We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Which stocks & shares ISA

Comments

-

Being invested for the long term is not so much about improving returns but more about about being able to see-through/outlast any market downturns to still come out ahead. To illustrate: at some point over the next ten years, it is perfectly feasible that the market will drop by 30% and then take 3 years to recover that amount. It is also perfectly feasible that after dropping 30% it will increase at 9% per year for the next 7 years.PJD said:So looking at this, I can see why you should invest for at least 5 years to ensure the biggest returns, however, most years it raises far beyond a normal cash ISA anyway, - so why is it so important to keep the money in there for so long?

Looking at the history of all of the other Vanguard Lifestratety products, they've all gone up most years well above the best cash ISA

You do not want to be a 'forced withdrawer' during that crash period; you want to be able to see it through and onto the new highs. The costs of achieving equity returns is equity volatility. the market has an upward trajectory, but you need to be able to suffer the highs and lows on the way..1 -

The dates you've looked at give quite a flattering picture. If you'd looked in April 2020 then you'd have a -25% (or something similar) number for the last year. It does very much depend on the time period and when you are looking so if you'd needed access to the money in April last year you'd have taken much more of a hit than if you'd waited until nowPJD said:In regards to the duration; looking at the history of Vanguard 80% Equity Fund for example (appreciate history is no indication of future),

last year: + 24%

2019: - 3%

2018: + 8%

2017: + 5%

2016: + 23%

So looking at this, I can see why you should invest for at least 5 years to ensure the biggest returns, however, most years it raises far beyond a normal cash ISA anyway, - so why is it so important to keep the money in there for so long?

Looking at the history of all of the other Vanguard Lifestratety products, they've all gone up most years well above the best cash ISARemember the saying: if it looks too good to be true it almost certainly is.2 -

Many thanks.

Should I be mindful that Vanguard is an American company, - would it be wise to keep investments in the UK?

I am considering various options, however, if I was to invest say £20k into a S&S ISA, I have read that it's best to split it, rather than transfer the entire amount, - how would you break it down - £3k a month or something?

0 -

The parent company is an American corporation but the Vanguard Investor platform is a UK operation and the LifeStrategy (and other) investments are offered by their UK fund manager. The underlying investments are global (which is the whole point of using multi-asset funds like that), so it's not clear what you really mean by 'keeping investments in the UK'?PJD said:Should I be mindful that Vanguard is an American company, - would it be wise to keep investments in the UK?

Contrary to what you've read, it generally makes financial sense to invest a lump sum at the earliest opportunity rather than drip-feeding it in, as the expectation when investing will naturally be that there will be more up days than down days, so, on average, delaying is likely to miss out on growth. Having said that, many newbie investors find it more comforting psychologically to get into the water gradually....PJD said:I am considering various options, however, if I was to invest say £20k into a S&S ISA, I have read that it's best to split it, rather than transfer the entire amount, - how would you break it down - £3k a month or something?2 -

Should I be mindful that Vanguard is an American company, - would it be wise to keep investments in the UK?

You are not buying shares in Vanguard. Vanguard are providing an administration service.

And investing 100% into UK assets would be poor quality investing. You would be using a UK regulated firm though.

It sounds like you need to do some more reading and research to bring your knowledge level up a bit.

am considering various options, however, if I was to invest say £20k into a S&S ISA, I have read that it's best to split it, rather than transfer the entire amountWhat have you read that suggests its best to split it? Statistically, that results in a worse outcome in most periods. So, why did whatever you read say that? (what was their reason for the scenario they were talking about?)

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Sorry - the American company concern was a comment from my Dad on the phone this morning!I have read on quite a few places about drip feeding investments into shares, the reason to ride out any potentials bumps in the market (and psychologically - in case the market suddenly drops). What you both say makes a lot of sense however. Thanks for your patience, you've all been hugely helpful here, I really appreciate it.0

-

I have read on quite a few places about drip feeding investments into shares, the reason to ride out any potentials bumps in the market (and psychologically - in case the market suddenly drops). What you both say makes a lot of sense however. Thanks for your patience, you've all been hugely helpful here, I really appreciate it.

Phasing can give the impression of reducing volatility. However, if you are nervous about that volatility, to begin with then perhaps you are investing above your risk level? (not necessarily you but the people thinking of phasing).

What happens when you stop phasing it in? Well, you are fully invested and subject to the same volatility that you would have been had you invested fully from the start. Phasing is just delaying the inevitable. So, better to get it right from the start.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

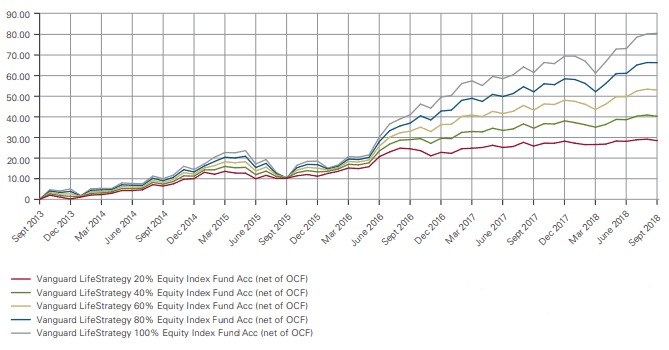

Just choosing which one to go for, am I reading this chart, below, incorrectly? It suggests that the highest risk (100% equity) never bottomed out any more than any of the others?

https://www.muchmorewithless.co.uk/wp-content/uploads/2018/12/18-12-13-Vanguard-LifeStrategy-performance.png

(Taken from here: https://www.muchmorewithless.co.uk/which-vanguard-lifestrategy-fund/)

If so - it seems silly to invest in anything other than the 100% equity?

0 -

VLS 100 dropped more in March 2020 than VLS 80, which was more than VLS 60 and so on.PJD said:Just choosing which one to go for, am I reading this chart, below, incorrectly? It suggests that the highest risk (100% equity) never bottomed out any more than any of the others?

https://www.muchmorewithless.co.uk/wp-content/uploads/2018/12/18-12-13-Vanguard-LifeStrategy-performance.png

(Taken from here: https://www.muchmorewithless.co.uk/which-vanguard-lifestrategy-fund/)

If so - it seems silly to invest in anything other than the 100% equity?

Unsurprisingly the 100% equity fund will drop more when equities drop in value.

That chart you linked to only looks at if you invested in September 2013, and as has been highlighted this has been a good period for investors.

You can easily compare past performance of the VLS funds over other time periods. e.g. charts below [VLS 100 (orange) and VLS 40 (blue), both Acc] starts in May 18 or November 2019 where you can see VLS 100 dropping more than 40.

1

1 -

The VLS range only has a short history. It didn't exist during the credit crunch or the dot.com (and other events) periods. It has existed only during a significant growth period that is unlike most periods in the history of investing. The US underperformed most countries/regions in the previous cycle but it has driven returns in the cycle VLS existed. So, any fund or portfolio that has been heavy in US in that period has done well and that has masked a lot of issues.PJD said:Just choosing which one to go for, am I reading this chart, below, incorrectly? It suggests that the highest risk (100% equity) never bottomed out any more than any of the others?

https://www.muchmorewithless.co.uk/wp-content/uploads/2018/12/18-12-13-Vanguard-LifeStrategy-performance.png

(Taken from here: https://www.muchmorewithless.co.uk/which-vanguard-lifestrategy-fund/)

If so - it seems silly to invest in anything other than the 100% equity?

It is rare for the best performing area/country in one cycle to be the best in the next. Often the one that is amongst the worst jumps to being up the top and vice versa.

So, be wary of looking at the last decade VLS has been available and think that is the norm. Look at the decades before that to get an idea of the real volatility that can and will occur at times.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards