We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

The Top Fixed Interest Savings Discussion Area

Comments

-

I don't think you're correct. In order to take advantage of the 0% starting rate I reckon that your total income, excluding savings income, but not ISA income, must be below £12750.Bigwheels1111 said:Steve_xx said:

I think, that to be able to take advantage of the 5% starting rate, that your income (from work and/or pensions) needs to be below £12570.Harryo said:

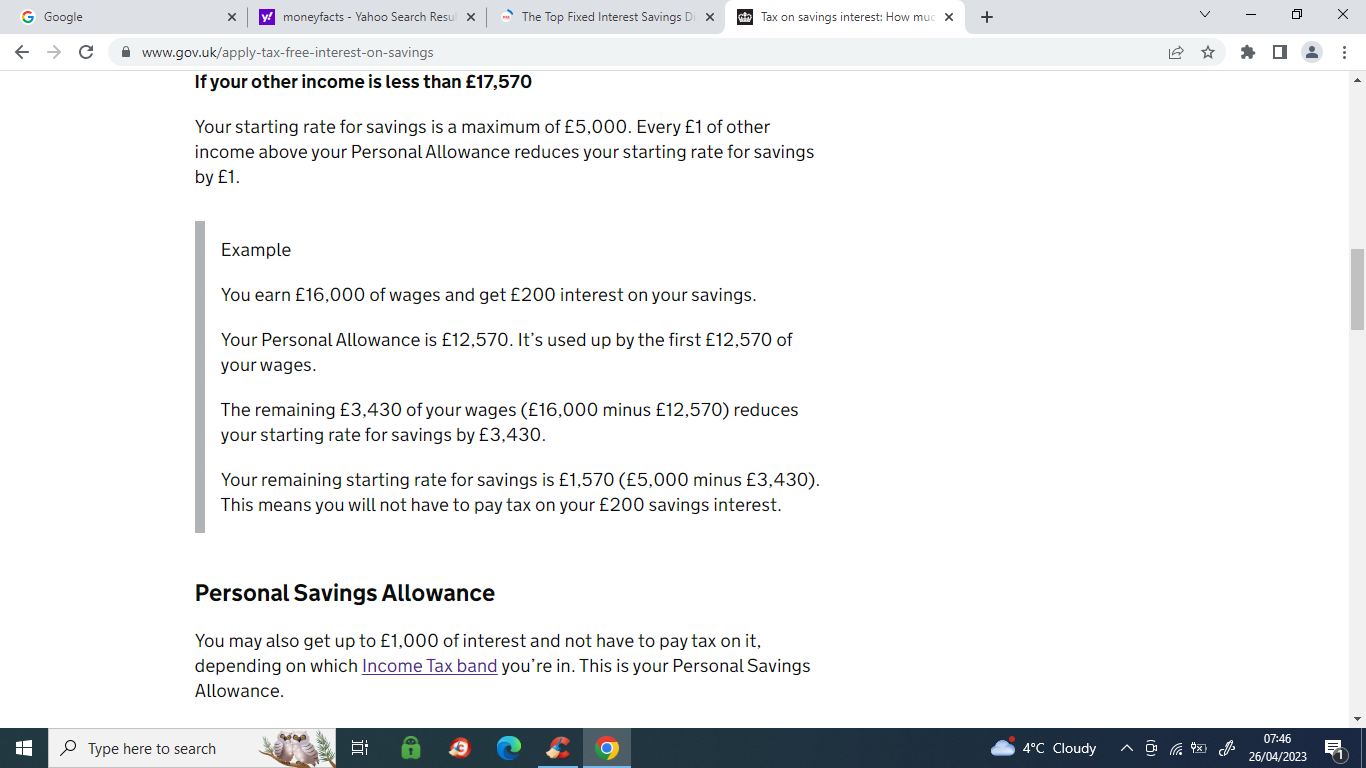

And also how much income you have. If it is between £12750 and £17500 then you can earn up to £5000 interest tax free at best from the additional Starting Savings Rate. If it is below £12750 then you can make use of your normal Personal Allowance.Steve_xx said:Well yes, that's worth considering I guess. So then, if you put 21k into the 4.75% account, that would just about use up your £1000 personal allowance. It depends how much money you have saved.The way I read it is that if you earn say £14k it deducts £1,430 from the starter rate leaving £3,570.

I could be wrong.

0 -

The way I read it if other income is not more than £12570 basic rate tax payer can get savings interest of £6000 tax free

Starting rate for savings

You may also get up to £5,000 of interest and not have to pay tax on it. This is your starting rate for savings.

Personal Savings Allowance

You may also get up to £1,000 of interest and not have to pay tax on it, depending on which Income Tax band you’re in. This is your Personal Savings Allowance.

0

0 -

Yes. I'm reading it the same as you do. But on reflection I think Bigwheels1111 comments are in fact correct. The nice space for the operation of the 0% band is where income from work/pensions is falling at or below £12570. The upper limit for applying the 0% Savings band looks to be £17570. So for every £1 earned over £12570 you lose £1 of the £5000 0% Savings Rate.bristolleedsfan said:The way I read it if other income is not more than £12570 basic rate tax payer can get savings interest of £6000 tax freeStarting rate for savings

You may also get up to £5,000 of interest and not have to pay tax on it. This is your starting rate for savings.

Personal Savings Allowance

You may also get up to £1,000 of interest and not have to pay tax on it, depending on which Income Tax band you’re in. This is your Personal Savings Allowance.

5 -

One piece of the jigsaw is missing for me and that is NS&I. They have been given a directive to attract more inward investment. Just wish they would get their finger out and get on with it.

I do wonder if they have received a large inflow of cash due to the recent banking issues going on in America and Europe.

1 -

This is so unusual that I had to check, and it's right:VNX said:Just for information you can only have one savings bond with Smartsave I had looked at having a one and a two year but was told can only have one

"Can I have more than one savings account?Our customers can only have one SmartSave savings account at a time."

Your questions answered with our FAQs - SmartSave (smartsavebank.co.uk)

Very odd, and could be quite aggravating (I opened a 3 year one with them last year, so there's no point in me thinking about another account with them for 2 years). I think it could be important enough for MSE to put it as a caveat when they list them in their best-paying accounts (currently, SmartSave are top for 1, 2 and 3 year accounts). Anyone know the best way of bringing an MSE staff member's attention to it?

5 -

"Anyone know the best way of bringing an MSE staff member's attention to it?"

Normally, social media. Twitter??0 -

We couldn't get any raisin accounts to approve, so ended up with Atom 5 Year at 4.65

We will have some more available for fixing for shorter periods soon so these numbers are looking interesting.

I'd like to see NS&I up their rates as well. Because they can offer a higher guarantee amount it would work well for us for some of our larger amounts and mean we don't have to keep lots of accounts on the go.1 -

I'm twiddling my thumbs before committing anything fixed (have only ever used easy access/regular savers until now) and hoping that the NS&I guaranteed income bonds increase to the better side of 4%0

-

I opened a one year fixed rate bond last November. Its slightly nerve racking locking money away for the first time.PloughmansLunch said:I'm twiddling my thumbs before committing anything fixed (have only ever used easy access/regular savers until now) and hoping that the NS&I guaranteed income bonds increase to the better side of 4%

If you open an oxbury one year fixed rate at 4.54% with 1k, which is the minimum. You can open an existing customer one year bond at 4.75%.

3 -

Thanks for this just to clarify if you open a one year bond with the one k minimum you then have access to the existing customer bonus rates?jimexbox said:

I opened a one year fixed rate bond last November. Its slightly nerve racking locking money away for the first time.PloughmansLunch said:I'm twiddling my thumbs before committing anything fixed (have only ever used easy access/regular savers until now) and hoping that the NS&I guaranteed income bonds increase to the better side of 4%

If you open an oxbury one year fixed rate at 4.54% with 1k, which is the minimum. You can open an existing customer one year bond at 4.75%.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards