We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

WASPI ‘victory’

Comments

-

comes down to the fact that people only want to keep the rules if the old ones were a better deal for the individual.Silvertabby said:I've heard people argue that the rules in place when someone started work should still be applied at retirement, with any new rules only applying to younger people who started work later, ie in full knowledge the new regulations.

If that were the case, then the mid 1970s Sex Equality and Equal Pay Acts wouldn't apply to me or all the others who started work before 1975.

A case of be careful what you wish for.....

good point re these, my first job was in 76 and I can't imagine working without this legislation.2 -

We didn't get any letters about these changes, but we all seemed to know about them!Flugelhorn said:

comes down to the fact that people only want to keep the rules if the old ones were a better deal for the individual.Silvertabby said:I've heard people argue that the rules in place when someone started work should still be applied at retirement, with any new rules only applying to younger people who started work later, ie in full knowledge the new regulations.

If that were the case, then the mid 1970s Sex Equality and Equal Pay Acts wouldn't apply to me or all the others who started work before 1975.

A case of be careful what you wish for.....

good point re these, my first job was in 76 and I can't imagine working without this legislation.2 -

I am a 59 year old Male, I knew all about this, its the same as all the Women who paid lesser NI Contributions, most of them were fully aware and now they are just jumping on a bandwagon of a cause with no wheels, being encouraged by a few people who probably do not need the money anyway.3

-

One has to ask how do I know that I qualify for a state pension at all? Is it reasonable to say:xylophone said:- I have always considered that those affected by the 2011 Act were indeed hard done by.

I have also always considered (in the light of the "Don't die of ignorance" campaign,

https://en.wikipedia.org/wiki/AIDS:_Don't_Die_of_Ignorance

a leaflet was sent to every home in the UK.[2][5][6][7] )

that it was open to the government to send every household a " Don't ignore increase to state pension age" letter (or at the least to require every employer to include such a letter with employees' P60s.

That said, I do find it strange that so many women claim ignorance. Did none of them have any older female friends or relations (mothers, even) who mentioned that they were drawing their state pension later than they had originally expected?

I heard from a bloke down the pub, who'd been talking with his mate, that got in a taxi with this driver, who frequently conveys a politician, that heard from his mate on the Parliamentary sub committee, that maybe, once I get to over 60ish, I can get some free cash.

Or because it is something that affects the quality of my retirement, it should be reasonable to show appropriate engagement to understand my current and future financial state and seek out the information to enable effective decisions, and on a number of occasions highlighting the limitations of the information that has been provided.

If they feel they were unable to plan effectively, they should be required to demonstrate, evidentially, the level of planning they did undertake, how much due diligence they applied to assuring themselves that their future income was sufficient and secure to meet their current and enduring needs.

Anything else is just jumping on the bus.Your life is too short to be unhappy 5 days a week in exchange for 2 days of freedom!2 - I have always considered that those affected by the 2011 Act were indeed hard done by.

-

My current SP age is 67.

It’s likely to rise before I get there. There’s talk about it being 71.

It’s likely to become means tested before I get there; which means my years of NI contributions count for diddly.

Put’s thick Yorkshire accent on; a SP at 65… “luxury”.1 -

I never recieved a letter saying that my state pension age was going up to 66.....

Do I have a claim????

Oh!

What?

I'm a man so no...

lol1 -

You’ve nailed the UK fiscal paradox!ex-pat_scot said:My NI on salary around the £100k mark (after whopping pension contributions, to keep out of the high marginal tax rate) is around £6,400 pa.

At 35 years of this it would give c£225,000 total NI contributions. This is rather unrealistic, but serves to show how modest even a high earner's contributions are, when set against the broad equivalent annuity cost of the SP at around £250,000 and also the other notional social benefits such as NHS, welfare etc.

(My actual NI contributions to date are not much more than £100,000 for 33 full years of contribution and a few partial years - I wasn't a v high earner until later in my career).

1 -

One has to ask how do I know that I qualify for a state pension at all?

Initially, how do we learn much at all about wages and pensions and managing money? I'd suggest from parents/grandparents.

Mary Brown aged 45 in say June 1995 would likely have seen grandmother and mother drawing their state pensions at age 60

and grandfather and father at age 65. She could have been paying NI herself for close on thirty years - and people get used to the

status quo....

The point I was making was that if the government could communicate with all households in 1986, then it was certainly within

its capacity in 1995 to organise an information drop to all women born in 1950 or later.

It would certainly have been simple enough to instruct all employers to include a note or leaflet on the change with the 1996

P60s and even thereafter?

That said, and as I said, it is difficult to believe that large numbers of women had no notion that SPA would increase from 6/4/10.

Even if publicity in the press/television news etc had passed them by, surely most had mothers/aunts/colleagues/neighbours who

would have been affected by the change and commented on it?

1 -

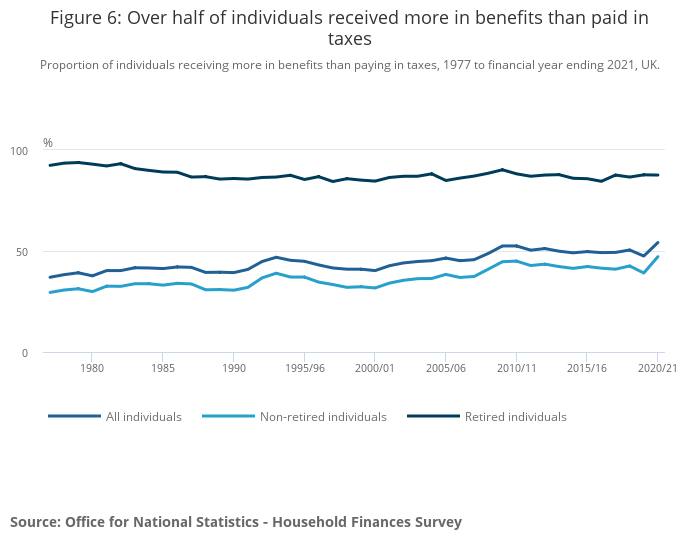

Is there a chart like this that shows the situation over people's entire lifetime rather than annual snapshots which this seems to be?BlackKnightMonty said:

You’ve nailed the UK fiscal paradox!ex-pat_scot said:My NI on salary around the £100k mark (after whopping pension contributions, to keep out of the high marginal tax rate) is around £6,400 pa.

At 35 years of this it would give c£225,000 total NI contributions. This is rather unrealistic, but serves to show how modest even a high earner's contributions are, when set against the broad equivalent annuity cost of the SP at around £250,000 and also the other notional social benefits such as NHS, welfare etc.

(My actual NI contributions to date are not much more than £100,000 for 33 full years of contribution and a few partial years - I wasn't a v high earner until later in my career).

This also neatly highlights that the state pension is considered as a benefit rather than a "right" as it's clearly being considered as a benefits in this chart. I know a few state pensioners who would be horrified if you suggested that they were on benefits")

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards