We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The big fat Electric Vehicle bashing thread.

Comments

-

There's nothing wrong with my figures. You can simply ignore the repayments and equity values and it adds up to the same total; I was just (very reasonably) demonstrating that the car wasn't suddenly worth zero and that I was building equity by overpaying on the mortgage. Just because something is unconventional doesn't make it wrong.Grumpy_chap said:

You trott this out regularly with very unconventional take on accounting practices when you try to explain the detail...Petriix said:

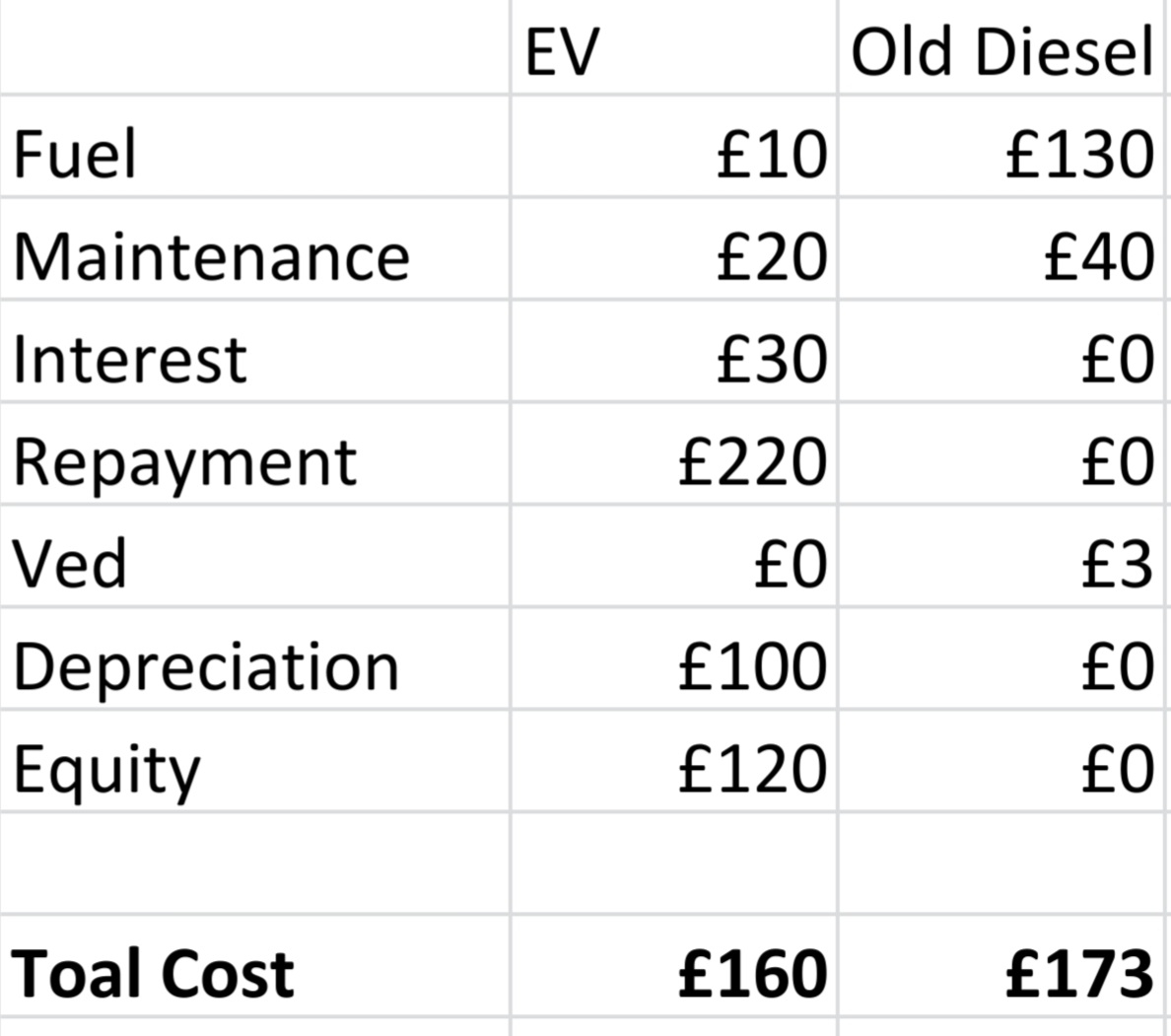

I've found it quite the opposite. Running a brand new EV has saved me thousands vs keeping my old diesel car on the road.Deleted_User said:Electric cars are still priced out of reach for most ordinary folk who buy used cars outright and run them for a good few years until they fancy something newer or they need replacing.Petriix said:I made a simple spreadsheet to demonstrate how paying more each month can save you money...

That depreciation figure is the key variable. It's highly unpredictable and represents the element of risk with my approach. Obviously fuel costs may change too. But I demonstrably have more money by switching from a 16 year old (fairly economical) diesel to a brand new EV; albeit some of that is locked in the equity in the car.

In reality it's actually better than those figures. Maintenance on the EV has been just £33 in 16 months and depreciation has been zero. The old diesel needed £800 of work to keep on the road. I owe £17,500 on the mortgage (having paid off £2,500 and paid £3k towards the EV from savings) so would be £5,500 in credit if I sold it today.

So, with capital outlay equaling equity, I can currently ignore those costs. I could stop paying the mortgage for the next year without penalty due to the overpayment reserve. While I'm happy to risk the value of that equity dropping, for comparison I only need to look at the running costs and interest.

The old diesel would have cost ~ £2,600 to cover the same 14k miles. The EV has cost ~ £600. That's a £2,000 contribution towards the current equity and potential future depreciation. But, if I sold it today, I'd have that £2k as profit.

But, it gets even better... The next 14k miles would cost more like £3k in the diesel while it will still be around £600 in the EV. With inflation at such a high level, money already paid for an asset effectively appreciates in value. The best deal on a new MG5 is around £4k more than I paid. The money I owe is devaluing faster than the interest rate I fixed at.

It's not rocket surgery. I know it's counterintuitive and not without risk, but sometimes spending money saves you more.ontheroad1970 said:How do you get paid that equity each month? - by that I mean, cold hard cash in your pocket?Cross_Man said:

I don't want to entirely discount the potential that buying a new EV (or even a new ICE) could work in such a way that there could be a "pay-back". I had a similar consideration once when I was driving a 2.5 litre petrol-guzzling Mondeo that was starting to accrue maintenance costs. I did compare the option to a C4 diesel that was on an attractive offer and in theory the fuel savings would have eventually paid for the car.

However, that calculation seems entirely flawed. Which lines are + costs and which lines are - savings to reach the £160?

The scenario is not right in the idea of "buying equity" every month.

You start with £25k equity (cash) and exchange that for £25k equity (car) on day 1.

After 1 month you pay £30 interest and £220 capital repayment (£250 total). You also have reduced equity as the car is no longer worth £25k.

Repeat each subsequent month.

In an extreme scenario, the car could be an appreciating asset in which case you'd have an "equity" value but no "depreciation" value - it is simply not possible to have an individual item showing depreciation and accumulation in the same period.

Anyway, it is entirely irrelevant for the OP who is likely frustrated by the de-railing of their thread. They have a perfectly good Fiesta (paid for) that will last them for many years and provide low-cost motoring. It is possible the OP could make a reduction in operating costs by swapping to an early Leaf, but they may well not feel that they have been "upgraded" in their car if they make that change. Whatever operating cost reduction might be possible, the OP will need to set that against the extra capital required to achieve that and, for the mileage profile in consideration, that is likely to be quite a long time even if the increase in purchase price was from the current £5k Fiesta to a £7k Leaf.

Proposals and consideration to a new £25k MG5 or any equivalent car would only be relevant if the OP was considering against a brand new car but that does not seem to be the OP's suggestion.

The fact is that the amount of money leaving my bank account has been roughly comparable to what it would have been to keep my 16 year old diesel car on the road. I paid £3k from savings, but this is entirely retained in equity in the car - I currently owe £17k against a value of > £22k.1 -

The figures in the spreadsheet don't even add up. No such thing as equity only depreciation. Fuel costs and VED will be less with electric car though dependent on charging at home. Depreciation greater for electric car although appreciate market distorted at the moment. Probably not much difference in total. Main reason to change would be 'going green'. Secondary effects are interesting though. If I bought an electric car I couldn't do the European driving that I am used to. Rail fares are horrendous. I would probably just fly more. Would that be good?2

-

Because the average driver has almost no journeys long enough to not use the EV. They can use it for the rest of the journeys.Thrugelmir said:

If the EV isn't used for the longer journeys. Then why tie up capital in what is ultimately a wasting asset. I'd say that many people commute far longer distances by car than they did even a few decades ago. There's a far better road network now.Herzlos said:I don't mean travelling over 100 miles without stopping is extreme, just that for most people it's not really an issue as they can have a coffee/lunch/explore or whatever.

I do get that EVs may not be suited to a once a year trek across the country and back (although many EV owners don't find it a problem), but I'm not sure it's that big a deal to that many people given the inconvenience is twice a year. It's also worth noting that many households have multiple cars, so many people have the option of using the other ICE car for the holiday road trip.

As for freedom, people can already live and visit where they want; they just tend to want to live close to work and shop close to home and so on.

I'm not convinced anyone can get 12p/mile out of an ICE car now. 50mpg at £1.50/l is 14p/mile

Lots of people with 2 cars; one EV and one ICE tend to find they rarely use the ICE so the ICE become the useless asset.2 -

Be a bit more imaginative. You can charge places that aren't motorway services, so break road trips up by stopping at nice places whilst you charge.DB1904 said:

Explore a motorway services. Are you serious?Herzlos said:I don't mean travelling over 100 miles without stopping is extreme, just that for most people it's not really an issue as they can have a coffee/lunch/explore or whatever.

I do get that EVs may not be suited to a once a year trek across the country and back (although many EV owners don't find it a problem), but I'm not sure it's that big a deal to that many people given the inconvenience is twice a year. It's also worth noting that many households have multiple cars, so many people have the option of using the other ICE car for the holiday road trip.

As for freedom, people can already live and visit where they want; they just tend to want to live close to work and shop close to home and so on.

I'm not convinced anyone can get 12p/mile out of an ICE car now. 50mpg at £1.50/l is 14p/mile

After 2 hours sat in a car then a short walk around a lake or beach or whatever will do everyone good. We usually do that when traveling with the kids anyway.2 -

No-one has ever said that the car is suddenly worth zero.Petriix said:

There's nothing wrong with my figures. You can simply ignore the repayments and equity values and it adds up to the same total; I was just (very reasonably) demonstrating that the car wasn't suddenly worth zero and that I was building equity by overpaying on the mortgage. Just because something is unconventional doesn't make it wrong.Grumpy_chap said:

You trott this out regularly with very unconventional take on accounting practices when you try to explain the detail...Petriix said:

I've found it quite the opposite. Running a brand new EV has saved me thousands vs keeping my old diesel car on the road.Deleted_User said:Electric cars are still priced out of reach for most ordinary folk who buy used cars outright and run them for a good few years until they fancy something newer or they need replacing.Petriix said:I made a simple spreadsheet to demonstrate how paying more each month can save you money...

That depreciation figure is the key variable. It's highly unpredictable and represents the element of risk with my approach. Obviously fuel costs may change too. But I demonstrably have more money by switching from a 16 year old (fairly economical) diesel to a brand new EV; albeit some of that is locked in the equity in the car.

In reality it's actually better than those figures. Maintenance on the EV has been just £33 in 16 months and depreciation has been zero. The old diesel needed £800 of work to keep on the road. I owe £17,500 on the mortgage (having paid off £2,500 and paid £3k towards the EV from savings) so would be £5,500 in credit if I sold it today.

So, with capital outlay equaling equity, I can currently ignore those costs. I could stop paying the mortgage for the next year without penalty due to the overpayment reserve. While I'm happy to risk the value of that equity dropping, for comparison I only need to look at the running costs and interest.

The old diesel would have cost ~ £2,600 to cover the same 14k miles. The EV has cost ~ £600. That's a £2,000 contribution towards the current equity and potential future depreciation. But, if I sold it today, I'd have that £2k as profit.

But, it gets even better... The next 14k miles would cost more like £3k in the diesel while it will still be around £600 in the EV. With inflation at such a high level, money already paid for an asset effectively appreciates in value. The best deal on a new MG5 is around £4k more than I paid. The money I owe is devaluing faster than the interest rate I fixed at.

It's not rocket surgery. I know it's counterintuitive and not without risk, but sometimes spending money saves you more.ontheroad1970 said:How do you get paid that equity each month? - by that I mean, cold hard cash in your pocket?Cross_Man said:

I don't want to entirely discount the potential that buying a new EV (or even a new ICE) could work in such a way that there could be a "pay-back". I had a similar consideration once when I was driving a 2.5 litre petrol-guzzling Mondeo that was starting to accrue maintenance costs. I did compare the option to a C4 diesel that was on an attractive offer and in theory the fuel savings would have eventually paid for the car.

However, that calculation seems entirely flawed. Which lines are + costs and which lines are - savings to reach the £160?

The scenario is not right in the idea of "buying equity" every month.

You start with £25k equity (cash) and exchange that for £25k equity (car) on day 1.

After 1 month you pay £30 interest and £220 capital repayment (£250 total). You also have reduced equity as the car is no longer worth £25k.

Repeat each subsequent month.

In an extreme scenario, the car could be an appreciating asset in which case you'd have an "equity" value but no "depreciation" value - it is simply not possible to have an individual item showing depreciation and accumulation in the same period.

Anyway, it is entirely irrelevant for the OP who is likely frustrated by the de-railing of their thread. They have a perfectly good Fiesta (paid for) that will last them for many years and provide low-cost motoring. It is possible the OP could make a reduction in operating costs by swapping to an early Leaf, but they may well not feel that they have been "upgraded" in their car if they make that change. Whatever operating cost reduction might be possible, the OP will need to set that against the extra capital required to achieve that and, for the mileage profile in consideration, that is likely to be quite a long time even if the increase in purchase price was from the current £5k Fiesta to a £7k Leaf.

Proposals and consideration to a new £25k MG5 or any equivalent car would only be relevant if the OP was considering against a brand new car but that does not seem to be the OP's suggestion.

The fact is that the amount of money leaving my bank account has been roughly comparable to what it would have been to keep my 16 year old diesel car on the road. I paid £3k from savings, but this is entirely retained in equity in the car - I currently owe £17k against a value of > £22k.

Financing a car on a mortgage is widely held as not the most cost-effective mechanism, but individual circumstances can exist where, with discipline, that works.

Your presentation of the figures is certainly unconventional. That may not make it wrong, but no-one else on this thread or the other one was able to understand the figures and @Ibrahim5 has repeated what others have said - the figures do not add up and there cannot be equity appreciation and depreciation for the same asset in the same time period.

It does not promote the conversion to greater EV penetration by using figures that are (or appear) spurious. I believe you are pro-EV, so can you clarify the spreadsheet so it is more clearly understandable?

IMO, trying to compare a new EV versus end-of-life ICE is the incorrect analysis as a starting point. The appropriate cost comparison would be new EV versus new ICE.1 -

When EVs become more dominant and traditional fuel petrol and diesel stations diminish in number, does anyone think road tax will remain at zero for an EV, and there won't be an electric vehicle fuel tax?

Maybe the transport system will change to "pay per mile" and hit every road user evenly. Either way, the "savings" of EV ownership are going to shrink as the purchase cost reduces and battery technology improves to make ownership more realistic.I’m a Forum Ambassador and I support the Forum Team on the In My Home MoneySaving, Energy and Techie Stuff boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.

1 -

I agree that EV taxes will start in some format - but do you really think that petrol/diesel costs/taxes won't increase by even more? The government will be looking to remove all of the last ICEs from the roads, fewer petrol stations and reduced demand will push up fuel prices. At the moment they're offering the carrot on taxation, once the momentum shifts they'll apply the stick.victor2 said:When EVs become more dominant and traditional fuel petrol and diesel stations diminish in number, does anyone think road tax will remain at zero for an EV, and there won't be an electric vehicle fuel tax?

Maybe the transport system will change to "pay per mile" and hit every road user evenly. Either way, the "savings" of EV ownership are going to shrink as the purchase cost reduces and battery technology improves to make ownership more realistic.

When EV ownership becomes the norm, then it will be all about where you charge, energy tariffs etc. I can charge for free via solar at home, or 50-60p/kWh on public chargers. Still lots of opportunities to reduce running costs, there will be much greater variation in costs than between current forecourt prices.

The next 3 years are going to be a good opportunity for some people to save a lot of money running an EV. Mine will cost me £360 for the next year - I don't have to pay personally for insurance, 'fuel', breakdown cover, maintenance etc. Even after these 3 years (2025 onwards BIK rates aren't published yet) it's going to be cheaper than an equivalent ICE.3 -

Speaking of figures that don't add up (well I suppose technically as you haven't provided any numbers there is no way they could) it might help if you provided figures rather than unsubstantiated statements with no such as "Depreciation greater for electric car"Ibrahim5 said:The figures in the spreadsheet don't even add up. No such thing as equity only depreciation. Fuel costs and VED will be less with electric car though dependent on charging at home. Depreciation greater for electric car although appreciate market distorted at the moment. Probably not much difference in total. Main reason to change would be 'going green'. Secondary effects are interesting though. If I bought an electric car I couldn't do the European driving that I am used to. Rail fares are horrendous. I would probably just fly more. Would that be good?

How did you calculate that depreciation for electric cars is greater than petrol cars? Is this all cars, new cars, second hand cars?

Regarding which is more polluting - running an electric car for the vast majority of your journeys and taking a small number of flights versus a petrol car for all journeys will depend on how many flights you take/miles you drive.

1 -

How the heck will pay per mile work for tax? they going to stick a black box in every car then send a bill every month for the miles you've travelled? Sick of hearing folk bleet on about it but never say how it will work.0

-

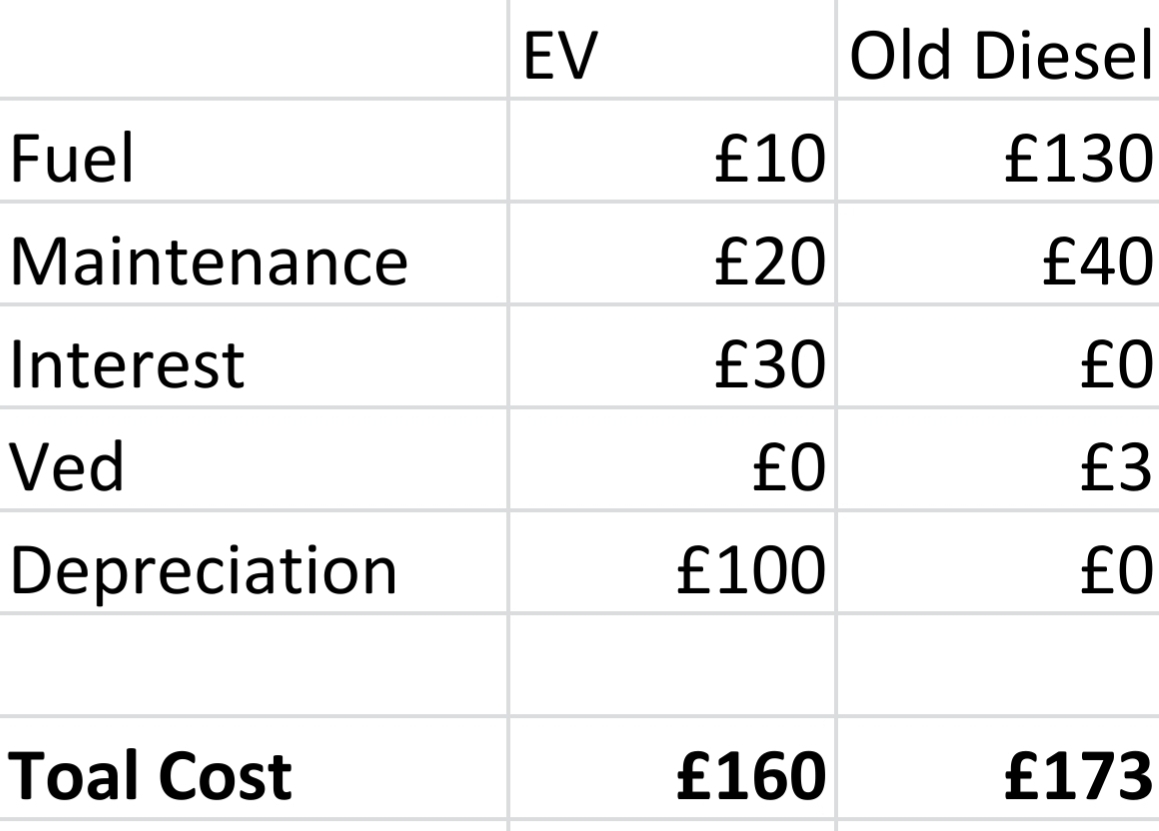

The numbers do add up - only the depreciation is a cost; the repayment of £220 minus the increased equity equals the depreciation. The equity figure is real and important to account for, otherwise you're assuming that the car is worth nothing. Here's the same figures without the offending 'equity':Ibrahim5 said:The figures in the spreadsheet don't even add up. No such thing as equity only depreciation. Fuel costs and VED will be less with electric car though dependent on charging at home. Depreciation greater for electric car although appreciate market distorted at the moment. Probably not much difference in total. Main reason to change would be 'going green'. Secondary effects are interesting though. If I bought an electric car I couldn't do the European driving that I am used to. Rail fares are horrendous. I would probably just fly more. Would that be good?

I've paid out about £6700 in total (including mortgage overpayments), but now owe £17k against a > £22k car. That £5k in equity would be in my pocket (or a deposit on whatever car I replace it with) if I sold it today. So the actual total cost of ownership has been ~ £1700 for 16 months and 14k miles.

The equivalent cost of running the old diesel would have been at least £3k - about £2k in fuel, £800 just to scrape through the MOT in 2020 then a couple of years of VED, a couple of oil changes, another MOT in 2021. So that's objectively at least £1300 saved.

Now there's currently only 1 MG5 on Autotrader for under £23k so that £5k equity is pretty conservative. It's more like £6k or more, but it's reasonable to assume that prices will settle in the long term. However, with inflation so high, it's not unreasonable to believe that second hand prices might remain fairly constant while new prices continue to escalate.

The only real costs I've had are ~ £400 in interest, £160 for electricity and a £33 service. Everything else I've paid is retained in the value of the car.

But it gets better still. Because I have an EV I was able to switch to Octopus Go in January and fix at 5p off peak, 24p peak, 24p per day standing charge. I've shifted half my home usage to the off peak window so I'm averaging ~ 15p per kWh for my home usage, plus the lower standing charge. That's saving me over £250 vs being stuck on the price cap.

That's a total cost of £350, a saving of over £2500, for the pleasure of upgrading a 16 year old banger to a brand new EV.

Now I'm fully aware that depreciation might accelerate. But it's got a long way to go just to cover that £2500 before it's actually cost me anything. And the savings vs diesel will keep increasing too.

I look forward to some further irrational dispute with my figures.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards