Current debt-free wannabe stats:

We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Mortgage broker - ask me anything

Comments

-

@bm645 I can't really give you any advice or pointers on what to do but my very general thoughts based on the limited info in your posts -BM645 said:Hi,

I have received my mortgage offer in the last two weeks but very nervous about it being pulled. For context mortgage value is approx 1.5x my salary, so in affordability terms it's fine (it's a major high street lender). However:

1) I have already sold my house, and address has changed since I made the application (living with parents short term, and not registered on electoral role here). Is this an issue, if it is I worry it will become one due to point 2 as the bigger issue.

2) The bigger issue, I have since relapsed from a bad gambling addiction since I submitted my application. There was nothing for concern on my bank statements at the time of application, but in the weeks since I have withdrawn and deposited over 12-14k in cash. Multiple transactions a day in excess of 1k some days. All balances out (no real profit or loss, fortunately) but clearly wouldn't look great to a lender. As part of this I accidentally withdrew cash on a credit card a couple of times as a cash advance (literally just used the wrong card, paid off instantly). I am concerned the cash advances will flash up on my credit file and trigger my case to be reviewed at completion stage, and then offer to be pulled if/when asked to re-supply bank statements. For further context I have since stopped gambling this last week and now getting support so not an ongoing issue, I have just read that banks apparently re-check you at completion stage so naturally am nervous.

I am now being asked to exchange contracts with intention to complete in 3 weeks or so (new build, no chain). I'm nervous about exchanging in the event my mortgage offer was pulled, as clearly based on my updated bank statements, I'd assume I'd have no chance of getting another mortgage offer, and be committed to buying a property that I assume nobody would lend to me.

I do suffer with really bad anxiety so hoping this is one of these things but just wanted to ask an expert to understand if this is something I should be worrying about.

Please let me know.

1) I wouldn't worry about that too much.

2) If the lender were to be aware of what you've described, it could well lead to the offer being reviewed.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

K_S said:

@bm645 I can't really give you any advice or pointers on what to do but my very general thoughts based on the limited info in your posts -BM645 said:Hi,

I have received my mortgage offer in the last two weeks but very nervous about it being pulled. For context mortgage value is approx 1.5x my salary, so in affordability terms it's fine (it's a major high street lender). However:

1) I have already sold my house, and address has changed since I made the application (living with parents short term, and not registered on electoral role here). Is this an issue, if it is I worry it will become one due to point 2 as the bigger issue.

2) The bigger issue, I have since relapsed from a bad gambling addiction since I submitted my application. There was nothing for concern on my bank statements at the time of application, but in the weeks since I have withdrawn and deposited over 12-14k in cash. Multiple transactions a day in excess of 1k some days. All balances out (no real profit or loss, fortunately) but clearly wouldn't look great to a lender. As part of this I accidentally withdrew cash on a credit card a couple of times as a cash advance (literally just used the wrong card, paid off instantly). I am concerned the cash advances will flash up on my credit file and trigger my case to be reviewed at completion stage, and then offer to be pulled if/when asked to re-supply bank statements. For further context I have since stopped gambling this last week and now getting support so not an ongoing issue, I have just read that banks apparently re-check you at completion stage so naturally am nervous.

I am now being asked to exchange contracts with intention to complete in 3 weeks or so (new build, no chain). I'm nervous about exchanging in the event my mortgage offer was pulled, as clearly based on my updated bank statements, I'd assume I'd have no chance of getting another mortgage offer, and be committed to buying a property that I assume nobody would lend to me.

I do suffer with really bad anxiety so hoping this is one of these things but just wanted to ask an expert to understand if this is something I should be worrying about.

Please let me know.

1) I wouldn't worry about that too much.

2) If the lender were to be aware of what you've described, it could well lead to the offer being reviewed.

Thanks. I guess to your second point as to the lender becoming aware, what final checks do they do before completion? There has been nothing changed in my credit file (with the exception of the 2 accidental cash advances which were paid off, if these were reported). I have purchased a number of properties in the past, in which the mortgage offer was issued a couple months before completion and was never asked to submit updated bank statements. I guess I am just looking for a gauge as to the level of risk.0 -

Thanks a billion! Yes, my broker has my CMF report as of yesterday and will go through with the underwriter to correct today...K_S said:

@annethemanannetheman said:

Thanks a million @K_S!K_S said:

@annetheman Unless I'm missing something obvious, I can't think of why a lender would adjust affordability for a historic AR on an account that has been fully settled. Or why an AR that isn't even on the credit report, on a loan that is long closed, would come up at all by itself.annetheman said:Hi brokers,

I'm on my 4th mortgage application this year (3 offers previously received -- 1 rescinded after I switched house and that house failed valuation, 1 expired because the purchase was taking so long, 1 active but I've pulled out of that house due to length of time...).

Virgin Money have refused to lend the amount I applied for (offered a lower amount) because of something in my report - my broker is speaking with underwriter, but as we are only at AIP stage and Virgin Money do hard checks just for AIP then again for full, I am wondering if it's worth the bother...

There are 2 issues with my report - 1st is a NatWest credit card missed payment (total £400 on a credit card I did not set up a direct debit for in May 2022, entire card paid off in full the next month). 2nd is an arrangement to pay a £3,400 NatWest loan in May 2017 when I was in an unstable contract job, next month I caught up with repayments and no issues until end of that loan.

Because the AR was in 2017, I didn't declare it, but my broker knew of the 2022. Is it worth the bother, since I know I can get the full amount from another lender (albeit at a higher rate)?

Thanks for your thoughts. Of course I have full faith in my brilliant broker but just good to hear opinions anyway!

The lender's system can adjust affordability downwards at AIP if it picks up existing commitments from the credit report that haven't been declared (or its system incorrectly thinks haven't been declared) on the AIP form.

Once your broker has a look at your latest Experian report, they should be able to figure out what the confusion is. If the downward adjustment is indeed an error, your broker should be able to correct, rerun the AIP (without a new hard check) and then proceed to full app.

If the downward adjustment isn't an error, then you could just use the next best lender.

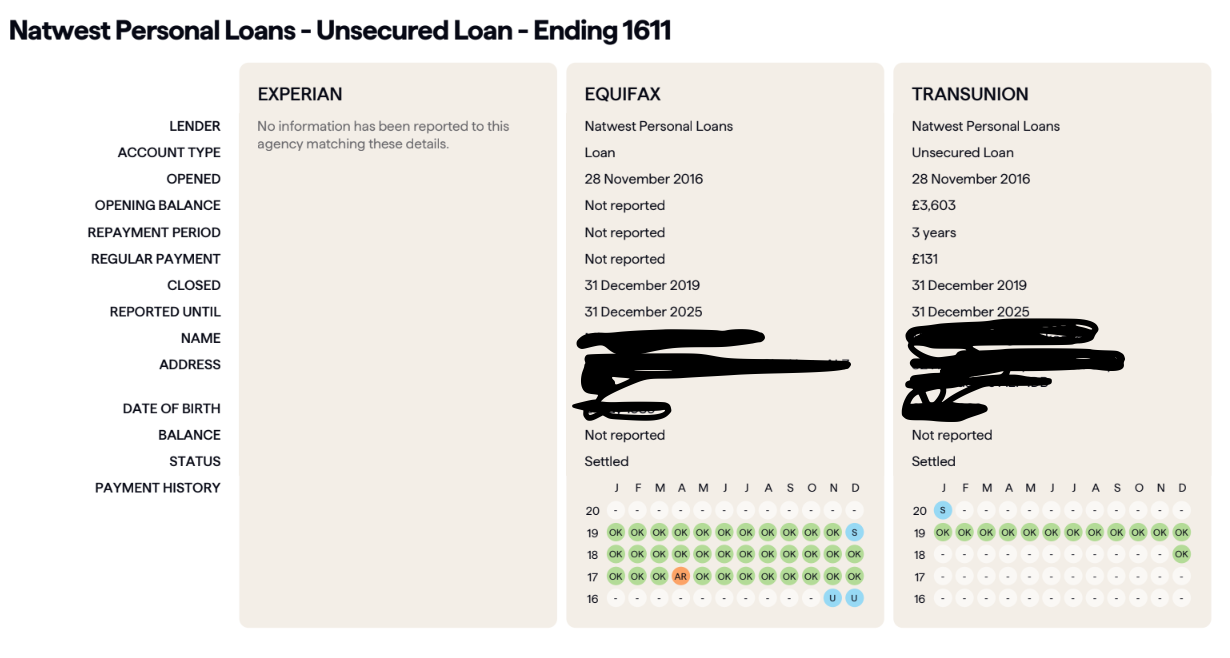

Do you think it could be this: I recently settled Tesco Loan that was £144 per month (£2,400 final payment was made as a lump sum on 21st October) -- we think the settlement hasn't registered but I sent my settlement letter to broker so I think she will discuss this with them. Do you think they didn't look at the letter? It is not showing as cleared on Equifax, but is on Transunion and nothing at all on Experian. Do they use Equifax?

This is the Natwest AR May 2017:

This is the Tesco loan settled 21 October 2024:

I also sold my flat 23 August (so settled mortgage in full, but that is showing on all reports), so recently on electoral roll at my temp address (perfect credit person lives here, no linked bad credit).

Basically it's just a mess now compared to before!

Noted that if the downward adjustment is deliberate we'll just go with the other lender (0.50% higher rate

Thank you!

Reduced affordability - it could well be the settled-but-not-updated Tesco loan that Virgin's AIP picked up automatically. Everything is automated at the AIP stage and the letter comes in only if/when there is any kind of manual adjustment. I can't remember if Virgin do that or not, or at what stage. Or it could be a simple matter of the broker correcting/tweaking the application.

AR marker from 2017 - if it's on the credit report, it will have been picked up by Virgin's AIP but would not impact affordability as the account is long settled. The impact that may have had would be either a decline at AIP or an LTV cap which I don't think has happened based on what you said. Unless it's a 95% LTV max-borrowing app, I can't imagine that a single 7+ year old AR marker would cause an application decline. You've had 4+ successful applications already!

I wouldn't stress too much, just make sure your broker has a copy of your latest CMF report so they can confirm what the confusion is and sort it out.

All the best!

I did ask NatWest this morning to change my April 2017 AR to a default so it can drop off, she says I didn't need to do that and it is the Tesco Loan.

I asked if it was worth the bother and she is confident this can be corrected, I am still doubtful and unsure...

She says as it was not a decline, the hard DIP search can be explained ahead should we apply to Accord (next best - 5.34% as unfortunately it is a 95% LTV) who are "common sense".

She did successfully do my 3 other apps so I'll do whatever she says. Thanks so much for the advice also!

Just reaffirms the need to change absolutely nothing in the run up to application, even if it's something positive like clearing a debt - I will ALWAYS give at least 3 months after any change before applying again... Thank you!!!Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66Debt-free target: 21-Mar-2027

Debt-free diary0 -

Afternoon all

So I have had a load of defaults fall off my credit file & have one left to go, next March.

I have accrued a little CC debt but what I'd like to know is when I go to apply for a mortgage with my wife next summer (currently just me on the existing mortgage), can I say I intend to clear the existing debt with the proceeds of our sale? The house is worth £135,000 & I have £70,000 on the mortgage.0 -

Hi, I am looking for an adverse mortgage broker. House is estimated value £360k, left on mortgage £220k. I am self employed (2 years books) partner f/t employed. We have debts of £40k. Credit score awful. Currently on a token payment plan with Stepchange, I suspect we won't have any options to stay put. Natwest (current lender) won't touch us which I expected. We really want to do some work on the house to increase it's size a bit and if we can't borrow more we will move. Would rather stay put though. We don't meet affordability with Natwest due to my self employed earnings.

Could just do with either a broker reccomendation or a mortgage company I can go direct to. I was going to try LBS as heard they do sub prime? But maybe a broker would be better?

Thanks in advance") 0

0 -

@penguin_ Generally speaking, yes you can mark some debts to be paid off on completion on the application form. Depending on the LTV and specific lender, it may or may not make a difference to the outcome.Penguin_ said:Afternoon all

So I have had a load of defaults fall off my credit file & have one left to go, next March.

I have accrued a little CC debt but what I'd like to know is when I go to apply for a mortgage with my wife next summer (currently just me on the existing mortgage), can I say I intend to clear the existing debt with the proceeds of our sale? The house is worth £135,000 & I have £70,000 on the mortgage.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

@misslisa Ignore your 'credit score'. What I would suggest doing is getting a copy of your Experian and Equifax credit reports (or at least one of them) for both applicants, copies of your self-employed income for two years (SA302s, Tax Year Overviews and full accounts), details of your DMP and speaking to a 'normal' broker first, one that has the time to review these and then tell you whether they can help or not. The MSE guide here has a list of brokers that you can approach, look towards the lower end of the list.misslissa said:Hi, I am looking for an adverse mortgage broker. House is estimated value £360k, left on mortgage £220k. I am self employed (2 years books) partner f/t employed. We have debts of £40k. Credit score awful. Currently on a token payment plan with Stepchange, I suspect we won't have any options to stay put. Natwest (current lender) won't touch us which I expected. We really want to do some work on the house to increase it's size a bit and if we can't borrow more we will move. Would rather stay put though. We don't meet affordability with Natwest due to my self employed earnings.

Could just do with either a broker reccomendation or a mortgage company I can go direct to. I was going to try LBS as heard they do sub prime? But maybe a broker would be better?

Thanks in advance

https://www.moneysavingexpert.com/mortgages/best-mortgages-cashback/#step3

If your credit situation is indeed 'bad' enough that they can't help, then you may need to go to brokers that specialise in heavy adverse.

I see clients time-and-again who assume their credit-report situation is far worse than it actually is, so make sure you've explored cheaper options before looking at heavy-adverse brokers that charge £1,000+.

If you would prefer to go direct, and understand what you might be missing out on by doing so, then to find out whether or not a lender will lend to you, you could consider running a soft-check DIP. If the DIP comes back positive then that's as much assurance as you can get at this stage. For Leeds (and most mainstream lenders) that would be step 2 in the below sequence. If you're on a DMP and have multiple recent adverse on your credit reports, this approach is highly unlikely to bear fruit.

All the best, hope it all works out!

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi @K_S and all,

Offer accepted for a house that I and my foreign national spouse love. It is a recently renovated property where a larger property has been split into two dwellings, and which has previously not been occupied, therefore classified by most lenders as a new build.

The vendor/seller has not split the title deeds yet, so whole property has only one land registry title. Apparently, that can take 6 months. (and yes, he should have done this before putting this up on market)

I am struggling to find a lender which fits our case (spousal visa + new build), even though we have a big deposit of at least 25%.

Should I ask the vendor to start the process for changing title deeds and keep the property on hold for us for 6 months/until it is done? Is there another way we can approach this, and still manage to keep the property for us?

I really love the property, and don't want to see it let go. Any advice welcome. Thanks.0 -

@fatcatonamat Sorry I'm not entirely sure what the issue is. You have a 25%+ deposit so that takes of the 75% LTV cap for non-ILR that many (not all) lenders have. It's a new build, and that isn't an issue either as long as the builder is offering one of the acceptable warranties.

I'm not entirely sure how the state of the title impacts the mortgage, but most new-builds will come with a fresh title and nothing on the land registry when the mortgage application goes in.

The spousal visa (and/or time to expiry) could be a roadblock with some lenders if you need their income to be considered but I can't imagine that it'd stop you from getting a mainstream mortgage.

What specifically is stopping you, can you give an example of what lenders have said?fatcatonamat said:Hi @K_S and all,

Offer accepted for a house that I and my foreign national spouse love. It is a recently renovated property where a larger property has been split into two dwellings, and which has previously not been occupied, therefore classified by most lenders as a new build.

The vendor/seller has not split the title deeds yet, so whole property has only one land registry title. Apparently, that can take 6 months. (and yes, he should have done this before putting this up on market)

I am struggling to find a lender which fits our case (spousal visa + new build), even though we have a big deposit of at least 25%.

Should I ask the vendor to start the process for changing title deeds and keep the property on hold for us for 6 months/until it is done? Is there another way we can approach this, and still manage to keep the property for us?

I really love the property, and don't want to see it let go. Any advice welcome. Thanks.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thanks @K_S.

We are okay on the spousal visa front. Even Halifax were okay and we met the affordability criteria. Proceeded to the mortgage valuation and failed there.

The seller has divided the larger property into two dwellings. This has been notified to the city council, and the TP1 is under process.

My solicitor was told by Halifax that "they do not wish to lend unless the title has been separately registered for six months."

Another issue could be I think the seller did not provide building warranties. They provided electrical warranties for all the rewiring of the house etc. But my solicitor knows about this and she tells me that since it is not a 'new build' there won't be any building warranties. Yet, lender is classifying it as a new build because it has renovation work done and we would be first occupancy.

How can we go about this?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards