We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Short Term Gilts

Comments

-

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.1 -

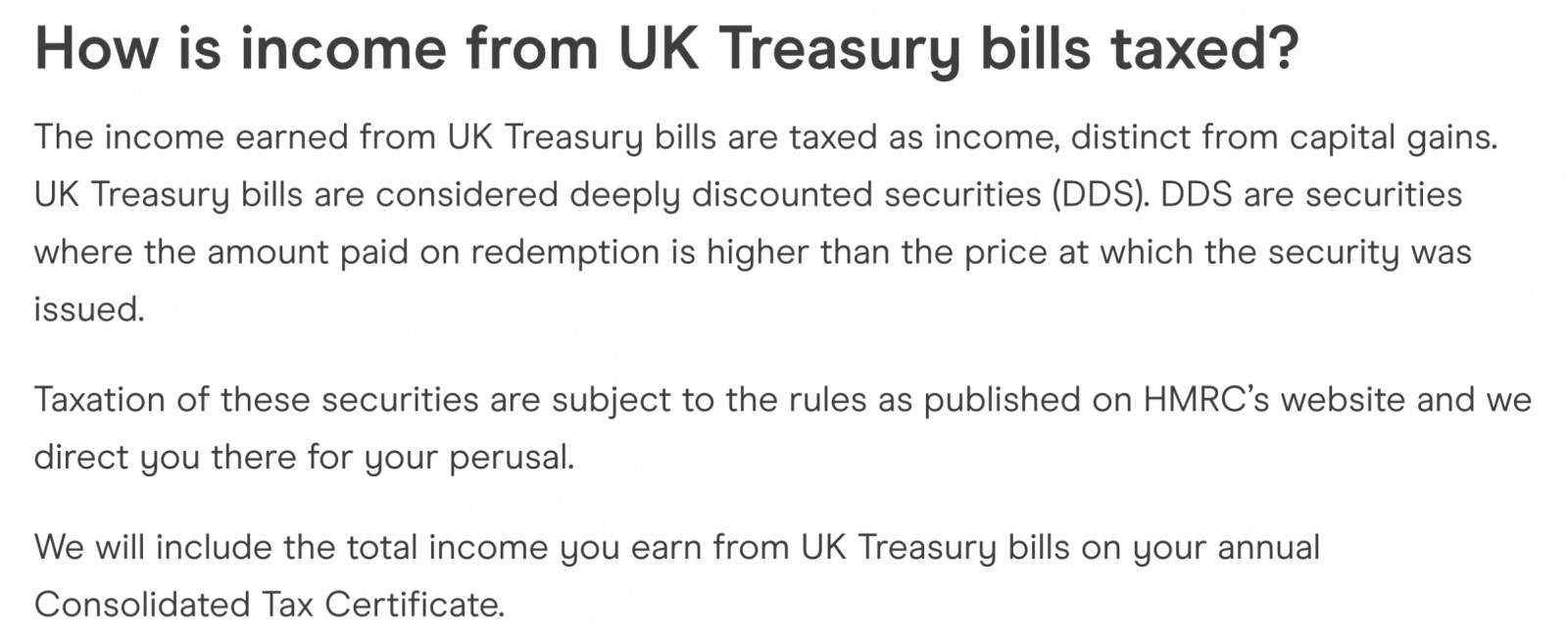

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.

3 -

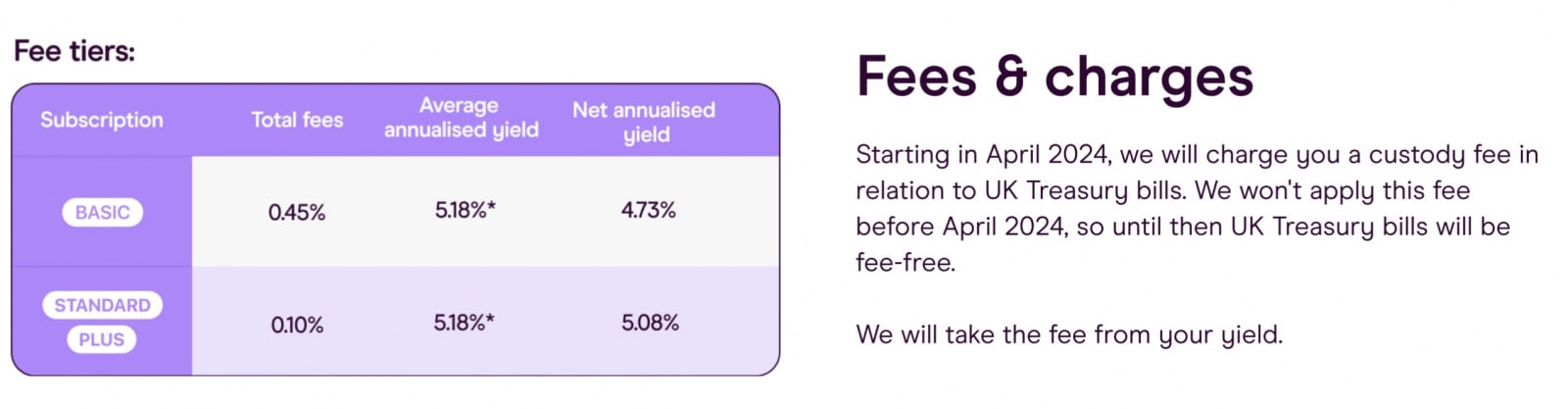

Freetrade recently announced the charges, see below.masonic said:brucefan_2 said:

Thanks for the reply.InvesterJones said:brucefan_2 said:Please excuse me if I'm missing something very obvious.

I'm struggling to see any advantage in the Freetrade UK Treasury Bills offering, given that I can (still just about) get 5.2% in an Easy Access Account.

I'm happy to say I don't know what I don't know but I can't figure out what job these would do in a portfolio.

I'd really appreciate it if someone who uses them could clarify for me what role they serve or maybe point me towards something I could read, which explains.

TIA

They're not easy access cash, so if you need that then of course you wouldn't consider these. However gilts are fixed coupon so you're guaranteed the return, while easy access cash is usually variable. Any capital gain on gilts is also free of tax, while there is no capital gain on cash and interest is taxed up to 45%.

I get that EA cash accounts are liable to rate changes but most providers currently give good notice of these coming into effect. The PSA also influences the tax levels on interest.

I'm having difficulty articulating the question but I guess I don't understand potential scenarios where these Treasury Bills might fit into an investment/savings strategy.

Thanks again.I think your question is why would someone not instead opt for the best easy access or notice account available at the time. There are several reasons someone might prefer something like this. For example, convenience. It means not having to chase the best rate and move money around. Though a money market fund would make things even more convenient, those carry slightly different risks. These Bills might also be somewhere to temporarily park cash held within a S&S ISA or SIPP with Freetrade. Also, if someone is not resident in the UK, they may be unable to open new savings accounts, but often can manage existing investment accounts.I don't think it is advisable for the typical forumite to use these, but for someone who doesn't like opening new accounts, but wants to get a fair market rate on their capital, something like this could fit the bill. Of course a lot depends on the so far undisclosed charges that will be deducted after April.

https://freetrade.io/treasury

2 -

Yep was just talking about Gilts above - have never looked into US Treasury Bills.wmb194 said:

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.0 -

I was talking about *UK* Treasury bills, which are the subject of Brucefan's recent comments re Freetrade and its offering of them.MacPingu1986 said:

Yep was just talking about Gilts above - have never looked into US Treasury Bills.wmb194 said:

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.1 -

Ouch!wmb194 said:

Freetrade recently announced the charges, see below.masonic said:brucefan_2 said:

Thanks for the reply.InvesterJones said:brucefan_2 said:Please excuse me if I'm missing something very obvious.

I'm struggling to see any advantage in the Freetrade UK Treasury Bills offering, given that I can (still just about) get 5.2% in an Easy Access Account.

I'm happy to say I don't know what I don't know but I can't figure out what job these would do in a portfolio.

I'd really appreciate it if someone who uses them could clarify for me what role they serve or maybe point me towards something I could read, which explains.

TIA

They're not easy access cash, so if you need that then of course you wouldn't consider these. However gilts are fixed coupon so you're guaranteed the return, while easy access cash is usually variable. Any capital gain on gilts is also free of tax, while there is no capital gain on cash and interest is taxed up to 45%.

I get that EA cash accounts are liable to rate changes but most providers currently give good notice of these coming into effect. The PSA also influences the tax levels on interest.

I'm having difficulty articulating the question but I guess I don't understand potential scenarios where these Treasury Bills might fit into an investment/savings strategy.

Thanks again.I think your question is why would someone not instead opt for the best easy access or notice account available at the time. There are several reasons someone might prefer something like this. For example, convenience. It means not having to chase the best rate and move money around. Though a money market fund would make things even more convenient, those carry slightly different risks. These Bills might also be somewhere to temporarily park cash held within a S&S ISA or SIPP with Freetrade. Also, if someone is not resident in the UK, they may be unable to open new savings accounts, but often can manage existing investment accounts.I don't think it is advisable for the typical forumite to use these, but for someone who doesn't like opening new accounts, but wants to get a fair market rate on their capital, something like this could fit the bill. Of course a lot depends on the so far undisclosed charges that will be deducted after April.

https://freetrade.io/treasury

1 -

Ok cool - My post was about Gilts, not other stuff where I'll happily defer to your knowledge!wmb194 said:

I was talking about *UK* Treasury bills, which are the subject of Brucefan's recent comments re Freetrade and its offering of them.MacPingu1986 said:

Yep was just talking about Gilts above - have never looked into US Treasury Bills.wmb194 said:

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.0 -

MacPingu1986 said:

Ok cool - My post was about Gilts, not other stuff where I'll happily defer to your knowledge!wmb194 said:

I was talking about *UK* Treasury bills, which are the subject of Brucefan's recent comments re Freetrade and its offering of them.MacPingu1986 said:

Yep was just talking about Gilts above - have never looked into US Treasury Bills.wmb194 said:

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.

Wmb194's point was you're both talking about the same thing. Gilts = UK treasury bills.

1 -

But you need to be careful with one month bills as their capital gains are treated as interest and are not CGT-free as gilts normally are.InvesterJones said:MacPingu1986 said:

Ok cool - My post was about Gilts, not other stuff where I'll happily defer to your knowledge!wmb194 said:

I was talking about *UK* Treasury bills, which are the subject of Brucefan's recent comments re Freetrade and its offering of them.MacPingu1986 said:

Yep was just talking about Gilts above - have never looked into US Treasury Bills.wmb194 said:

You need to be careful with these; even though you technically make a capital gain with them the returns on Treasury Bills are classified as interest as they're considered to be deeply discounted securities.MacPingu1986 said:

If I've understood correctly, these cannot yet be held within an ISA or SIPP wrapper.

Your point that these are probably not for the typical forumite makes a lot of sense but the low entry threshold of £50 to participate is probably designed to attract a wider range of clients.

I've just done a quick check - not the most competitive but a Zopa 31 day notice account currently offers 4.65% AER with no platform charge.

I've been using Freetrade pretty much from the outset and invested in them also. This is an interesting development but I'm left wondering whether this is intended to be more of use to the client or to Freetrade itself, via its charges.

Thanks for taking the time to reply.

To briefly follow on from what Masonic & Invester Jones said - I think the most likely scenario where you might want to use Gilts in the current environment is to use them as a sort of quasi short term savings (lets say you'll want the cash in a year or two for a house deposit), have maxed out your yearly ISA allowances and if you're a higher/additional rate tax payer then that almost entirely tax free return of 4% becomes notionally equivalent to a savings account interest rate of c7%.

Wmb194's point was you're both talking about the same thing. Gilts = UK treasury bills.

https://freetrade.io/uk-treasury#3

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards