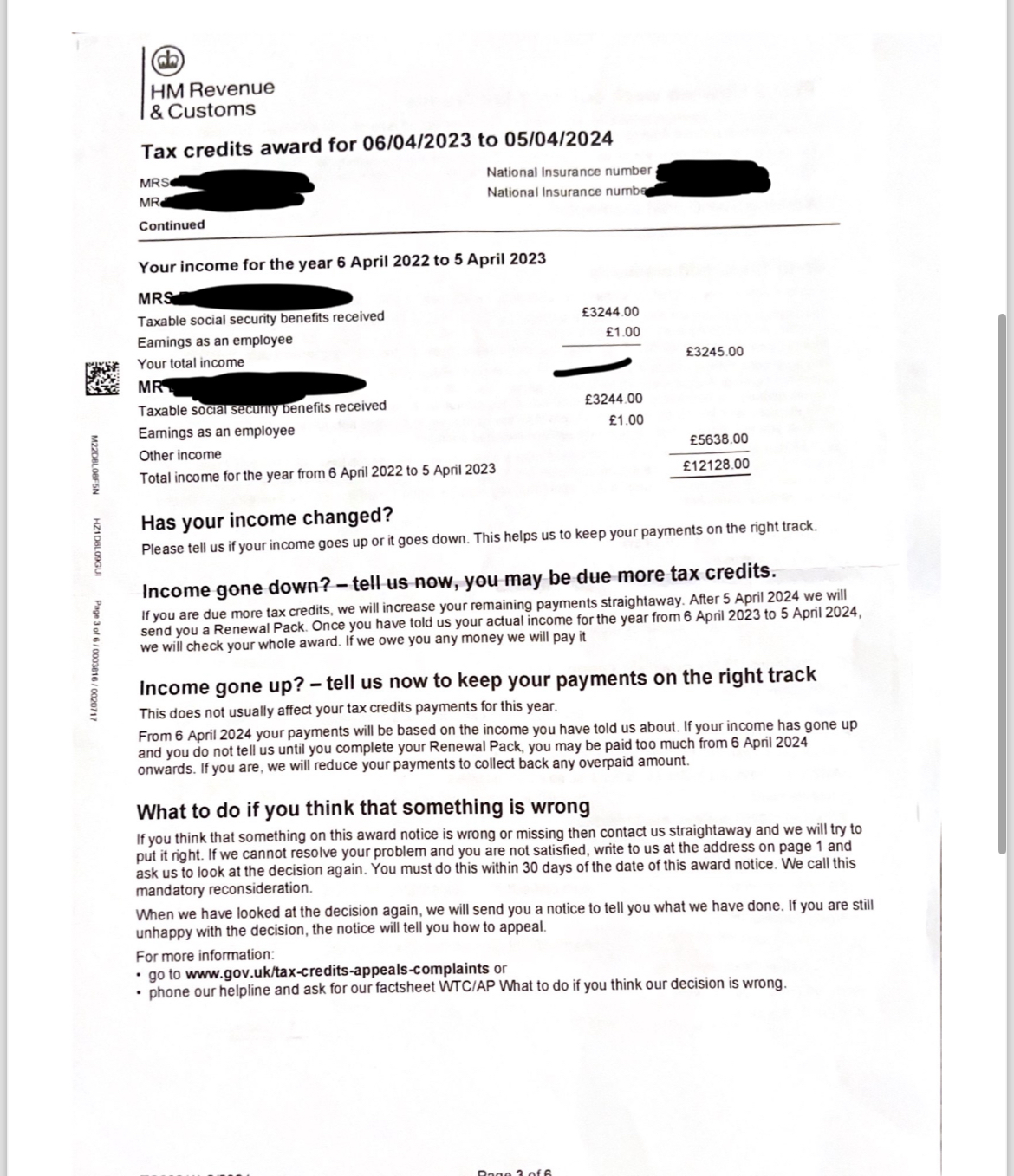

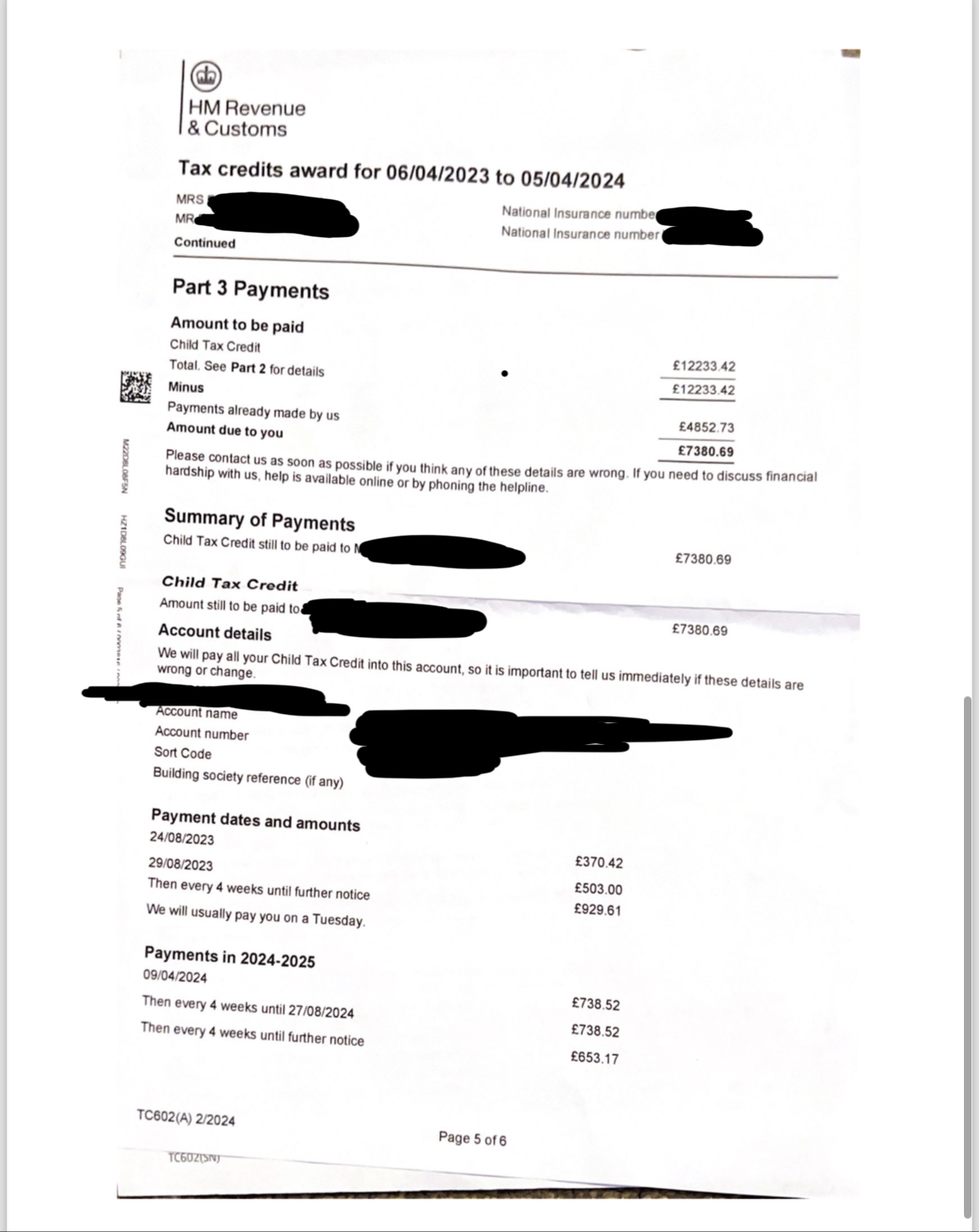

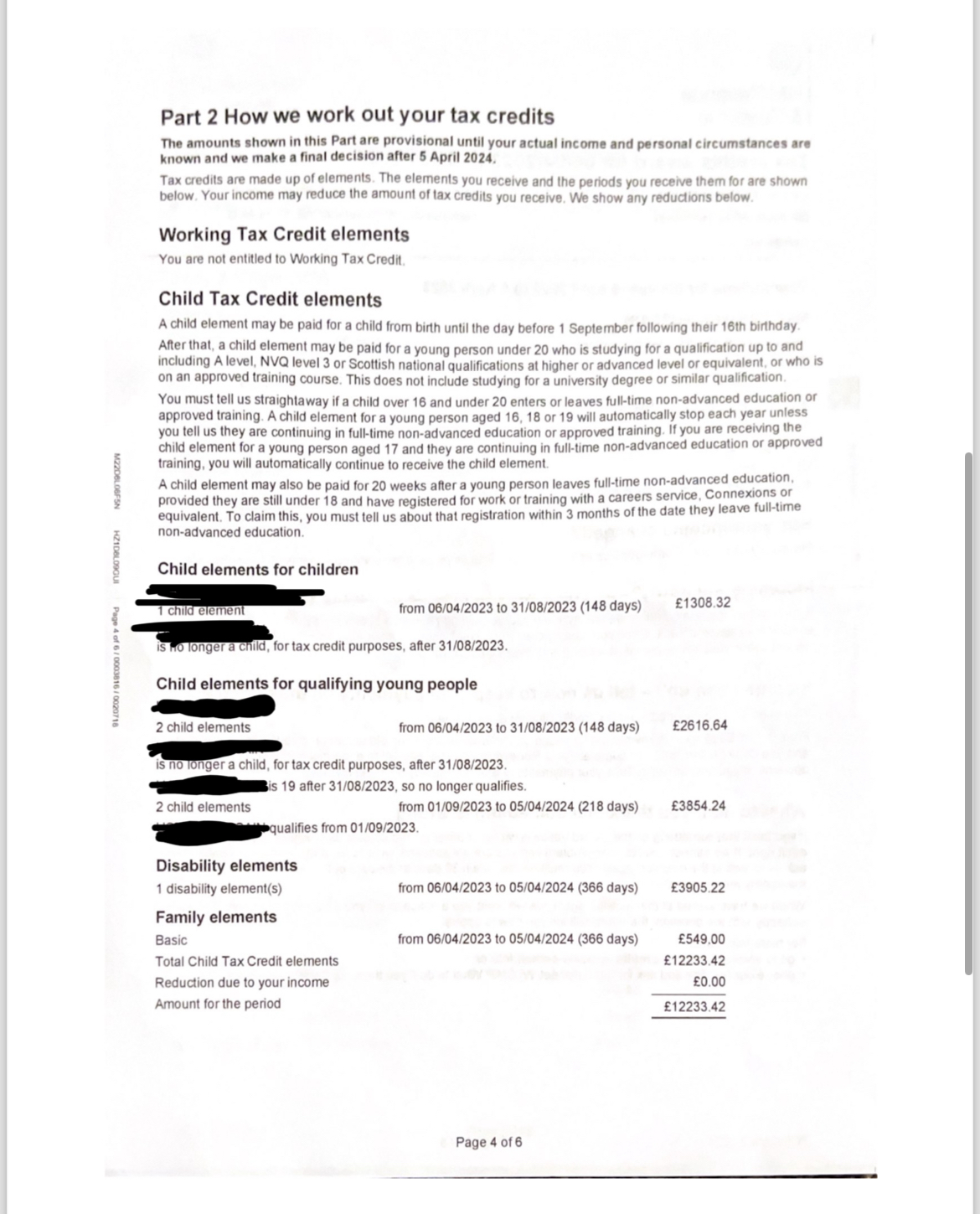

Exactly, so they were no longer entitled to tax credits for the 19 year old. Same applies to UC as they are no longer a dependent child or qualifying young person there's no entitlement to child element for them. They are only entitled to 2 child elements.Hi2928828292 said:It says this on the tax credit award letter dated 2023 AugustOn the tax credit it says the child who is turning 19y is no longer a child, for tax credit purposes, after 31/08/2023. 19y is 19 after 31/08/2023, so no longer qualifies. 2 child elements from 01/09/2023 to 05/04/2024 (218 days)

1 -

If you post up an anonymised copy of their latest tax credits award notice received before the UC claim was made, then I may be able to advise.

Please note: this must be the LAST award notice from tax credits for the 23/24 tax year, but DATED before the UC claim was made.0 -

I've just looked at it again, and I can see what the error was even without you posting the tax credits award notice.

In the calculation of the Transitional Element, they seem to have only included the Carer's Allowance income for one of them, not both. This has led to a transitional element of £104.40 instead of £436.98.

I would write to them again as follows:

1) Please can you provide the breakdown of the transitional element calculation. Specifically, can you confirm that two sets of unearned income from Carer's Allowance were taken into account in the calculation of the Indicative UC Amount.

2) Please refer it to a Decision Maker to carry out a Mandatory Reconsideration on the decision as to the amount of entitlement, on the grounds that the transitional element was not calculated correctly, and is too low.3 -

I have a few minutes spare, and I thought people might find it interesting/helpful to see the breakdown of a transitional element calculation. The case in this thread is also one of the more straightforward examples. So here goes:

First, we have to calculate what is known as the "Total Legacy Amount". In this case, it is the representative monthly amount of entitlement to tax credits (which is not necessarily the same as the weekly or 4-weekly tax credits payments actually in payment at the point of the UC claim).

This is calculated by taking the "daily rate" from HMRC for the award. In this case, the daily rate is fairly straightforward because the household income is below the child tax credit threshold, so there is no taper in the tax credits award.

This family are entitled to the following elements of CTC:

Family element: £545

2*Child element: 2*£3,235

Disabled child element: £3,905

The daily rate for each is found by dividing by 366 (the number of days in 23/24), and rounding up to the nearest penny.

(HMRC have made an error with the family element this year, and have been using a daily rate which is 1p too high. They have recognised this mistake, and have said they will be leaving it as is, so that is also the figure used for this calculation.)

As such, the daily rates are as follows:

Family element: £1.50

2*Child element: 2*£8.84

Disabled child element: £10.67

TOTAL: £29.85

This is then converted to a monthly amount by multiplying by 365 (despite it being a leap year) and then dividing by 12:

£29.85 * 365 / 12 = £907.94

This is the "Total Legacy Amount".

Then we have to calculate the "Indicative UC Amount". In this case, it includes the following elements:

Standard allowance: £578.82

Child element (first child): £315

Child element (second child): £269.58

Disabled child (lower rate): £146.31

2*Carer element: 2*£185.86

TOTAL: £1,681.43

From this is deducted:

Pension income: £545.31

2*Carer's Allowance: 2*£332.58 (weekly rate is £76.75, multiplied by 52 and divided by 12 equals £332.58)

TOTAL: £1,210.47

Net amount of UC: £1,681.43 - £1,210.47 = £470.96.

This is the "Indicative UC Amount".

As the Total Legacy Amount is higher than the Indicative UC Amount, the transitional element is equal to the difference:

£907.94 - £470.96 = £436.98.

This should therefore be the transitional element in this case.

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

6 -

Thank you so much!

Yamor said:I have a few minutes spare, and I thought people might find it interesting/helpful to see the breakdown of a transitional element calculation. The case in this thread is also one of the more straightforward examples. So here goes:

Yamor said:I have a few minutes spare, and I thought people might find it interesting/helpful to see the breakdown of a transitional element calculation. The case in this thread is also one of the more straightforward examples. So here goes:

First, we have to calculate what is known as the "Total Legacy Amount". In this case, it is the representative monthly amount of entitlement to tax credits (which is not necessarily the same as the weekly or 4-weekly tax credits payments actually in payment at the point of the UC claim).

This is calculated by taking the "daily rate" from HMRC for the award. In this case, the daily rate is fairly straightforward because the household income is below the child tax credit threshold, so there is no taper in the tax credits award.

This family are entitled to the following elements of CTC:

Family element: £545

2*Child element: 2*£3,235

Disabled child element: £3,905

The daily rate for each is found by dividing by 366 (the number of days in 23/24), and rounding up to the nearest penny.

(HMRC have made an error with the family element this year, and have been using a daily rate which is 1p too high. They have recognised this mistake, and have said they will be leaving it as is, so that is also the figure used for this calculation.)

As such, the daily rates are as follows:

Family element: £1.50

2*Child element: 2*£8.84

Disabled child element: £10.67

TOTAL: £29.85

This is then converted to a monthly amount by multiplying by 365 (despite it being a leap year) and then dividing by 12:

£29.85 * 365 / 12 = £907.94

This is the "Total Legacy Amount".

Then we have to calculate the "Indicative UC Amount". In this case, it includes the following elements:

Standard allowance: £578.82

Child element (first child): £315

Child element (second child): £269.58

Disabled child (lower rate): £146.31

2*Carer element: 2*£185.86

TOTAL: £1,681.43

From this is deducted:

Pension income: £545.31

2*Carer's Allowance: 2*£332.58 (weekly rate is £76.75, multiplied by 52 and divided by 12 equals £332.58)

TOTAL: £1,210.47

Net amount of UC: £1,681.43 - £1,210.47 = £470.96.

This is the "Indicative UC Amount".

As the Total Legacy Amount is higher than the Indicative UC Amount, the transitional element is equal to the difference:

£907.94 - £470.96 = £436.98.

This should therefore be the transitional element in this case.

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

I can’t thank you enough

This is there 2023 to 2024 tax credit award.

0 -

@Yamor I think you may have identified a bug in the way the TP calculator works. Even for a joint claim, it appears to work under one claimant's name. The calculator pre-populates their DoB, asks if they are a carer, if they are in receipt of LCW/LCWRA and pre-populates the tax credits award data etc. There is nowhere AFAIK for the agent to record that both members of a couple are carers. I will investigate further and see what I can find out.Yamor said:

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.Our green credentials: 12kW Samsung ASHP for heating, 7.2kWp Solar (South facing), Tesla Powerwall 3 (13.5kWh), Net exporter2 -

Thanks, I would be really interested to hear!NedS said:

@Yamor I think you may have identified a bug in the way the TP calculator works. Even for a joint claim, it appears to work under one claimant's name. The calculator pre-populates their DoB, asks if they are a carer, if they are in receipt of LCW/LCWRA and pre-populates the tax credits award data etc. There is nowhere AFAIK for the agent to record that both members of a couple are carers. I will investigate further and see what I can find out.Yamor said:

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

It may not be as simple as that, because in this case it DID identify that they were both carers for the purposes of the carer element, just not for the deduction for the Carer's Allowance income.1 -

Sorry, I was mistaken - the TP calculator does have the facility to input caring activity for both the claimant and the partner, but it is not auto-populated so the agent must check what has been declared and complete the todo correctly.Yamor said:

Thanks, I would be really interested to hear!NedS said:

@Yamor I think you may have identified a bug in the way the TP calculator works. Even for a joint claim, it appears to work under one claimant's name. The calculator pre-populates their DoB, asks if they are a carer, if they are in receipt of LCW/LCWRA and pre-populates the tax credits award data etc. There is nowhere AFAIK for the agent to record that both members of a couple are carers. I will investigate further and see what I can find out.Yamor said:

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

It may not be as simple as that, because in this case it DID identify that they were both carers for the purposes of the carer element, just not for the deduction for the Carer's Allowance income.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.Our green credentials: 12kW Samsung ASHP for heating, 7.2kWp Solar (South facing), Tesla Powerwall 3 (13.5kWh), Net exporter1 -

What about income from DWP benefits (incl. Carer's Allowance) - is that auto-populated? And if yes, does it capture the info for both claimants?NedS said:

Sorry, I was mistaken - the TP calculator does have the facility to input caring activity for both the claimant and the partner, but it is not auto-populated so the agent must check what has been declared and complete the todo correctly.Yamor said:

Thanks, I would be really interested to hear!NedS said:

@Yamor I think you may have identified a bug in the way the TP calculator works. Even for a joint claim, it appears to work under one claimant's name. The calculator pre-populates their DoB, asks if they are a carer, if they are in receipt of LCW/LCWRA and pre-populates the tax credits award data etc. There is nowhere AFAIK for the agent to record that both members of a couple are carers. I will investigate further and see what I can find out.Yamor said:

However, in this case, UC seem to have only deducted one Carer's Allowance when calculating the Indicative UC Amount. This therefore left the Indicative UC Amount at £803.54 (£470.96 + £332.58 = £803.54), and the transitional element was therefore calculated as being only: £907.94 - £803.54 = £104.40.

Although this mistake was made for the transitional element calculation, the actual UC award was calculated correctly in this respect, with two deductions made for Carer's Allowance.

This mistake actually brings out the point that the transitional element is calculated as a one-off snapshot, without reference to the actual UC award in the first (and subsequent) assessment periods.

It may not be as simple as that, because in this case it DID identify that they were both carers for the purposes of the carer element, just not for the deduction for the Carer's Allowance income.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards