We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Timing the market

Comments

-

Maybe I've not been looking in the right places but I have struggled to find any good data to show that quality (as we understand it in modern times) underperforms the market over the longer term?

Data mining is great but who really cares about the past? The problem for every single factor is that outperformance tends to disappear once the factor is “discovered”. The added problem for “quality” is that everyone defines it differently.

0 -

"Would be interesting to see the correlation of large cap growth and quality over the last decade."BritishInvestor said:

it would be useful to strip out the last decade (not just 5 years) to see how quality has performed. Would be interesting to see the correlation of large cap growth and quality over the last decade.Alexland said:BritishInvestor said:"If the performance is identical why not use Fundsmith and avoid the effort"

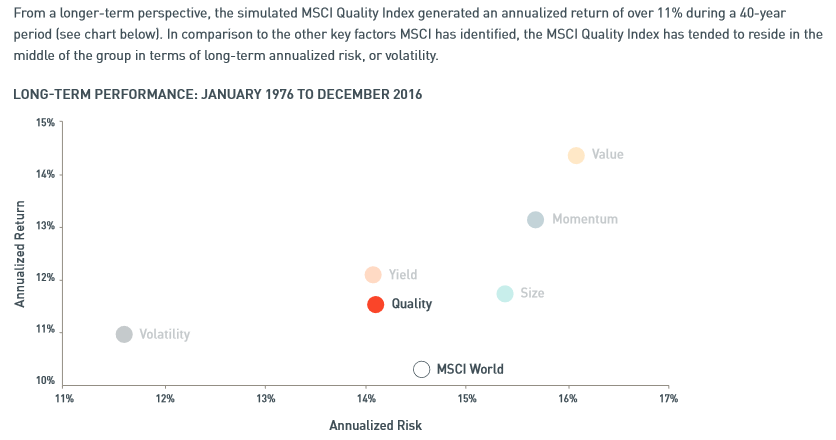

I think we might be arguing two different things. My main point is that it's unlikely you will fund genuine outperformance in the retail space. As to whether you should buy a certain fund or not, that's a different question, but I can't really think of a retirement objective that would be best fulfilled by strategies that history shows underperform over the longer term.Maybe I've not been looking in the right places but I have struggled to find any good data to show that quality (as we understand it in modern times) underperforms the market over the longer term? It's easy to find plenty of data that shows value doing better but with higher volatility.For example, the below 5 year old image (to remove some recent quality overperformance) from the MSCI factor factsheet using data going back the previous 40 years suggests that quality has provided a higher return with lower volatility than going passive with a world index. Of course with Fundsmith that extra 1% return goes back to Terry with his high OCF and it's hard to stick with any factor investment in periods when it's totally out of favour and many tend to close down or get merged into something else with better short/medium term prospects so holding a world index might be an easier ownership path.

Re fundsmith, I'm thinking more of the large-cap growth style.

0.961 -

The signs were there. Borrowing in SF against revenues and assets in Turkish Lira. Exchange rate losses taken through balance sheet not P&L.Thrugelmir said:

Polly Peck collapsed due to a well hidden and complex fraud. Dented confidence in the the value of what at face value appeared to be healthy annual audited accounts. As a consequence the Cadbury Report recommended fundamental changes to Corporate Governance for UK listed companies. The code has changed over the years but the cornerstones of practice have remained in place. A reason that the London stock markets are so well regarded globally.MarkCarnage said:Source and application of funds statement is a key page in a company's annual accounts. Far more difficult to hide transgressions thereAgreed. Queens Moat and Polly Peck were but two where a quick perusal of these would have had significant alarm bells ringing.....years before they actually went bust.

Non Exec director appointed then resigns suddenly 2 months later (presumably when he finds out what is going on). Among others. Nadir was a persuasive and charismatic individual. I met him. He wasn't a bully like Maxwell.0 -

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

1 -

jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.

0 -

I would suggest that some of those very rich people are there because they took us mortals along with them. Poor fund managers are not typically very rich.BritishInvestor said:jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.0 -

I think we're talking about three distinct groups of people.Prism said:

I would suggest that some of those very rich people are there because they took us mortals along with them. Poor fund managers are not typically very rich.BritishInvestor said:jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.

1.Someone that could predict factor performance - net worth TBD (if such a person/firm exists)

2.Hedge funds

https://en.wikipedia.org/wiki/Jim_Simons_(mathematician)

As reported by Bloomberg Billionaires Index, Simons' net worth is estimated to be $25.2 billion, making him the 66th-richest person in the world

3. Active fund managers

https://en.wikipedia.org/wiki/Terry_Smith_(businessman)

The Sunday Times Rich List has estimated his wealth to be £300 million.

0 -

Yet funds which do consistently outperform exist and have existed repeatedly for long enough to exploit this.BritishInvestor said:jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.

There's a class that matters: those who are good at fund management in whatever team they are in and whatever part of the market who can do quite well out of that particular skill set but maybe not so well individually.

While looking at factors may determine some or even all of how they did or do manage their work, that still leaves them with the higher performance.0 -

"Yet funds which do consistently outperform exist and have existed repeatedly for long enough to exploit this."jamesd said:

Yet funds which do consistently outperform exist and have existed repeatedly for long enough to exploit this.BritishInvestor said:jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.

There's a class that matters: those who are good at fund management in whatever team they are in and whatever part of the market who can do quite well out of that particular skill set but maybe not so well individually.

While looking at factors may determine some or even all of how they did or do manage their work, that still leaves them with the higher performance.

If you are able to continually identify genuine outperformers ahead of time you have a rare and valuable skill. Professionals running Discretionary Fund Management (DFM) offerings struggle to do this. To be fair this might be because they don't want all their eggs in one style basket which is working now (but might not work in the future).

1 -

I'm not sure how rare that ability to pick a decent active fund ahead of time is. I think its fairly clear that the average investor does underperform to some degree but those (rare) stats include all of the investors who try and assess individual stocks to hold alongside or instead of funds and all of those investors who simply use the default fund in their pension or platform.BritishInvestor said:

"Yet funds which do consistently outperform exist and have existed repeatedly for long enough to exploit this."jamesd said:

Yet funds which do consistently outperform exist and have existed repeatedly for long enough to exploit this.BritishInvestor said:jamesd said:

You proceeded to use hindsight to determine that it would have been possible to match the results using a range of factors, without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight. Anyone can match or beat a past market by knowing what worked."Regrettably, your view does not seem logical, for it's deciding in advance, not with hindsight, that is the challenge. Someone has to make the decisions about which factors, weightings or whatever to use, before the future unfolds."

That's what I said - maybe I didn't make myself clear enough.

It'll normally be the case that with hindsight past performance can be matched, but hindsight isn't available when making the decisions. If choosing active, you're choosing a person and team based on their ability to do this (and often, rejecting lots of others based on their demonstrated lack of such ability, which greatly narrows the range of candidates).

"without giving any apparent weight to the difficulty of picking those factors without the benefit of hindsight."

I think I've given plenty of weight when I said anyone that is able to do this consistently would be one of the richest people in the world. And they'd be unlikely to be giving away any of their profits/secret sauce to us mere mortals.

There's a class that matters: those who are good at fund management in whatever team they are in and whatever part of the market who can do quite well out of that particular skill set but maybe not so well individually.

While looking at factors may determine some or even all of how they did or do manage their work, that still leaves them with the higher performance.

If you are able to continually identify genuine outperformers ahead of time you have a rare and valuable skill. Professionals running Discretionary Fund Management (DFM) offerings struggle to do this. To be fair this might be because they don't want all their eggs in one style basket which is working now (but might not work in the future).

I honestly know of no research that has ever asked the question of how well does an active investor do when they try and pick a fund that will perform well in the future. The other unknown is that does that strategy increase or reduce some form of risk - thats a very personal trait. So all 'evidence' for and against is anecdotal - hence these types of debate.

Just to bring back in the original topic, some people say that timing the market is very possible and they have done very well from it.0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards