We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Ns&i Green Bonds

Comments

-

Minimum investment is £100. Open as as many as you as you wish.InvesterJones said:Another thought: it is sometimes possible to buy more than one bond, in which case you could start one this tax year and start another the next (ie in two months time) - that way the maturities fall across two tax years so you'll get the advantage of another years PSA.0 -

The new tax year is only 7 weeks away

0 -

Oh?InvesterJones said:Another thought: it is sometimes possible to buy more than one bond, in which case you could start one this tax year and start another the next (ie in two months time) - that way the maturities fall across two tax years so you'll get the advantage of another years PSA.

ok so if I was to buy half the bonds now - then the other half in two months time - I wouldn’t get hit with anywhere near as much tax?0 -

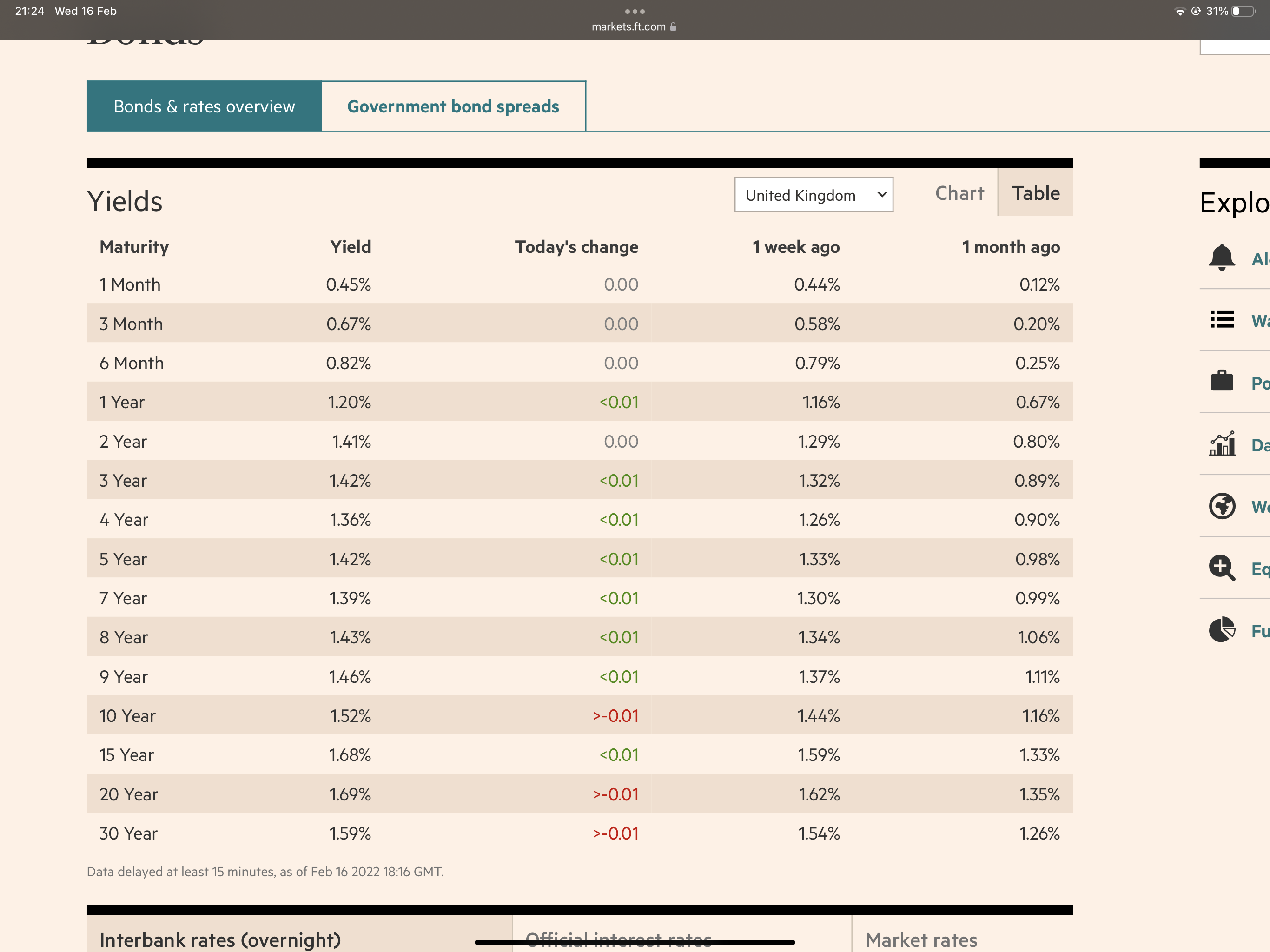

You'll need a stockbroker but the annual yield to maturity of the benchmark gilt maturing in three years' time is presently 1.41%.

0 -

The redemption yield is your return on the investment. The running yield is what you pay tax on. Currently, most gilts will be above par, which means that the running yield will be more than the redemption yield. The market spreads are also wide if you trade in small amounts via the LSE. Do your homework before investing in anything.wmb194 said:You'll need a stockbroker but the annual yield to maturity of the benchmark gilt maturing in three years' time is presently 1.41%.0 -

Yes, I wanted to keep it simple and just give an easy comparison but it certainly explains why NS&I/the Treasury decided to up the rate on these 'green' bonds to 1.3%.GeoffTF said:

The redemption yield is your return on the investment. The running yield is what you pay tax on. Currently, most gilts will be above par, which means that the running yield will be more than the redemption yield. The market spreads are also wide if you trade in small amounts via the LSE. Do your homework before investing in anything.wmb194 said:You'll need a stockbroker but the annual yield to maturity of the benchmark gilt maturing in three years' time is presently 1.41%.If you look at TR25 5% Treasury Stock 07/03/25 the current indicated offer is £111 and my calculator tells me, ex broker fees, that this gives a YTM of 1.309%... A running yield of 4.5% paid twice a year, you can sell them whenever you like and whilst you'll take a loss at redemption it'll be on future pounds which will be worth less. If I felt a strong compulsion to lend to the government at a lousy rate I think this they way I'd do it. They trade on ORB so there should be no issue trading in small clips and this has certainly been my experience in the past with other issues.

https://www.londonstockexchange.com/stock/TR25/united-kingdom/company-page2 -

ranciduk said:

Oh?InvesterJones said:Another thought: it is sometimes possible to buy more than one bond, in which case you could start one this tax year and start another the next (ie in two months time) - that way the maturities fall across two tax years so you'll get the advantage of another years PSA.

ok so if I was to buy half the bonds now - then the other half in two months time - I wouldn’t get hit with anywhere near as much tax?

Precisely. If it earned £1500 interest in one tax year and £1500 in the next then your PSA of 1000 would apply separately to each, resulting in 20% tax on only £1000 in total rather than £2000.

1 -

Nice one!InvesterJones said:ranciduk said:

Oh?InvesterJones said:Another thought: it is sometimes possible to buy more than one bond, in which case you could start one this tax year and start another the next (ie in two months time) - that way the maturities fall across two tax years so you'll get the advantage of another years PSA.

ok so if I was to buy half the bonds now - then the other half in two months time - I wouldn’t get hit with anywhere near as much tax?

Precisely. If it earned £1500 interest in one tax year and £1500 in the next then your PSA of 1000 would apply separately to each, resulting in 20% tax on only £1000 in total rather than £2000.

Thanks for that0 -

Can someone clear up for me?

do you have to buy all the bonds in one lump?

or is it ok to by them in individual chunks - over a few weeks?

0 -

Impossible to find information about that on their website. As it is a fixed term account, you probably can only make one single deposit but the terms and conditions (which are incredibly difficult to find) are not conclusive. I suggest you ring them if you want to find out.ranciduk said:Can someone clear up for me?

do you have to buy all the bonds in one lump?

or is it ok to by them in individual chunks - over a few weeks?

I find this account truly awful in every sense. The information about it on the NS&I website is unclear, and the interest rate is anything but competitive. I can't help the suspicion that they are trying to exploit the good intentions of people who want to see environmentally friendly investments.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards