We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

I have a question about UK mortgage lending. Do any providers accept SIPP pension drawdown as "income" to support a mortgage. I can understand why some wouldn't because SIPP drawdown is not guaranteed income as it would be with annuity or DB income. Ignoring those that don't are there any who do? Thanks1

-

Yes. Some do, some don't. Percentage varies from lender to lender but 3-4% of fund value is common.Sunnylifeover50plan said:I have a question about UK mortgage lending. Do any providers accept SIPP pension drawdown as "income" to support a mortgage. I can understand why some wouldn't because SIPP drawdown is not guaranteed income as it would be with annuity or DB income. Ignoring those that don't are there any who do? ThanksI am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.1 -

@sunnylifeover50plan I'll echo what Kingstreet has said above.Sunnylifeover50plan said:I have a question about UK mortgage lending. Do any providers accept SIPP pension drawdown as "income" to support a mortgage. I can understand why some wouldn't because SIPP drawdown is not guaranteed income as it would be with annuity or DB income. Ignoring those that don't are there any who do? Thanks

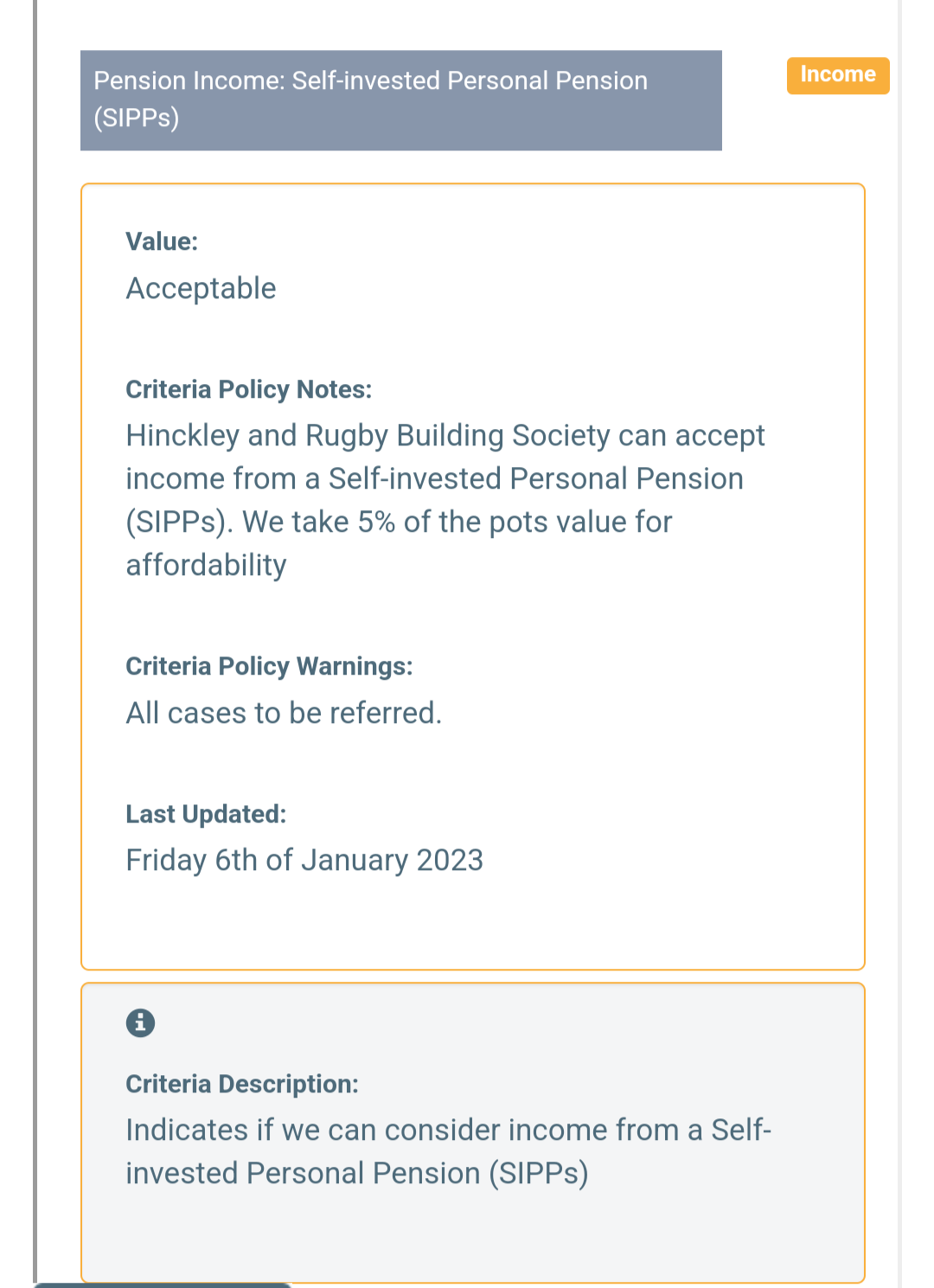

Most don't, some do. Most of the lenders that may consider future SIPP income are smaller building societies, for instance the H&R BS criteria that I've pasted below. Unlike standard PAYE income or DB pension income, it will almost certainly be subject to a manual review (with some level of subjectivity involved) and will come with a host of associated criteria - age, term, years from retirement, etc. that varies across lenders.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

thankyou @K_S and @kingstreet0

-

I wanted to get a mortgage based on SIPP flexible drawdown, but struggled - I can't say for sure if the broker checked every single lender, but no luck. In the end, I got round it by purchasing a fixed term annuity to provide enough guaranteed/provable income for slightly longer than the mortgage term I was looking for.Sunnylifeover50plan said:I have a question about UK mortgage lending. Do any providers accept SIPP pension drawdown as "income" to support a mortgage. I can understand why some wouldn't because SIPP drawdown is not guaranteed income as it would be with annuity or DB income. Ignoring those that don't are there any who do? Thanks

With the fixed term annuity, that opened up main stream, hight street lenders - currently going through an application with Nat West at the moment. Not approved just yet, so hopefully not tempting fate by posting this now 1

1 -

Hi

Just after a bit of advice please before I start getting solicitors and brokers involved.

My mum wants to move closer to us. She is retired, owns her property outright (probs worth about 90k).

I live with my partner. House in my name only (he had credit issues when we moved in 10 years ago all clear now).

House prices in our area much more expensive than my mums. Could my mum put her 90k down as a deposit and partner get a mortgage for the rest? Only mum would be living in the property. I am an only child.

I am absolutely boggled with all the deliberate deprivation of assets stuff.

Thanks in advance

0 -

@emmad1982 First off, try stop worrying too much about the DoA stuff. Most of what's written about DoA on these forums might be well-intentioned but is often wrong and scaremongering. If your mum is currently in good health and able to take care of herself, financial decisions made during this time are very unlikely to meet the strict thresholds for something to be considered as DoA.EmmaD1982 said:Hi

Just after a bit of advice please before I start getting solicitors and brokers involved.

My mum wants to move closer to us. She is retired, owns her property outright (probs worth about 90k).

I live with my partner. House in my name only (he had credit issues when we moved in 10 years ago all clear now).

House prices in our area much more expensive than my mums. Could my mum put her 90k down as a deposit and partner get a mortgage for the rest? Only mum would be living in the property. I am an only child.

I am absolutely boggled with all the deliberate deprivation of assets stuff.

Thanks in advance

Setting that aside, there are a few ways that people typically do something like this -

- Mum buys the property using the 90k as deposit (she will be the sole owner) and your partner will be on the mortgage along with her but not on the deeds. Mum makes the mortgage payments, though your partner will jointly be responsible for the upkeep of the mortgage. This way your mum owns the property 100%. What you would use for this is called a JBSP (Joint Borrower Sole Proprietor) mortgage.

- You do a transfer-of-equity on your property to add your partner to the mortgage (you'll be able to keep the fix you're on). Once that is done (or alongside that process), you consider releasing equity through a further advance/additional borrowing, adding it up to the 90k and use that to buy a property for mum outright. You could either join her as an owner on the deeds (% corresponding to deposit as tenants in common) or loan her the money secured against the property she's buying.

- other ways to achieve a similar result

In both the ways I've described, your mum gets full benefit of her 90k.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi there,I am in the process of buying a flat and my father gave me part of the deposit as a gift (83K-but will use half if possible waiting for the mortgage offer) The gift deposit is from overseas, in the EU.I am providing:-EEA National Photo Card ID Notarised (confirming identity),-EEA Driving Licence Photo Card Notarised (confirming address),-Gift Letter,-6 Month bank statement translated into English showing the transfer and address of my father.-My bank statement shows the gift deposit transferred to my UK bank account.Now, the solicitor assistant saying they don't accept EEA National ID's, and asking for a Passport or Birth Certificate.My father doesn't have a passport and he is 86 years old, I believe He provided every information required to run Money Laundering Checks.I will have a call with the solicitor but I would like to ask your opinion about it.Thanks0

-

@grrowthh Sorry to hear about the trouble you're having.

Unfortunately the nitty-gritty of AML and proof-of-deposit checks is down to the solicitor's processes. There is no set process or list of documents required, each firm is expected to do the necessary steps to be able to meet their regulatory obligations and confirm to the lender that they have done the same.

For example, when I have clients whose source of deposit is from xxxx, I will often suggest using a particular London based solicitor firm for conveyancing as they are comfortable handling funds from xxxx (not all solicitors will) and have offices there who will verify documents without needing to be translated. Other firms will have different policies towards deposits from xxxx.

All I can suggest is telling the solicitor the facts - that your father doesn't have a passport - and ask for alternatives. All the best, hope it gets sorted soon!grrowthh said:Hi there,I am in the process of buying a flat and my father gave me part of the deposit as a gift (83K-but will use half if possible waiting for the mortgage offer) The gift deposit is from overseas, in the EU.I am providing:-EEA National Photo Card ID Notarised (confirming identity),-EEA Driving Licence Photo Card Notarised (confirming address),-Gift Letter,-6 Month bank statement translated into English showing the transfer and address of my father.-My bank statement shows the gift deposit transferred to my UK bank account.Now, the solicitor assistant saying they don't accept EEA National ID's, and asking for a Passport or Birth Certificate.My father doesn't have a passport and he is 86 years old, I believe He provided every information required to run Money Laundering Checks.I will have a call with the solicitor but I would like to ask your opinion about it.Thanks

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi,

was really hoping that I could be given some advice please. My wife & I are starting the divorce proceedings and will be selling the house so should receive £35-£45k each.I would eventually like to buy again as a single, potentially shared ownership. However, around 2 months ago I stopped paying my unsecured debts to get into a DMP. Totals around £28k. The accounts haven’t defaulted yet, but shows as a late payment on one.I have two options (I think)

1- get back up to date with the payments, struggle with money until the house sells and pay them all off. This will avoid the defaults on credit score2- continue with the DMP & have a poor credit record for 6 years.Like I said I would love to eventually buy my own place again, I’m not sure what option to go for I terms of a better future with mortgage rates etc?Thanks so much0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards