We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is a perfectly balanced portfolio possible? What would it look like? How would it perform?

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

[Deleted User]

Posts: 0 Newbie

For the sake of this thought experiment I’ll just include liquid assets that you could buy/sell from your computer on a Wednesday afternoon - (so no rare books or Star Wars action figures).

I imagine you’d want to include share tracker funds from every country where they are available, corporate and government bonds, and commodities, and probably a lot of other more exotic investments that I’ve never heard of.

If you were able to get this perfectly balanced how would it perform? Would it move at all (the gains in one area cancelling losses in another)?

I’m asking because I’m wondering what people really mean when they say a balanced portfolio, they say it as if there is some set threshold at which a portfolio goes from being unbalanced to balanced.

I imagine you’d want to include share tracker funds from every country where they are available, corporate and government bonds, and commodities, and probably a lot of other more exotic investments that I’ve never heard of.

If you were able to get this perfectly balanced how would it perform? Would it move at all (the gains in one area cancelling losses in another)?

I’m asking because I’m wondering what people really mean when they say a balanced portfolio, they say it as if there is some set threshold at which a portfolio goes from being unbalanced to balanced.

0

Comments

-

You can't get a 'perfectly balanced' portfolio, because compromises always need to be made when executing a theoretical plan. To devise a balanced portfolio, you need to start with your objectives, circumstances and risk tolerance, then work forward from there towards the most efficient (highest expected return for lowest level of risk) collection of assets that meet your needs. What is right for you won't be right for everyone else.

3 -

The Nobel man William Sharpe has proposed a global representative portfolio of stocks and bonds weighted by how much money is in the stock and bonds markets I think, as a way of optimising a risk adjusted return. You can read about here, including how it might have performed. https://www.bogleheads.org/forum/viewtopic.php?t=3003871

-

If you were able to get this perfectly balanced how would it perform?Impossible to get it perfectly balanced as it requires opinions to decide what is perfect.Would it move at all (the gains in one area cancelling losses in another)?No, that isn't how it works.I’m asking because I’m wondering what people really mean when they say a balanced portfolio, they say it as if there is some set threshold at which a portfolio goes from being unbalanced to balanced.Balanced means a spread of assets across the areas with what would be considered a reasonable allocation to each.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

‘ When I use a word... it means just what I choose it to mean, no more no less’. Alice was told.1

-

1

-

Now that's a really interesting little problem, but also leads to the question of what a perfectly balanced portfolio means to you.Here's how I'd tackle it:First, define your objective: (a) minimise portfolio variance, (b) maximise returns, (c) maximise sharpe ratio, (d), minimise tail risk, ....

Next, what are the constraints: (a) long only, (b) long and short, (c) minimum and maximum percentages for each (or group) of assets. Now this can be solved numerically to give you the optimal portfolio weights as per objective. Mind you that's optimising history, so repeat that process over the sampling period whereby you re-calculate new weights for the next quarter or year. Using these weights get the performance history over time. I'd run it both ways: first zero fees and then with some fee assumptions to see how practical it is. My fear is, unless you restrict to say 10 assets and rebalance not that often, transaction costs will drown everything.

Then benchmark it against passive alternatives.

The biggest challenge would be to get all candidate assets and their time series together. There you want all bases covered: across asset classes and regions. Bit of programming, but should be solvable in principle. If you start off with a handful of asset all from one source, solving these weights is easy, the rebalancing is just iterating the whole spiel, getting time series together would be a challenge ...

1 -

What metric are we using to balance things, cap weighted? How do we balance bonds, stocks, commodities etc? The closest thing might be a global multi-asset fund.“So we beat on, boats against the current, borne back ceaselessly into the past.”0

-

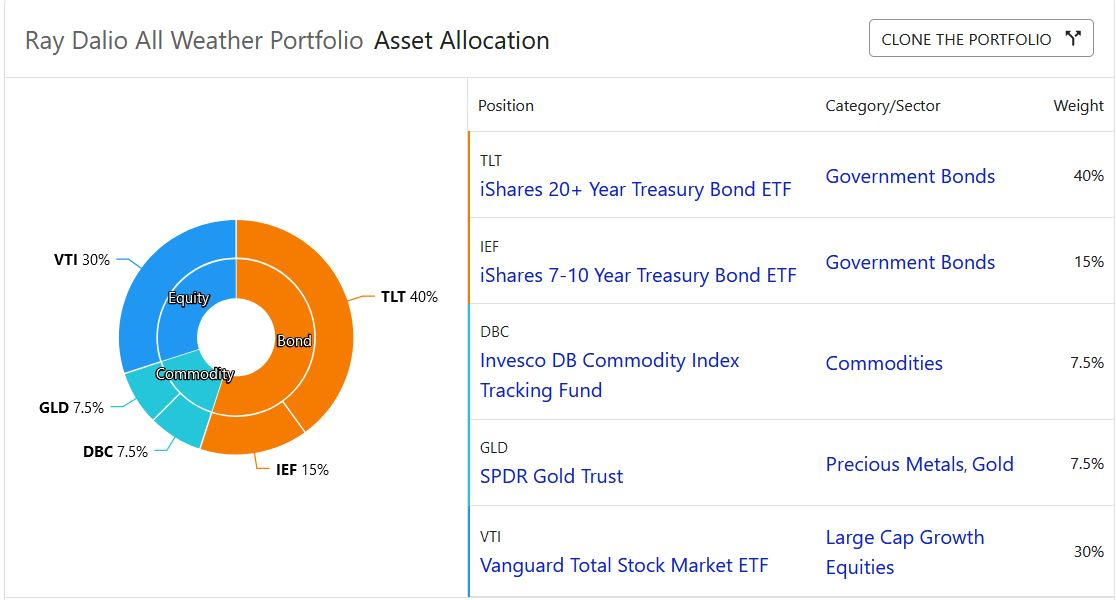

Nothing is perfect.But one quite close to that is proposed by one of the well know hedge fund Ray Dalio. It is called "all whether portfolio". With such portfolio it will be less volatile, less risky, less intervention is needed but you are sacrificing the potential return. The return is more likely to be lower than the market, the S&P500.

Here is how the so called "balanced portfolio", "all whether portfolio" is performing against the market S&P500

Here is how the so called "balanced portfolio", "all whether portfolio" is performing against the market S&P500 Volatility has a correlation with the reward (e.g return). The less volatile your portfolio is (e.g balance port folio, all weather port folio) the less reward you will likely to get. It is represented by a ratio called "Treynor Ratio"Another one is the ratio of the return of your investment vs the risk you are willing to take which is already mentioned above formulated by William F. Sharpe called "Sharpe Ratio"Unless you are lucky, the "Balanced portfolio", "All whether portfolio"are less volatile, less risky than S&P500 (say) but are more likely to produce a lower return.2

Volatility has a correlation with the reward (e.g return). The less volatile your portfolio is (e.g balance port folio, all weather port folio) the less reward you will likely to get. It is represented by a ratio called "Treynor Ratio"Another one is the ratio of the return of your investment vs the risk you are willing to take which is already mentioned above formulated by William F. Sharpe called "Sharpe Ratio"Unless you are lucky, the "Balanced portfolio", "All whether portfolio"are less volatile, less risky than S&P500 (say) but are more likely to produce a lower return.2 -

For the record do you know what the Five and Ten Year comparisons are?

Although the fact the S&P 500 did so well over those periods may not give a very good forward indication.1 -

Albermarle said:For the record do you know what the Five and Ten Year comparisons are?

Although the fact the S&P 500 did so well over those periods may not give a very good forward indication.

Very good point. In fact I'd go back to pre-2000 as well to capture that bull market with its subsequent crash. (Note on the side, reducing drawdowns has a big impact, in fact, one can afford a relatively low beta if the losses are rigorously limited, yielding an incredible risk/reward or sharpe ratio.)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards