We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Getting FIREd up 😀

Comments

-

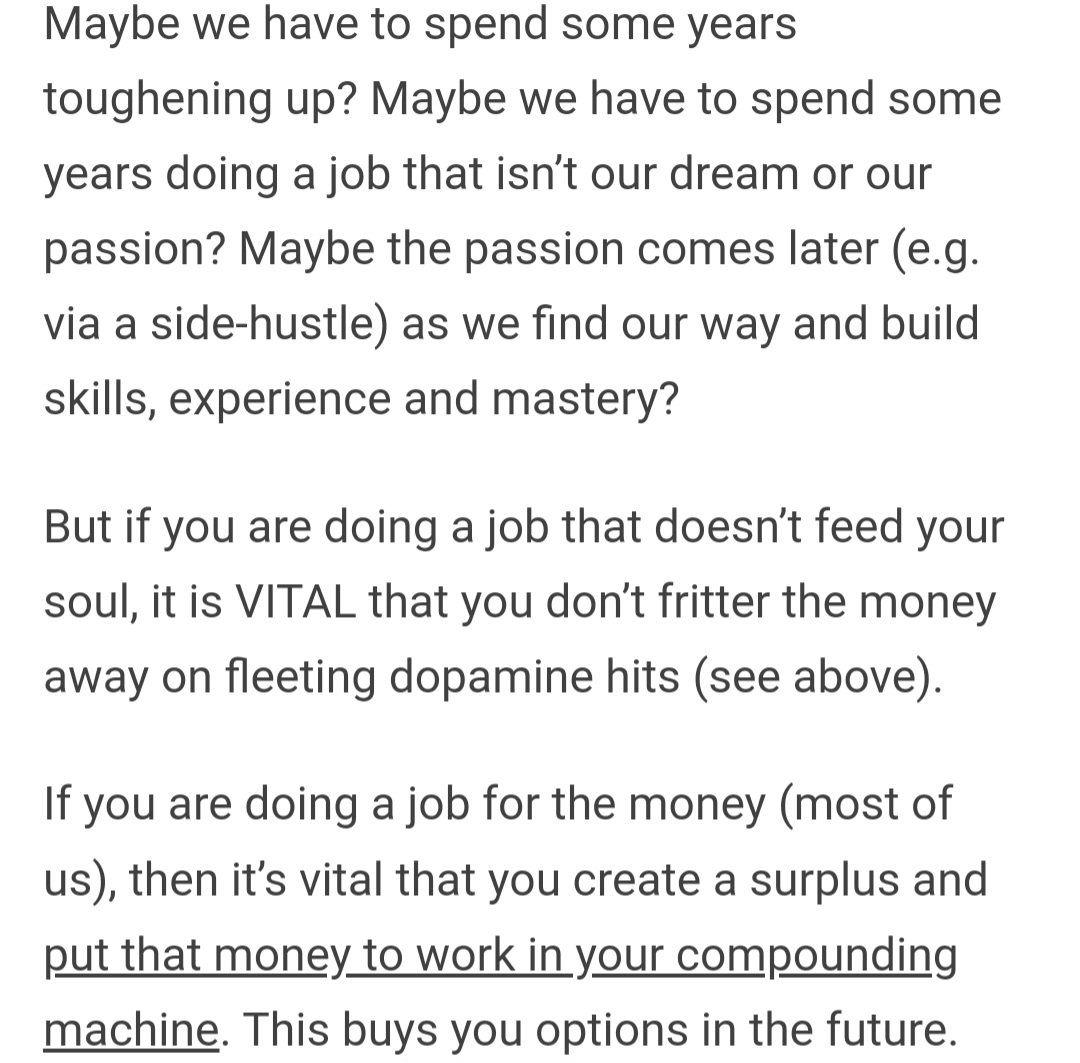

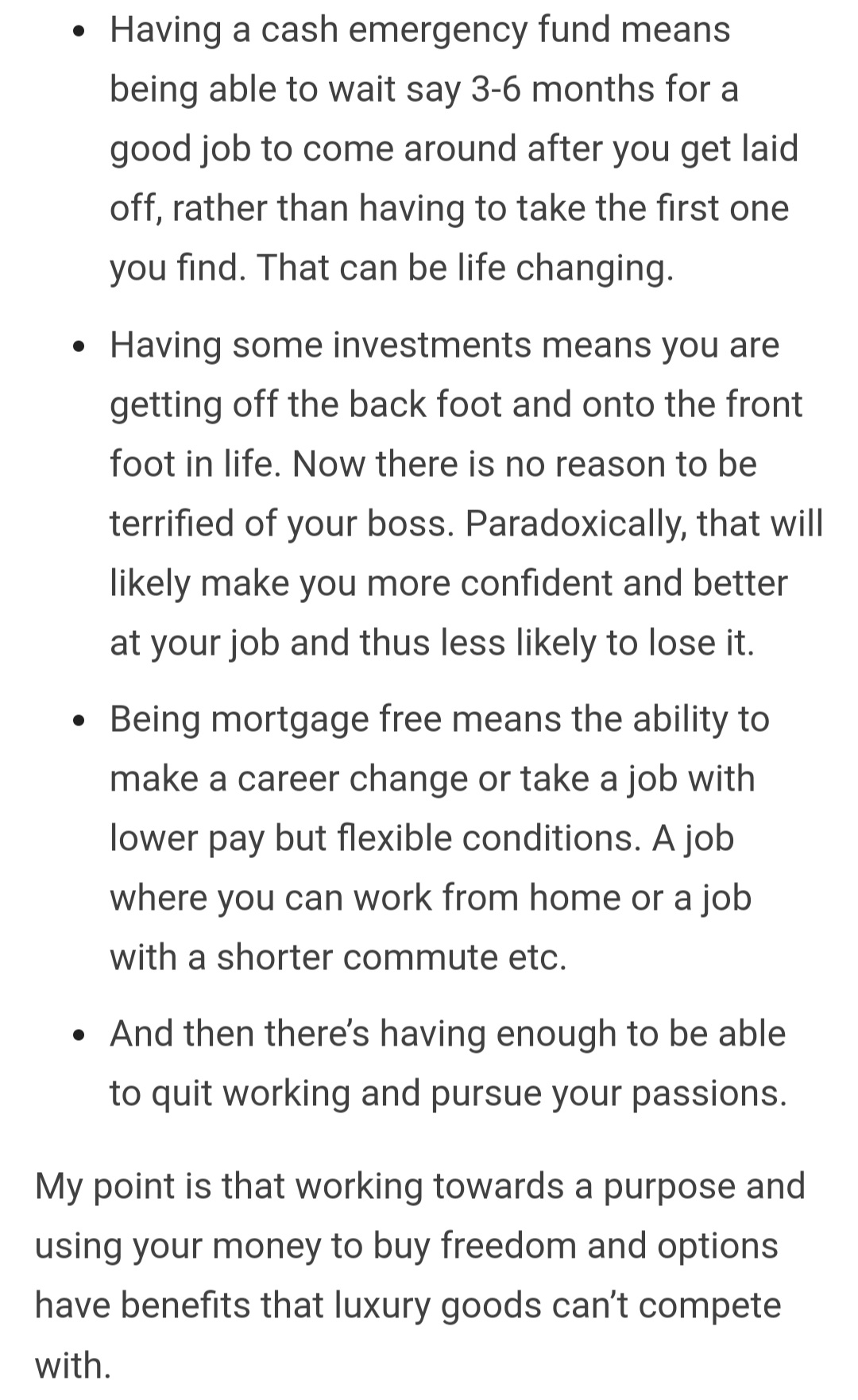

Just read this by The Escape Artist. An excellent reminder of what we can actually "afford" to do once we take control of our money 😀:

Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!9 -

Great piece and really resonates3

-

Definitely agree with that and it's nice to see it written down to make you really think.I've been mortgage free once, so let's do it again!

Starting balance March 26 £191,274.533 -

An excellent reminder that we need to be mindful in what we're doing and why we're doing it!Start mortgage date: August 2022; Start mortgage amount: £240,999; Original mortgage free date: August 2056

Current mortgage amount: £224,460.73

Start student loan 2012: £29,750; current student loan: CLEARED July 2025

Unread owned books Jan 2026: 256

Undone crafts 2026: +12 -

I should not do hard maths at this time of night 😅!Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!1 -

At the risk of being contrary, I don't think that spending on hits of dopamine is a bad thing as long as they are measured and don't damage your long term goals.

For example, I can't ever imagine calling my job a passion. I play with spreadsheets all day, fun sometimes, mentally stimulating almost always, satisfying often but my passion? Nah. I spend money to pursue my interests outside work, it's budgeted and it makes life good. It doesn't stop me from pursuing my financial goals.

Buying random food however... I really need to stop that.3 -

Not contrary at all KP, it's discussion that we're here for 👍! It's the focus on the long-term goals that sets you apart in this situation, I think. What the article was getting at (there was a lot more that I didn't post, as it was quite lengthy), was that if you are spending money on things to make you feel better about life, without first having set yourself up on a solid financial footing, things are never going to change long-term and you'll only get fleeting satisfaction from your spending, but live with a constant low-level angst.

What makes you different (and the rest of us here), is that you have done that financial groundwork and have a long-term plan underway. In which case (although it wasn't stated explicitly), I think we are safe to do a little happy spending 😀Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!3 -

First of the month round-up….

15x extra £50s this month, coming from bank account cashback, TopCashBack, surveys, interest, some tilly tidies, another energy rebate and a chunky amount leftover from the holiday pot (none being planned at present so I can focus on the refurb 😥, so wanted to put it to good use). Used them towards the big bill pot - which is now complete 🥳🥳🥳!!!

Realised I am at the point of getting taxed on my savings interest, so I've cleared almost the whole balance from my stooze cards (I'll chuck a load into an ISA when the new year starts in April, but that's a long time away 😬) Probably cutting off my nose to spite my face, as obvs the tax man wouldn't take all the money, but I just can't be bothered with the paperwork. I did toy with putting some in premium bonds until April, but I like having it all with the same provider….and I just can't be bothered with the paperwork

Conversely, have taken out a new 0% card with a £15k limit (£15k 😳!), which will be used to buy materials for the refurb so that I can focus the cash on paying for labour and get the work done without necessarily having every penny already in the bank. I now have £33k available across 6 cards though, which is a bit bonkers. I'll be closing at least 2, probably 3, but that is on the Christmas holidays life admin list, as no mad rush to get it done

Have been upset all month about Panelbase switching to Norstatpanel. The surveys are fine, but earning vouchers is irksome and the redemption process is cumbersome. I liked earning cash!

Spent £10 getting a new photo taken for my driving licence, to discover on returning home and actually reading the renewal letter I'd been sent 6 weeks earlier that they will ONLY use the photo from your passport 🙄 Thought I would at least have had a choice (not entirely sure how that works - passport is 2 years old so it still looks like me, but if it were 9 years old, the driving licence photo could be 19 years old by the time it expires 🤔🤷♀️?)

Realised that powering on through the last week's worth of a Lidl night cream that I thought I'd trial but haven't been getting on with really wasn't necessary in value for money/getting my money's worth terms, as the whole jar had only cost me £1.49 😅

Dramatically reduced the annual mileage on my car insurance (more on that another day) in the hope of a tasty refund, but insurance costs have gone up so much recently that it only worked out as £8.84, despite still having 4 months to run on the policy. Oh well, better in my hands than theirs I suppose, and at least the renewal quote will come out with the correct details 🤷♀️!

The £8.84 went onto the Sainsbury's Bank card that I stopped using when I started stoozing, so I've pressed that back into service again, as even I can't see the logic in continuing to stooze whilst at the same time fretting that I have “too much” (from stoozing!) in savings. It's nowhere near as pretty-looking as the Barclaycard was though - sad times 😥🤣

11.38 years to go….

The stock market appears to have had something of a rally - both of the larger pensions were up by a bit over £1k each (about 4%), as was the smaller one (about a 7% increase in that one, once you deduct the new money added). KP was right, November was a better month 🤣!

Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!5 -

I must have timed it right as my passport and driving license are due to run out in the same year so the photo thing won't be such an issue I hope. Shame you spent the money on new photos but you never know when they might come in handy - I needed one for an international driving permit the other month. Sounds like the renovation plans might happen next year if you're prepping with the credit card? I'm really not looking forward to insurance renewals next year so well done on at least getting something back.Emergency Fund - £8572.39 / £10,000 :: Mortgage OP 2025 - £LISA 24/25 - £3200 / £4000 :: NSD 2025 - 2 / 150 :: Books Read: 1 / 52 :: Decluttering - 4 / 1000Engaged 9th December 2010 :: Married 29th October 2015 :: Bought a House 13th January 20172

-

That's a lot of extra £50s SC, well done!

I'm absolutely with you on avoiding tax on savings interest. I do a tax return anyway, but avoiding the savings interest does simplify the process a little. If in future you have a considerable amount on hand do give premium bonds a second thought, could make you a millionaire, but even if not will still likely give you a few more extra £50s tax free along the way 🙂

It's possible you were charged an admin fee for updating insurance mid contract, so the saving on a full year could be more substantial.

The stock market bounce this month really was something wasn't it!? 🤑3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards