We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Pension recovery from covid

Comments

-

Yes, I picked up a couple of bargains this year around 10-15% cheaper than they are today. At the time they were at a 6-7% yield. GRID and HICLThrugelmir said:

Even that's pricey now. Renewables are likewise generally trading at substantial premiums. Best route into these is by investing into new IPO's and floatations. Energy prices are falling in particular those for solar power.Prism said:

maybe a touch of alternative stuff like infrastructure.garmeg said:

Care to please share what funds you hold because it may be suitable for my early retirement plans? Certainly need to reduce my pension volatility going forwards.OldMusicGuy said:I set up my portfolio to avoid large downward movements accepting I would lose out on rapid growth during a recovery. That's because I am newly retired and need to protect what I have rather than grow it. I also hold a much higher proportion of cash in my SIPP than most would because I am very concerned about sequence of returns risk and am also very risk averse.

My portfolio was down around 11% from its February high at some of the lowest points of the drops and is currently just under 1.5% above the Feb high. That performance suits my risk profile and investment objectives.Otherwise my job is going to be like Royston Vasey. I'll never leave ...

Not entirely comfortable with a large exposure to China. Though looking ahead. Might well be the way to go.0 -

My 2020

0

0 -

No growth potential? Maybe the raw instrument of "gilts" suggest that.Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.")

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!

I would suggest the BlackRock Over 15 Year Gilt Index Tracker might disagree with your summary of returns:

Feel reasonable to me. Not 'blow your mind amazing', but technically well above our company's default Aviva fund (BlackRock (50:50) Global Equity Index Tracker):

One reason I shifted to a different sounding 'global' fund many years ago: it looked better (BlackRock World ex UK Equity Index Tracker):

One reason I think people need to dig into fact sheets as a basic part of their analysis.

Look at the 3/5/10 year returns (where available) - the difference to 100k from 85.36% to 126.51% or even 183.53% makes a BIG difference.

Not the whole story, clearly, but important for those DIYing.... & also worth looking into if an IFA is suggesting things, and you're ending up with a plethora of funds Plan for tomorrow, enjoy today!1

Plan for tomorrow, enjoy today!1 -

In the 70's long dated gilts were issued with a 17% coupon. Been a bull market ever since as yields progressively declined.Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!0 -

You are confusing me with Thrugelmir. He is claiming (wrongly) that gilts have no potential for growth except yield.cfw1994 said:

No growth potential? Maybe the raw instrument of "gilts" suggest that.Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!

I would suggest the BlackRock Over 15 Year Gilt Index Tracker might disagree with your summary of returns:

Feel reasonable to me. Not 'blow your mind amazing', but technically well above our company's default Aviva fund (BlackRock (50:50) Global Equity Index Tracker):

One reason I shifted to a different sounding 'global' fund many years ago: it looked better (BlackRock World ex UK Equity Index Tracker):

One reason I think people need to dig into fact sheets as a basic part of their analysis.

Look at the 3/5/10 year returns (where available) - the difference to 100k from 85.36% to 126.51% or even 183.53% makes a BIG difference.

Not the whole story, clearly, but important for those DIYing.... & also worth looking into if an IFA is suggesting things, and you're ending up with a plethora of funds1 -

Lets do some arithmetic which will make it clear...Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!

10 years ago there was a 4% 50 year gilt issued. So with £100 invested over 50 years it will generate £200 interest (gilts dont compound) and return your £100.

This gilt is now worth £204. So a 104% capital gain in 10 years - whoopee!! And then there is £40 of interest on top!! Who needs equity!

The gilt will generate £160 interest in the next 40 years. take off the £104 loss in capital value which leaves £56 gain. And oddly enough £144+£56 profit=£200 which is what we calculated originally. So the increase in capital value now is just prepayment of the future returns you would have got anyway.

But now look to the future. In May this year there was a 41 year gilt issued with an interest rate of 0.5%. Clearly there is very little profit that can be brought foward to justify a rise in the capital value. Indeed, it is currently priced at £88, which represents a 12% loss in 6 months.

This is why I am veryt wary of gilts for the non-equity part of my portfolio.

See https://fixedincomeinvestor.co.uk/x/bondtable.html?groupid=3 for source of this data and a lot more.4 -

You are correctly illustrating that capital gains on bonds (“growth”) are possible and in fact that is exactly what we have seen over many decades (contrary to what Thrugelmir claimed) . You are incorrectly claiming that future returns on a bond are known in advance and are certain.Linton said:

Lets do some arithmetic which will make it clear...Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!

10 years ago there was a 4% 50 year gilt issued. So with £100 invested over 50 years it will generate £200 interest (gilts dont compound) and return your £100.

This gilt is now worth £204. So a 104% capital gain in 10 years - whoopee!! And then there is £40 of interest on top!! Who needs equity!

The gilt will generate £160 interest in the next 40 years. take off the £104 loss in capital value which leaves £56 gain. And oddly enough £144+£56 profit=£200 which is what we calculated originally. So the increase in capital value now is just prepayment of the future returns you would have got anyway.

But now look to the future. In May this year there was a 41 year gilt issued with an interest rate of 0.5%. Clearly there is very little profit that can be brought foward to justify a rise in the capital value. Indeed, it is currently priced at £88, which represents a 12% loss in 6 months.

This is why I am veryt wary of gilts for the non-equity part of my portfolio.

See https://fixedincomeinvestor.co.uk/x/bondtable.html?groupid=3 for source of this data and a lot more.Lets look at a government bond in dollars because its easier for me to type. Suppose a bond with a coupon rate of 5% is available with exactly one year until maturity. If the interest rate is 5%, the bond is worth $100. If the interest rate is higher than the coupon value, the value of the bond will be depressed such that the total amount received will be comparable. If interest rates are 7%, there would be a 2% difference between the coupon and the interest rate, and the price would drop by about 2% (to about $98) to compensate. But if the interest rate is only 3%, the bond is worth a bit more (roughly $102), so if you sell it you get growth (capital gain).Future interest rates are unknown. And unpredictable. Therefore you have no idea what your long term bond will be worth in the future. Bond funds never wait until maturity before selling bonds and buying new ones at current rates. We’ve had lots of capital gains/growth on bond funds because interest rates have been dropping for a looong time. On top of all that, what actually matters is real return above inflation and future inflation is also unknown.

The point is that we’ve had a 30 plus year bull market in bonds/gilts and that there have been massive capital gains. Claiming otherwise is to ignore facts. The future is unknown. The potential for a very large drop in interest rates is limited so I agree that the case for buying long term gilts is more difficult than it used to be. I tend to focus on shorter duration. Still, Vanguard and others are making this case and there may be advantages in having gilts even without capital growth, eg so you have dry powder when stocks fall.

0 -

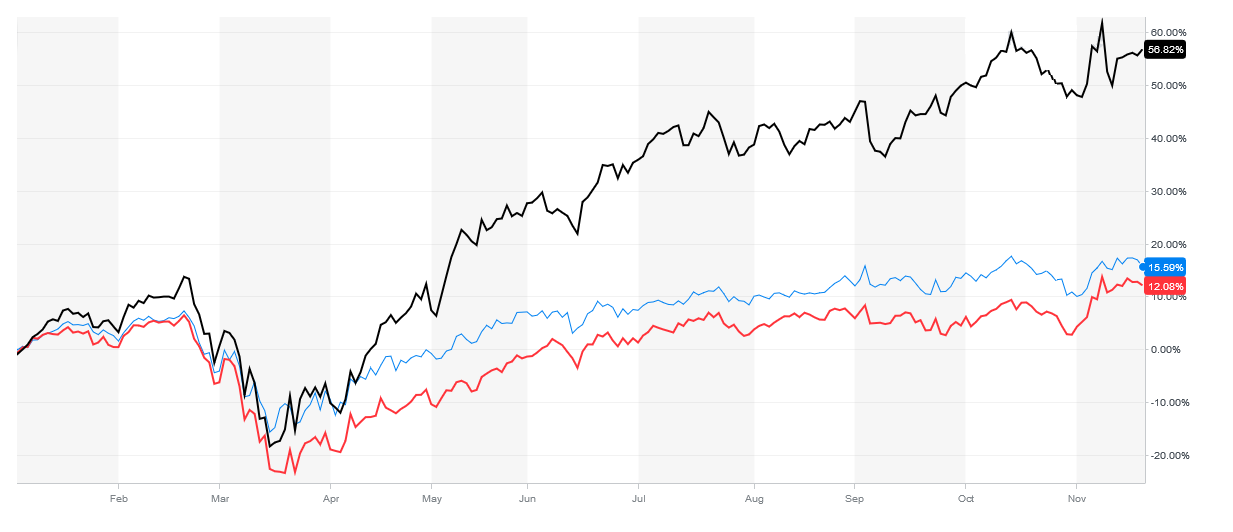

Well if we're sharing pretty charts, here's mine

So points I've noted to myself from the covid crash experience:

1. Everything in my portfolio went down, even the defensives.

2. The blue line in the middle is the £100 SIPP I opened recently with L&G Multi-Index 5 to get a TopCashBack offer. Historically, it fared the worst in terms of recovery so far.

3. The green line is my global government bonds. Took the smallest hit, but then flatlines.

4. The red line is my 'wealth preservation' investments. Took the next smallest hit, and recovering, albeit at a not exciting rate.

5. Yellow and Grey are my global equity ETFs. Biggest hit, but fastest recovery.

So no surprises here. My investments performed as I'd expected considering the circumstances.

The crisis was also a good test of my own behaviour. I just carried on with my regular investing as before, and will keep doing do through the next crash, and the next crash, and the next crash, and the next crash...

Retired 1st July 2021.

This is not investment advice.

Your money may go "down and up and down and up and down and up and down ... down and up and down and up and down and up and down ... I got all tricked up and came up to this thing, lookin' so fire hot, a twenty out of ten..."6 -

I bought 107k SCHP in early January. This is a US TIPS fund (inflation protected government bond). Pays 1.5% coupon. Its worth 115k now for a 8.2% return if you count the interest. Not bad for an asset that does not grow.0

-

Err you do know something about bond rates for the future - they are never going to go significantly below zero. or are you seriously expecting a 5% fall from current interest rates when a 0.5% bond as in my example would have serious value? Without a fall in interest rates you cannot get the capital growth in bond values.Deleted_User said:

You are correctly illustrating that capital gains on bonds (“growth”) are possible and in fact that is exactly what we have seen over many decades (contrary to what Thrugelmir claimed) . You are incorrectly claiming that future returns on a bond are known in advance and are certain.Linton said:

Lets do some arithmetic which will make it clear...Deleted_User said:

If you look at a chart of historic returns for a gilt fund over the last 30 years you will find that the total return far exceeds the yields. What was the reason for that difference?Thrugelmir said:

Gilts offer fixed yields to redemption. They don't offer growth potential. Other than reinvestment of the income. Market prices will fluctuate daily won't impact the eventual outcome.cfw1994 said:

A friend told me his FA (I have no idea if an IFA or FA) had suggested 15yr gilts were going to take a drop some time back. Some of my “less risky” money is in a blackrock 25yr gilt tracker: it looked better than the similar bond option I had. I left it there....garmeg said:

Potentially this fund has to last 30 years plus as i am 56 so needs a high equity allocation.Deleted_User said:

If it was me, I would consider a more defensive portfolio. Now that things calmed down could be a good time. In March/April would have been bad time.garmeg said:Looking at my crystallised SIPP, I am down 6% from when i crystallised it in 2019 and down 15% from its February 2020 peak. It was 40% down from February at its worst (having ASEI Aberdeen Standard Equity Income and TMPL Temple Bar ITs didnt help alongside too much UK generally) so it is recovering.

Large movements like this do make it hard to make a decision about when to retire. Guess I will be a perpetual "One More Year" employee.

Maybe 80% in equity ETF and keep 20% in cash as bonds not good value now.

Something like VWRL or the HSBC and Fidelity ETFs?I can now see the past year has managed to muster 7.5% growth, which I am happy with.Partly makes me wonder where finance “specialists” get their ideas from!

10 years ago there was a 4% 50 year gilt issued. So with £100 invested over 50 years it will generate £200 interest (gilts dont compound) and return your £100.

This gilt is now worth £204. So a 104% capital gain in 10 years - whoopee!! And then there is £40 of interest on top!! Who needs equity!

The gilt will generate £160 interest in the next 40 years. take off the £104 loss in capital value which leaves £56 gain. And oddly enough £144+£56 profit=£200 which is what we calculated originally. So the increase in capital value now is just prepayment of the future returns you would have got anyway.

But now look to the future. In May this year there was a 41 year gilt issued with an interest rate of 0.5%. Clearly there is very little profit that can be brought foward to justify a rise in the capital value. Indeed, it is currently priced at £88, which represents a 12% loss in 6 months.

This is why I am veryt wary of gilts for the non-equity part of my portfolio.

See https://fixedincomeinvestor.co.uk/x/bondtable.html?groupid=3 for source of this data and a lot more.Lets look at a government bond in dollars because its easier for me to type. Suppose a bond with a coupon rate of 5% is available with exactly one year until maturity. If the interest rate is 5%, the bond is worth $100. If the interest rate is higher than the coupon value, the value of the bond will be depressed such that the total amount received will be comparable. If interest rates are 7%, there would be a 2% difference between the coupon and the interest rate, and the price would drop by about 2% (to about $98) to compensate. But if the interest rate is only 3%, the bond is worth a bit more (roughly $102), so if you sell it you get growth (capital gain).Future interest rates are unknown. And unpredictable. Therefore you have no idea what your long term bond will be worth in the future. Bond funds never wait until maturity before selling bonds and buying new ones at current rates. We’ve had lots of capital gains/growth on bond funds because interest rates have been dropping for a looong time. On top of all that, what actually matters is real return above inflation and future inflation is also unknown.

The point is that we’ve had a 30 plus year bull market in bonds/gilts and that there have been massive capital gains. Claiming otherwise is to ignore facts. The future is unknown. The potential for a very large drop in interest rates is limited so I agree that the case for buying long term gilts is more difficult than it used to be. I tend to focus on shorter duration. Still, Vanguard and others are making this case and there may be advantages in having gilts even without capital growth, eg so you have dry powder when stocks fall.

Interestingly my demonstration of 144% growth in 10 years arising from falling interest rates represents a 9% annualised rate of return, which is similar to that of long dated gilt funds. So there is no evidence there that the fund itself is adding significant extra return by clever trading, reinvestment or whatever.

But in any case major rises and falls in value are not compatible with the objective of buying bonds in the first place which are supposed to provide a level of security.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards