We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

SWR Question

Comments

-

Wow! More than I've read, but good work putting those drawdown resources together.

0 -

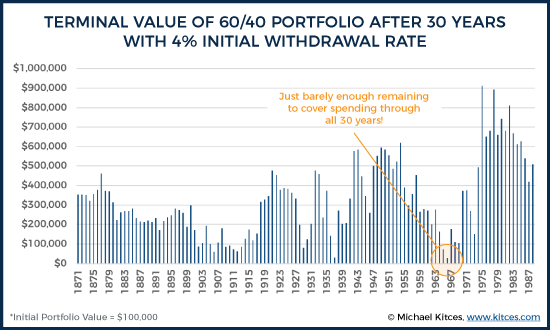

Over that period US moved from an emerging economy to the dominant economic powerhouse of the world. Scenario which is pretty rare. People do use SWR for periods far exceeding 30 years; nor do those retiring at 65 know how long they would need it. Still, 150 years is very short, in statistical terms, when compared to 30. On top of that, fiat money we currently use have existed for a MUCH shorter period. And the fiscal and monetary systems are undergoing rapid and fundamental changes over the last 10 years. We have no idea if any of the preceding history of the stockmarket is relevant to the future.Linton said:

Also the figures are based on the performance of US investments over the past 150 years and are believed to be lower for UK investors, particularly those who invest in the UK which as been the majority for most of that time. On the other hand the past 150 years include 2 world wars, several technological revolutions, the rise and fall of empires and major economic powers etc etc which may or may not be relevent to the next 50 years.JohnWinder said:Yes, it's worth reading more fully on this, as one would discover that 'safe' means the method fails in only 5% of circumstances based on history. That wouldn't be safe enough for me, but you only have drop to about 3.7% instead of 4% withdrawal to be 99% certain of never running out. And if one kept reading one discovers it's not designed for 50 years of withdrawal, but 30.

So all in all I think SWR figures may be useful for a sanity check but cannot provide any sort of guaranteed basis for one's entire retirement. Certainly anyone who says that their plan has a x% chance of future success is fooling themselves.3 -

Agree on all points. To illustrate how short a period 150 years is, in the past 150 years more than 2/3 of all 40 year periods include at least one world war.Deleted_User said:

Over that period US moved from an emerging economy to the dominant economic powerhouse of the world. Scenario which is pretty rare. People do use SWR for periods far exceeding 30 years; nor do those retiring at 65 know how long they would need it. Still, 150 years is very short, in statistical terms, when compared to 30. On top of that, fiat money we currently use have existed for a MUCH shorter period. And the fiscal and monetary systems are undergoing rapid and fundamental changes over the last 10 years. We have no idea if any of the preceding history of the stockmarket is relevant to the future.Linton said:

Also the figures are based on the performance of US investments over the past 150 years and are believed to be lower for UK investors, particularly those who invest in the UK which as been the majority for most of that time. On the other hand the past 150 years include 2 world wars, several technological revolutions, the rise and fall of empires and major economic powers etc etc which may or may not be relevent to the next 50 years.JohnWinder said:Yes, it's worth reading more fully on this, as one would discover that 'safe' means the method fails in only 5% of circumstances based on history. That wouldn't be safe enough for me, but you only have drop to about 3.7% instead of 4% withdrawal to be 99% certain of never running out. And if one kept reading one discovers it's not designed for 50 years of withdrawal, but 30.

So all in all I think SWR figures may be useful for a sanity check but cannot provide any sort of guaranteed basis for one's entire retirement. Certainly anyone who says that their plan has a x% chance of future success is fooling themselves.3 -

The US moved from an emerging economy to an economic powerhouse and the UK from a global empire to an ordinary developed country. So the SWRs appear safe against radically different economic progressions.

No reason not to use an SWR for more than thirty years, just calculate one for the desired term. Thirty is long enough that 35 or 40 is close enough to work if people follow the usual pattern of spending declining over time.0 -

To a certain extent the "cash pot" scenario is similar to the Overpay Mortgage or Invest (in Pension) questions we get on here.

Mathematically and rationally investing will provide a better return at some point in the future if the future broadly pans out like the past so don't pay mortgage off or keep a multi-year cash buffer.

Paying the mortgage off / having a cash buffer is a more emotional response and lets you sleep easier in the here and now.3 -

Lets arbitrarily assume that the future will be very much like the recent past. A 1 in 20 probability of running out of money and dying in abject poverty does not make me think “safe”. If you live for 40 or 50 years after retirement that probability goes up quite a bit. The constant should really be called UWR.jamesd said:The US moved from an emerging economy to an economic powerhouse and the UK from a global empire to an ordinary developed country. So the SWRs appear safe against radically different economic progressions.

No reason not to use an SWR for more than thirty years, just calculate one for the desired term. Thirty is long enough that 35 or 40 is close enough to work if people follow the usual pattern of spending declining over time.Alternatively, you could account for the fact that you are invested in a highly variable market and improve your chances in a meaningful manner by not planning for a constant rate of withdrawal.0 -

Good points with some important implications....jamesd said:

.........ac198179 said:Assume a 4% SWR, I thought that each year you took out 4% of your pot (plus adjustment each year for inflation, but let's ignore inflation just for now). But is it actually that each you take out 4% of your starting balance at retirement? E.g. say I retire at 57 with a pot of £100k, 4% of which is of course £4k - is that how much I withdraw on each of the following years, or do I withdraw 4% of the new balance each year? So, assuming no growth at all between year 0 and year 1, do I then withdraw 4% of £96k?

But be aware:

1. That is for a US investor using a fifty fifty mixture of equities and government bonds2. Adding substantial small cap weight increased it to 4.5%

3. The UK equivalent to 4% is 3.7% using UK investments4. It's for a thirty year plan, you need to start lower for say forty years5. It ignores costs. Deduct one third of costs to allow for them6. It's for 100% success within the analysis period. If you're willing to adapt if you live through bad times you can use 99%, 90% or 75% or even 50% success rate to get a higher starting level. Something like fifty percent success might work for a person with all core needs covered by guaranteed income who's flexible about this part.

1) Most people on this forum seem to be thinking of a higher % equity than 50%. With a 50/50 portfolio, if you can manage both halves separately you have plenty of room to carve out a cash buffer. It would seem better to put the non equity to a positive use then just have it sat there doing nothing very much at the moment. So there may be no need to sacrifice performance beyond what one may have done anyway.

3) Yes 40 years will be lower than for 30 years - about 10% from a quick test. On the other hand 10 years into retirement hopefully without a major SORR occuring, you will be at 30 years so the SWR wont remain constant over time. Not only is the risk less for shorter time periods but also in most cases the worst risk wont happen and so you will have more money left after 10 years than planned.

6) Choose whatever % historic success rate gives you the confidence you need to stop working,. You are very unlikely to be following it anyway.

Running a set of cfiresim data to produce SWRs at 95% success rate:

50% equity, 75% equity

30 year: 4.0%, 4.1%

40 year 3.5%, 3.7%

Interesting that the % equity doesnt make as much difference as one may have guessed.0 -

Deleted_User said:

Lets arbitrarily assume that the future will be very much like the recent past. A 1 in 20 probability of running out of money and dying in abject poverty does not make me think “safe”. If you live for 40 or 50 years after retirement that probability goes up quite a bit. The constant should really be called UWR.jamesd said:The US moved from an emerging economy to an economic powerhouse and the UK from a global empire to an ordinary developed country. So the SWRs appear safe against radically different economic progressions.

No reason not to use an SWR for more than thirty years, just calculate one for the desired term. Thirty is long enough that 35 or 40 is close enough to work if people follow the usual pattern of spending declining over time.

Given that the usual 4% rule is calculated for no failures, where does the 1 in 20 probability of failure come from?

Life expectancy is perhaps one possible source, given that I tend to suggest a planning horizon no shorter than giving a five percent chance of still being alive. But the 4% rule is so cautious that even if you're in that five percent you're likely to have lots of money when you die anyway, as Kitces illustrates in The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement

So if in that five percent you'd also need to be in the less than five percent of cases where the 4% rule isn't likely to have lots of money left. That takes it down to 0.25% chance of running out, or less.

But abject poverty isn't in the picture for those in the UK who qualify for a state pension and thereby pension credit. There's not even a need to go there for anyone who acts as I suggest and does lots of state pension deferring for longevity insurance and does significant annuity buying when that starts to beat drawdown. You could have a sequence that blocks those but it's really hard to block deferral because it pays more than drawdown, improving the position of the pot.

There's no need to fear the very long life case because you can prepare for it instead.3 -

That's my own preference, of course, since I prefer the Guyton-Klinger rules, partly because they do help if you encounter something worse than the historic cases.Deleted_User said:Alternatively, you could account for the fact that you are invested in a highly variable market and improve your chances in a meaningful manner by not planning for a constant rate of withdrawal.1 -

Deleted_User said:

Lets arbitrarily assume that the future will be very much like the recent past. A 1 in 20 probability of running out of money and dying in abject poverty does not make me think “safe”. If you live for 40 or 50 years after retirement that probability goes up quite a bit. The constant should really be called UWR.jamesd said:The US moved from an emerging economy to an economic powerhouse and the UK from a global empire to an ordinary developed country. So the SWRs appear safe against radically different economic progressions.

No reason not to use an SWR for more than thirty years, just calculate one for the desired term. Thirty is long enough that 35 or 40 is close enough to work if people follow the usual pattern of spending declining over time.Alternatively, you could account for the fact that you are invested in a highly variable market and improve your chances in a meaningful manner by not planning for a constant rate of withdrawal.

Many people would find it difficult to accept a possibly widely varying rate of income. The compromise I use is to require that everyday expenditure is covered with as near to 100% certainty as can reasonably be achieved barring catastrophic global events when everyone could be in serious difficulty. If that means basing one's plan on a 100% historically successful SWR or reducing overall investment performance to provide a large buffer or to buy an annuity, so be it.

Any expenditure beyond the basics would then rely on performance being better than the worst case scenario. So I suggest one should plan on a steady withdrawal but have no intention of being restricted by the plan if circumstances permit.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards