We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

How much to live on

Comments

-

Thanks, yes, lots to think about![Deleted User] said:jackieblack so with a full state pension you will have an index linked £10636 a year.(From your state pension age)

You need to find out what your other pensions such as your LGPS pension will give you at different ages from say 60.

Also as part of your divorce settlement was there any agreement about pension provision with your ex?

I would also double check that your state pension is definitely £203.85 a week. Its just that you say you have been in the LGPS pension scheme for over 20 years and you may have been opted out for this time. However, if you had NI contributions before that time and after 2015 you may well (as you have said) already qualify for the full amount.

It would also be useful to get an approximate value for your house to help with forward planning.

Do you have an emergency fund and any others savings?

What are your approximate yearly outgoings? Do you manage on your current income?

Perhaps look at different spending/income possibilities from 58 onwards?

Lots of questions and lots to think about. However, planning for the future can also be fun and exciting too!

I currently have two LGPS records - I’ve had several different roles in my 21+ years at the school and there was some reason why two of them couldn’t be merged but I can’t remember what it was (it was a long time ago). As far as I can work out, it looks like I can get about £5k pa at 58 adding the two together (obviously working part time for 25 years has had a big impact), increasing by just over £800 at 60, although I may not be reading that right so need to explore that further. I transferred my only previous pension into the LGPS when I joined.

In the divorce financial settlement we each kept our own pensions.

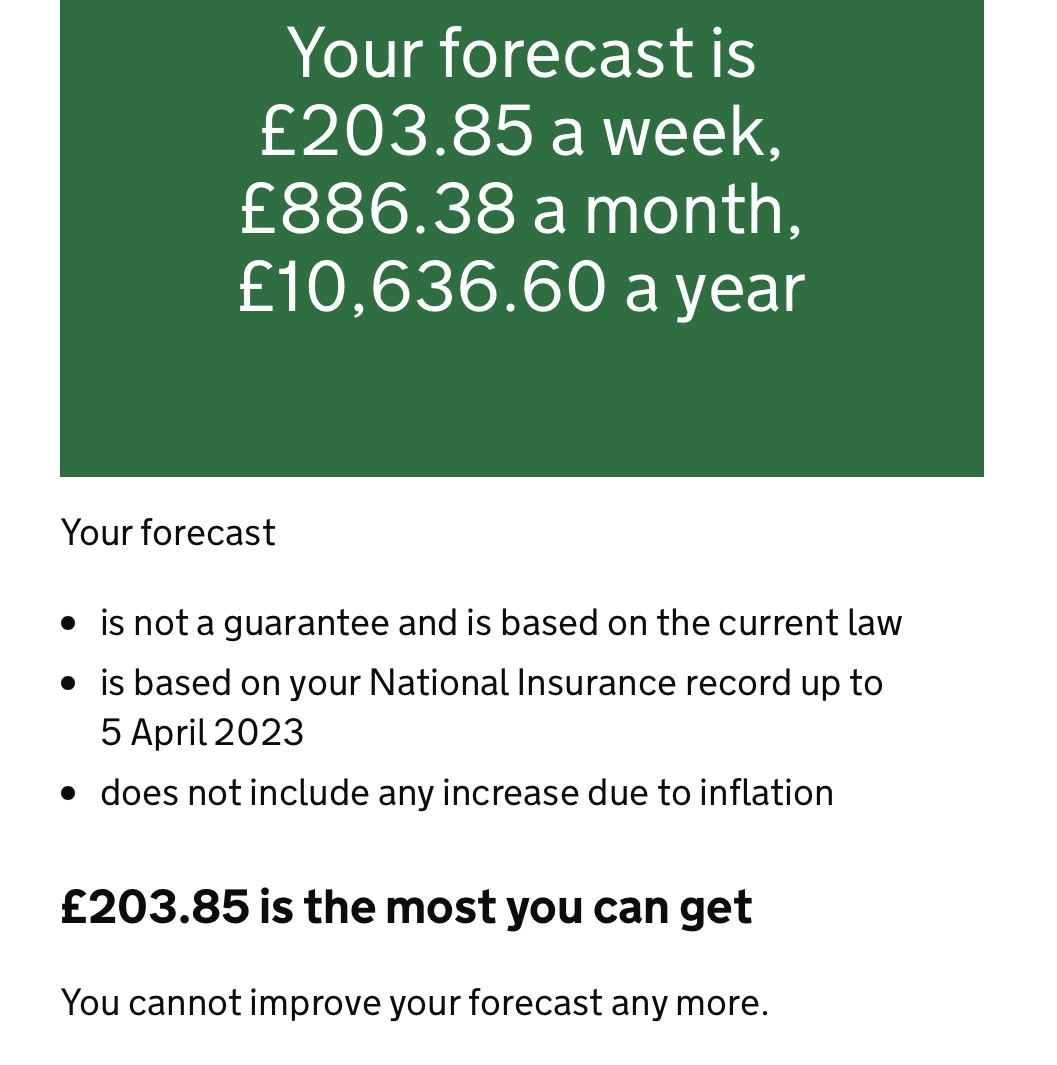

My state pension forecast says this:

I don’t seem to be able to make that any smaller, apologies - I’m not convinced the goal posts won’t be moved again in the next 12 and a bit years…Yes, getting the house valued is on my ‘to do’ list, however between work, granddaughter and parents I’m barely at home and local estate agents don’t appear to be open on Sundays/Bank Hols. May be something for the summer holidays…

Emergency Fund/savings - I have various bits of money tucked away in different accounts and Premium Bonds, I do need to have a sort out - again, maybe in the summer hols…Yearly outgoings, well I did a comprehensive budget over New Year, but recent COL rises mean I really need to redo this. Living closer to my daughter/granddaughter would reduce petrol costs (for us both), some weeks we’re doing 3 or 4 round trips of around 70 miles to facilitate childcare - it’s just as well we can both both walk to work!

Yes, I manage fine on my current income, thanks to increasing my hours a few years ago. I’ve always budgeted for everything and manage/budget to save a bit every month but probably could do better (as my school report always used to say). I would estimate that I could manage fine on £10-12k pa and would be happy to work part time at least until SPA. That wouldn’t, however, leave much/anything to cover replacing anything that breaks down or any travelling - I have two big trips I’d really like to do before I get too decrepit to travel alone. Travelling isn’t possible for the foreseeable future, however, for various reasons (including parents health).Everything will be alright in the end so, if it’s not yet alright, it means it’s not yet the endQuidquid Latine dictum sit altum videtur2 -

jackieblack. Well your state pension looks fine. That's a positive.

So at current values at state pension age annual income would be £16436 before tax (£15662 per annum or £1305 a month after tax) which exceeds your current minimum.

If you took your LGPS pension at 60 you will need to work until state pension age to maintain current lifestyle and perhaps save more for retirement.

I think you will find estate agents more flexible these days when it comes to home visits and valuations.

I appreciate you are very busy but spending an hour or two a week looking at budgets and financial planning will help you achieve your plans.1 -

£1305 a month is more than I have now, so happy with that 🙂

It’s the years prior to getting my state pension that I really need to plan for if I want to go sooner.

Something else to throw in the mix… Pre-Covid, I was planning to leave work and do a full time degree at the local uni. (The student maintenance loan amount was roughly the same as I was earning at the time.) It’s something I’d still like to do, but between granddaughter and parents not possible in the foreseeable future.An hour or two a week to spend on this would be amazing, but unlikely in the current circumstances - during term my brain is too frazzled by the time I get home in the week to do anything that requires a thought process, and on average I get half a day a weekend to myself (and need to do housework/laundry/mow the lawns/do the bins etc).

Maybe in the summer holidays 🤔Everything will be alright in the end so, if it’s not yet alright, it means it’s not yet the endQuidquid Latine dictum sit altum videtur1 -

I'm 57 in September, and having number crunched the finances until the cows come home I've decided to go part time and take my teacher pension early. I've been teaching for 32 years and the teacher pension is a good DB one. I have to take an actuarial reduction which worried me a little, but have argued to myself I'm not losing money - I'm getting less but for longer. Has anyone else gone through this?3

-

Not exactly the same situation as you because I have both DB and DC pensions.Tastiger said:I'm 57 in September, and having number crunched the finances until the cows come home I've decided to go part time and take my teacher pension early. I've been teaching for 32 years and the teacher pension is a good DB one. I have to take an actuarial reduction which worried me a little, but have argued to myself I'm not losing money - I'm getting less but for longer. Has anyone else gone through this?

I wanted to go part time and having looked at all the options decided to take the DB pension early using the same argument as you, smaller monthly amount for a longer period.

The other things that swayed it for me were the number crunching told me that my reduced DB pension plus SP when it becomes payable will exceed my income requirement and due to having no spouse and children now too old for death benefits if I died before taking the payout would have been minimal. I want to get as much out of it as I can!

Still haven’t got round to going part time tho!4 -

Tastiger said:I'm 57 in September, and having number crunched the finances until the cows come home I've decided to go part time and take my teacher pension early. I've been teaching for 32 years and the teacher pension is a good DB one. I have to take an actuarial reduction which worried me a little, but have argued to myself I'm not losing money - I'm getting less but for longer. Has anyone else gone through this?Well here is my similar journey!Back in 2013 when 55 I took the first part phased retirement from teaching with 50% of my retirement benefits. There was a significant reduction but I wanted to continue full time without significant management responsibilities.I worked full time a further 3 years and then took the rest of my pension.

I maximised my lump sum both times, clearing mortgage and any remaining debt which still left me with a useful back in savings and a S&S ISA. I know many agonise about maximising the lump sum and it is frowned upon by many on the pensions board, but it was right for me and I do not regret my decision.

Fortunately, having been full time for 35 years with a good salary the reduced pension is still a decent amount. Also for me it was never totally about maximising income but achieving a work life balance and peace of mind.

From 2017 ‘post retirement’ to the present day, I have undertaken several part time contracts at the same school in pastoral and teaching roles. I will finish completely in early June as they have finally been able to recruit staff for the positions I have been covering. Between 2018 and 2020 I did earn another £600 a year additional pension which again I took at 63. This was added to my main TPS pension.

These contracts have enabled me to pay NI to ensure I will receive the full new state pension from next July,(I will have to pay voluntary one year voluntary as I was contracted out for many years),pay for some house improvements and buy a car without having to dent the financial back up. I have to say that I could have managed fine on my pension, but I enjoyed the work and knew I could give up anytime if I no longer did.

Looking at it in financial terms (Well this is MSE! ) I collected by the age of 60 about £66000 in pension payments as well as a decent lump sum. For me it was a good decision.

I also took at 55 a very small AVC. The tax free lump sum was £2500 and the remaining £10000 was used to buy an annuity that pays on average about £675 a year. I have already had nearly 10 years’ worth. If I’m lucky enough to reach say 80 I will have received nearly £17000 for contributions of just £5000 so not too bad!I suppose I am saying here, yes of course do your research , ask others, perhaps take advice but in the end do what is right for you. This may or may not be the one that maximises income and wealth but enables you to live a happy life.Of course I realise that I was in a good job with a great pension scheme.Although at age 23 I just wanted to teach and knew nothing about pensions, However, when I finish in June I will have worked in education for 42 full and part time years so feel I have earned both my pension and my rest. I will be 65 in July.6 -

I've highlighted what I feel are really important points. I've made decisions that the pensions board wouldn't approve of and same on the Savings board. But we have to do what we're comfortable with and can live with. It isn't just about maximising on the fiscal aspects, but finding a balance and arrangement that fits our personal needs and future plans. So hats off to you for doing that and getting to an arrangement that works well for you - that's all that matters.Baron_Dale said:[snip]I maximised my lump sum both times, clearing mortgage and any remaining debt which still left me with a useful back in savings and a S&S ISA. I know many agonise about maximising the lump sum and it is frowned upon by many on the pensions board, but it was right for me and I do not regret my decision.

Fortunately, having been full time for 35 years with a good salary the reduced pension is still a decent amount. Also for me it was never totally about maximising income but achieving a work life balance and peace of mind.

[snip]

I wish you well in your impending retirement and as far as I'm concerned, anyone who has worked in education for 42 years deserves a whopping great medal and definitely a good rest!

My situation has changed slightly since I last posted my own arrangements, so I might post more about it shortly.7 -

I know many agonise about maximising the lump sum and it is frowned upon by many on the pensions board, but it was right for me and I do not regret my decision.

As 'someone from the Pensions Board' I think some clarity here could be useful for other posters.

For a DB pension, whether to take the lump sum or not is dependent on the commutation rate ( £ of lump sum for each £ of pension given up ) For some public sector schemes, it is only 12, which is poor, so is best avoided if possible. For other public sector and most private sector it is typically 20 to 25. In this case it gets a bit more 50 : 50 and depends on personal circumstances/preferences. Plus the lump sum is tax free.

For a DC scheme, if you want to withdraw from it you are forced to take at least some of the 25% tax free lump sum. However it can work out better to take it in stages, with or without some taxable income as well. What is 'frowned upon' is taking the whole tax free lump sum from a DC scheme, either when you are still working and/or when you have no actual need for it. Normally it is better just to leave it in the pension until you actually need it/retire.

Many people take out the tax free lump sum from a DC pension as soon as they can, when they have no need for it/no idea what to do with it and it just sits in their current account. This is almost always a bad idea.

4 -

I recently took s db at 58, two years before its normal pension date. It was reduced from £4890 at 60 to £4680.Tastiger said:I'm 57 in September, and having number crunched the finances until the cows come home I've decided to go part time and take my teacher pension early. I've been teaching for 32 years and the teacher pension is a good DB one. I have to take an actuarial reduction which worried me a little, but have argued to myself I'm not losing money - I'm getting less but for longer. Has anyone else gone through this?

The reduction was so little it seemed a no brainer. Incidentally, it went up to £5060 IN April.

I think taking a db pension scheme early depends on the reduction. If you have the majority of your pension in a 60 npa it may be ok for you.

I have a few small pensions in payment so i can ease off and go part time like yourself.3 -

Trying to do something similar myself. I'm 56.Tastiger said:I'm 57 in September, and having number crunched the finances until the cows come home I've decided to go part time and take my teacher pension early. I've been teaching for 32 years and the teacher pension is a good DB one. I have to take an actuarial reduction which worried me a little, but have argued to myself I'm not losing money - I'm getting less but for longer. Has anyone else gone through this?

Here's my rough figures.

I worked prior to teaching and have much better commutation factors than the TPS. This allows me to take a lump sum big enough to pay off the mortgage, buy a new car and put solar panels on roof to reduce my bills.

With the phased retirement scheme I will be about £600 a month better off after factoring in the reduction in the mortgage.

I intend recycling this into a SIPP which won't break the recycling rules as it will be less than 30% of my lump sum over 3 years. I currently have another pot valued at about £35k.

I intend to retire fully at 60 years and 7 months. The shortfall in income will be funded either from savings or the above pots until 67 when state pension kicks in. I've factored in holidays, cars etc etc.

During the whole period my effective income is higher than now because I won't be paying a mortgage and importantly I'm still able to save £400 a month or thereabouts until I retire which is rainy day money for the gap until state pension.

To me, it makes no sense flogging myself to remain working full time any longer.7

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards