We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Stamp Duty on re-mortgaged 2nd house?

Comments

-

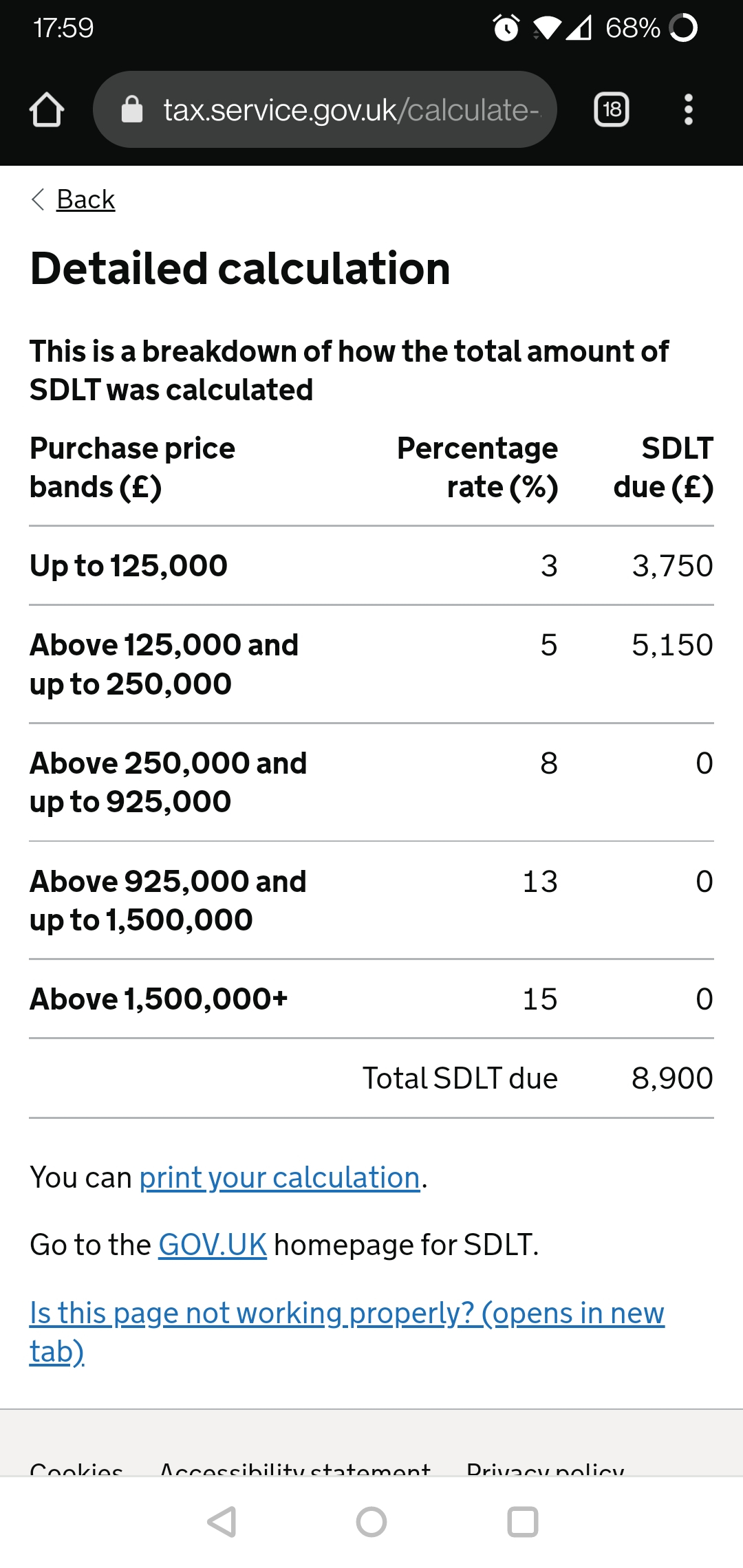

Here is the calculation.

1 -

And just to double/triple check before I call my solicitor an idiot, the additional 3% is still applicable even tho its a BTL mortgage on the 2nd property?SDLT_Geek said:

£2,060 is the correct amount on £228K without the 3% extra. 3% of £228K is another £6,840. Adding that to £2,060 gives £8,900 which is the amount of SDLT you should pay.warwick2001 said:

The solicitor has quoted £2,060 for the Stamp Duty. Please could you show how you got to £8,900, thanksSDLT_Geek said:

The SDLT on House A with the extra 3% on a price of £228K comes to £8,900. Is that what the solicitor said?warwick2001 said:

We are paying £228k for House ASDLT_Geek said:

I would expect you to pay SDLT only on the property you are buying, House A, but with the extra 3% for additional properties. If you say what the price is, I could work out the SDLT to see if it matches what your solicitor says.warwick2001 said:Afternoon all,

Just got a question for you knowledgeable folk.

We are in the process of buying a house for us to live in (£182k mortgage). House A

Our current house is being remortgaged with a BTL mortgage (£85k BLT mortgage). House B

We have just received our completion certificate from our solicitor, and there appears to be only 1 stamp duty payment, and it appears to be attached to House A.

I have read that "Stamp Duty Land Tax is not payable unless there is a need to transfer the legal title of your home as part of the remortgage transaction". And technically this is the case, we are not changing the legal title. However, I am positive I should be paying 2 lots of stamp duty on the purchase/re-mortgage as we will have 2 houses, House A is our home, House B will be rented out.

Can anyone advise please.

Many thanks

I would not expect you to have to pay SDLT on the remortgage of House B, unless its underlying ownership is also changing.0 -

The extra 3% is due because you will own two properties when you buy House A. You do not qualify as "replacing" your residence as you are keeping House B, not selling it.warwick2001 said:

And just to double/triple check before I call my solicitor an idiot, the additional 3% is still applicable even tho its a BTL mortgage on the 2nd property?SDLT_Geek said:

£2,060 is the correct amount on £228K without the 3% extra. 3% of £228K is another £6,840. Adding that to £2,060 gives £8,900 which is the amount of SDLT you should pay.warwick2001 said:

The solicitor has quoted £2,060 for the Stamp Duty. Please could you show how you got to £8,900, thanksSDLT_Geek said:

The SDLT on House A with the extra 3% on a price of £228K comes to £8,900. Is that what the solicitor said?warwick2001 said:

We are paying £228k for House ASDLT_Geek said:

I would expect you to pay SDLT only on the property you are buying, House A, but with the extra 3% for additional properties. If you say what the price is, I could work out the SDLT to see if it matches what your solicitor says.warwick2001 said:Afternoon all,

Just got a question for you knowledgeable folk.

We are in the process of buying a house for us to live in (£182k mortgage). House A

Our current house is being remortgaged with a BTL mortgage (£85k BLT mortgage). House B

We have just received our completion certificate from our solicitor, and there appears to be only 1 stamp duty payment, and it appears to be attached to House A.

I have read that "Stamp Duty Land Tax is not payable unless there is a need to transfer the legal title of your home as part of the remortgage transaction". And technically this is the case, we are not changing the legal title. However, I am positive I should be paying 2 lots of stamp duty on the purchase/re-mortgage as we will have 2 houses, House A is our home, House B will be rented out.

Can anyone advise please.

Many thanks

I would not expect you to have to pay SDLT on the remortgage of House B, unless its underlying ownership is also changing.

You can refer your solicitor to the guidance on it starting from this contents page: https://www.gov.uk/hmrc-internal-manuals/stamp-duty-land-tax-manual/sdltm097301 -

If you are swapping your main residence for your main residence my understanding is you do not need to pay the 3% stamp duty ?0

-

Just to clarify my understanding is you would’ve already paid the 3% on the cheaper house as it’s a buy to let0

-

Your understanding is incorrect. 'Replacing' in SDLT terms means selling the previous main residence.SuseOrm said:If you are swapping your main residence for your main residence my understanding is you do not need to pay the 3% stamp duty ?

The extra SDLT due is for 'additional properties'. The OP will own one property before the transaction and two afterwards hence the additional 3% SDLT.1 -

Well if it was me I would somehow orchestrate it so that you pay the 3% stamp duty on the cheaper house first and then go ahead with the purchase of house A which therefore is replacing the main residence0

-

You pay stamp duty if applicable on your first house.. Then when you buy another house, if you do not sell the other house you are changed normal stamp duty plus the additional 3%or4%.SuseOrm said:Just to clarify my understanding is you would’ve already paid the 3% on the cheaper house as it’s a buy to let

It doesn't matter that is BTL or not. If you have one property and you buy another thus having 2 houses, the additional tax is due.0 -

https://www.capextax.com/news/what-is-the-definition-of-main-residence-for-stamp-duty-land-taxSnookie12cat said:

You pay stamp duty if applicable on your first house.. Then when you buy another house, if you do not sell the other house you are changed normal stamp duty plus the additional 3%or4%.SuseOrm said:Just to clarify my understanding is you would’ve already paid the 3% on the cheaper house as it’s a buy to let

It doesn't matter that is BTL or not. If you have one property and you buy another thus having 2 houses, the additional tax is due.That doesnt seem to always be the case.0 -

Well if that was possible it would be fantastic. But it isn't...SuseOrm said:Well if it was me I would somehow orchestrate it so that you pay the 3% stamp duty on the cheaper house first and then go ahead with the purchase of house A which therefore is replacing the main residence

I'm not sure how you're interpreting that website but it confirms what the rest of us are saying...SuseOrm said:

https://www.capextax.com/news/what-is-the-definition-of-main-residence-for-stamp-duty-land-taxThat doesnt seem to always be the case.3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards