We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Damages by gardener

Comments

-

You have a duty of care to anyone working on your property which includes removing or safeguarding from potential hazards. I think you need to ask yourself what position you would be in if the gardener had been injured or killed.3

-

Thanks, I thought it sounded odd.user1977 said:

It's completely inaccurate. You don't take on any sort of employer/employee relationship. Your duties to tradespeople are no more and no less than those in relation to any other visitor to your home.

Is there anything to back up this statement?bris said:

Its all very well saying people use extension leads etc but when you get tradesmen in, you become their employer and as such need to make sure they are safe or you are as negligent as any other employer would be.

I don't see that you become an employer, particularly as a tradesperson may have an actual employer, that's not to pass comment on who is responsible, merely a question of how accurate this is")

It would seem this falls under the Occupiers’ Liability Act 1957

https://www.legislation.gov.uk/ukpga/Eliz2/5-6/31

which notes with regards to the owner's duty of care(3)The circumstances relevant for the present purpose include the degree of care, and of want of care, which would ordinarily be looked for in such a visitor, so that (for example) in proper cases—(a)an occupier must be prepared for children to be less careful than adults; and(b)an occupier may expect that a person, in the exercise of his calling, will appreciate and guard against any special risks ordinarily incident to it, so far as the occupier leaves him free to do so.

The question would be whether (3)(b) applies or not, the gardener was "in the exercise of his calling" so it's a question of whether checking for hazards hidden in the grass, perhaps particularly electrical cables, is a special risk ordinarily incident to the action of cutting grass or not.

There's been a few cases in higher courts where (3)(b) has been considered although the circumstances appear to vary, I only had a brief look but didn't see one relating to a tradesperson and a homeowner.

As a side note there is also the Occupiers Liability Act 1984 but this applies to those who are not visitors (i.e those who enter land/property without permission).In the game of chess you can never let your adversary see your pieces0 -

it is occupier's liability, insurance for which often comes with house contents insurance

leaving a cable hidden in the grass and then telling someone to come and cut the grass is ... well not sure of the word !0 -

I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.user1977 said:

It's completely inaccurate. You don't take on any sort of employer/employee relationship. Your duties to tradespeople are no more and no less than those in relation to any other visitor to your home.

Is there anything to back up this statement?bris said:

Its all very well saying people use extension leads etc but when you get tradesmen in, you become their employer and as such need to make sure they are safe or you are as negligent as any other employer would be.

I don't see that you become an employer, particularly as a tradesperson may have an actual employer, that's not to pass comment on who is responsible, merely a question of how accurate this is

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either and I don’t see why a gardener would be any different.

https://help.quotemehappy.com/home-insurance/my-cover/what-is-occupier-s-personal-and-employer-s-liability-insurance/#:~:text=Liability%20cover%20is%20insurance%20which,employer%20of%20a%20domestic%20employee.

Northern Ireland club member No 382 :j0 -

Always happy to be correctedMoney_Grabber13579 said:I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either and I don’t see why a gardener would be any different.

https://help.quotemehappy.com/home-insurance/my-cover/what-is-occupier-s-personal-and-employer-s-liability-insurance/#:~:text=Liability%20cover%20is%20insurance%20which,employer%20of%20a%20domestic%20employee. but, I doubt you have employer’s liability insurance, it is a legal requirement for any employer to have employer’s liability insurance with fines of up to £2500 per day that you don't have cover, your home insurance offering cover for your liability to someone you "employ" to work on your land/property is likely different, the term "employ" could be substituted for any number of words in this situation.

There isn't a suggestion of there being no liability at all rather that the liability that does exist between a homeowner and tradesperson doesn't meet the high standards of liability that exists between employers and employees under employment law, as Bris inferred.In the game of chess you can never let your adversary see your pieces0 -

No, that would be exactly the same as any other tradesperson visiting your home, unless you were actually their employer (i.e. signing them up to an employment contract). If you're not at risk of them taking you to an Employment Tribunal, why would you be considered their employer for liability purposes?Money_Grabber13579 said:

I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.user1977 said:

It's completely inaccurate. You don't take on any sort of employer/employee relationship. Your duties to tradespeople are no more and no less than those in relation to any other visitor to your home.

Is there anything to back up this statement?bris said:

Its all very well saying people use extension leads etc but when you get tradesmen in, you become their employer and as such need to make sure they are safe or you are as negligent as any other employer would be.

I don't see that you become an employer, particularly as a tradesperson may have an actual employer, that's not to pass comment on who is responsible, merely a question of how accurate this is

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either

Obviously people who do actually have domestic staff would need such cover, which is probably why it's chucked into the policy. My own insurer describes employer's liability as being:

"Your or your family’s liability as a result of accidental bodily injury, illness or disease of any person you or your family employ as domestic staff under a contract of employment."1 -

Don't fall into the trap, as many do, of thinking along the lines of 'Mrs Mopp only does two hours a week on Thursdays, surely she can't be my employee'.

Always happy to be correctedMoney_Grabber13579 said:I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either and I don’t see why a gardener would be any different.

https://help.quotemehappy.com/home-insurance/my-cover/what-is-occupier-s-personal-and-employer-s-liability-insurance/#:~:text=Liability%20cover%20is%20insurance%20which,employer%20of%20a%20domestic%20employee. but, I doubt you have employer’s liability insurance, it is a legal requirement for any employer to have employer’s liability insurance with fines of up to £2500 per day that you don't have cover, your home insurance offering cover for your liability to someone you "employ" to work on your land/property is likely different, the term "employ" could be substituted for any number of words in this situation.

There isn't a suggestion of there being no liability at all rather that the liability that does exist between a homeowner and tradesperson doesn't meet the high standards of liability that exists between employers and employees under employment law, as Bris inferred.

She can and probably is. There’s no single rule that determines whether or not a home help (which can include a nanny or gardener too) is self-employed or your employee. It all boils down to the terms and conditions of your arrangement. If they work set hours each week, use your bucket or your lawnmower, you tell them what to do and how you want it done then you are their employer and carry the full burden of employers' responsibilities (right to work in UK, minimum wage, unfair dismissal, redundancy, employer's liability insurance, etc.)

The only sure way to avoid it is either to hire them through an agency or make absolutely sure they meet HMRC's rules for self-employment (bring their own bucket, etc.)3 -

I think you've probably over-estimated that likelihood. If Mrs Mopp is operating her own business, paying her tax direct, invoices for her work, does her work unsupervised, sets her own prices and quotes for work, and works for 3 other houses in the street then she's much more probably self-employed.Alderbank said:

Don't fall into the trap, as many do, of thinking along the lines of 'Mrs Mopp only does two hours a week on Thursdays, surely she can't be my employee'.

Always happy to be correctedMoney_Grabber13579 said:I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either and I don’t see why a gardener would be any different.

https://help.quotemehappy.com/home-insurance/my-cover/what-is-occupier-s-personal-and-employer-s-liability-insurance/#:~:text=Liability%20cover%20is%20insurance%20which,employer%20of%20a%20domestic%20employee. but, I doubt you have employer’s liability insurance, it is a legal requirement for any employer to have employer’s liability insurance with fines of up to £2500 per day that you don't have cover, your home insurance offering cover for your liability to someone you "employ" to work on your land/property is likely different, the term "employ" could be substituted for any number of words in this situation.

There isn't a suggestion of there being no liability at all rather that the liability that does exist between a homeowner and tradesperson doesn't meet the high standards of liability that exists between employers and employees under employment law, as Bris inferred.

She can and probably is. There’s no single rule that determines whether or not a home help (which can include a nanny or gardener too) is self-employed or your employee. It all boils down to the terms and conditions of your arrangement. If they work set hours each week, use your bucket or your lawnmower, you tell them what to do and how you want it done then you are their employer and carry the full burden of employers' responsibilities (right to work in UK, minimum wage, unfair dismissal, redundancy, employer's liability insurance, etc.)

The only sure way to avoid it is either to hire them through an agency or make absolutely sure they meet HMRC's rules for self-employment (bring their own bucket, etc.)

0 -

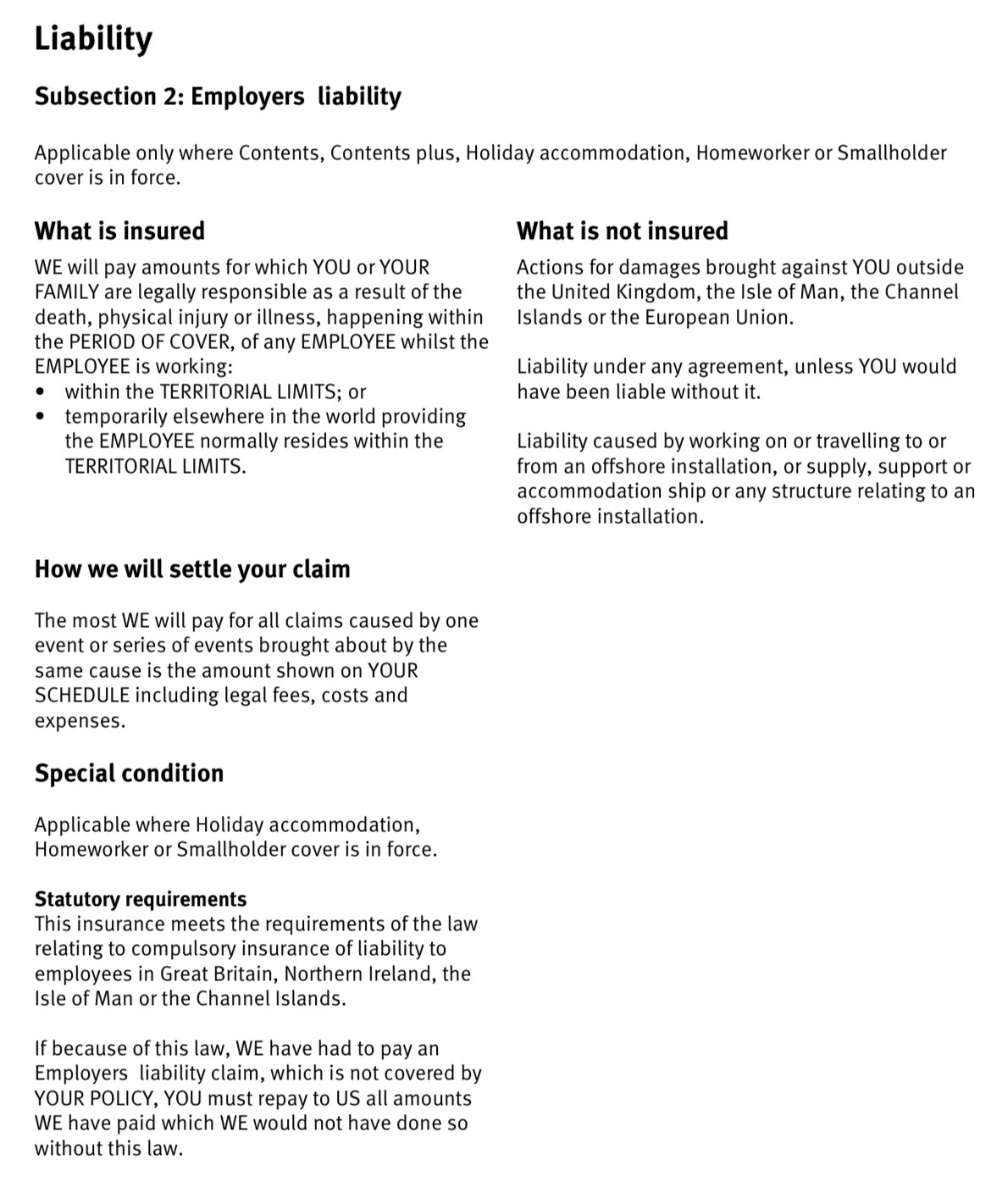

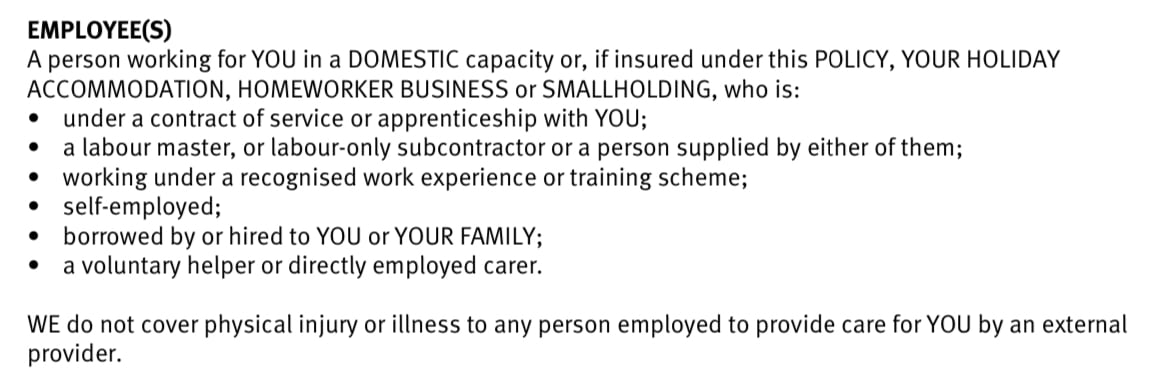

I do have employers liability insurance, it comes with my contents insurance. This is what my policy documents say about the insurance i.e. death or injury of any employee whilst working in my premises. For the avoidance of doubt, I don’t run any business from my house or have any business insurance.

Always happy to be correctedMoney_Grabber13579 said:I’m not sure it is completely inaccurate. I have employer’s liability insurance on my own household policy and my insurance company told me that it was to cover for any claims made by people I’d engaged to work on my property.

This link also summarises the different types of liability insurance and specifically mentions a cleaner as a circumstance in which employers liability insurance would be required. That wouldn’t be a standard employer/employee relationship either and I don’t see why a gardener would be any different.

https://help.quotemehappy.com/home-insurance/my-cover/what-is-occupier-s-personal-and-employer-s-liability-insurance/#:~:text=Liability%20cover%20is%20insurance%20which,employer%20of%20a%20domestic%20employee. but, I doubt you have employer’s liability insurance, it is a legal requirement for any employer to have employer’s liability insurance with fines of up to £2500 per day that you don't have cover, your home insurance offering cover for your liability to someone you "employ" to work on your land/property is likely different, the term "employ" could be substituted for any number of words in this situation.

There isn't a suggestion of there being no liability at all rather that the liability that does exist between a homeowner and tradesperson doesn't meet the high standards of liability that exists between employers and employees under employment law, as Bris inferred. However, employee is a defined term and includes anyone working for me in a domestic capacity. I think it’s hard to say that a cleaner or gardener isn’t someone who is working for me in a domestic capacity. It’s not clear to me if the bullets also apply to people working in a domestic capacity or if they only apply to holiday accommodation, Homeworker business or smallholding, but if they do, then I think it puts it without doubt.

However, employee is a defined term and includes anyone working for me in a domestic capacity. I think it’s hard to say that a cleaner or gardener isn’t someone who is working for me in a domestic capacity. It’s not clear to me if the bullets also apply to people working in a domestic capacity or if they only apply to holiday accommodation, Homeworker business or smallholding, but if they do, then I think it puts it without doubt. Northern Ireland club member No 382 :j0

Northern Ireland club member No 382 :j0 -

I would say that's just a definition which the insurer is using for the purposes of their policy, it doesn't reflect a more general legal implication of an employer/employee relationship.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards