We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@thewannabedebtfree From a purely mortgage point of view, and based on the limited info in your post - option 1 is likely be better, as in have less of an adverse impact on your credit report.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Thank you, so I’ve just worked out it’s not £28k unsecured it’s more £38K, so if we sell the house and I pay them all of id be left with £0! (If I paid them off)K_S said:@thewannabedebtfree From a purely mortgage point of view, and based on the limited info in your post - option 1 is likely be better, as in have less of an adverse impact on your credit report.

I have an active claim going through the courts and have been advised I’d get upwards of £50k, hopefully next year at some point.So now thinking, continue with the DMP plan, as otherwise I’d walk away from the sale with £0. Wait for the other money next year, and put a pretty hefty deposit down for a new home.Would I likely get a mortgage with recent active defaults? (<1 year old) using a larger deposit, or would you say to avoid the defaults at all costs?

idea is I’d get a few settlement offeres down the line.Thank you0 -

@Thewannabedebtfree There are a lot of things you're saying here, different potential scenarios, etc. It's really not possible to say with any certainty how exactly your credit report should look like to maximise your chances of a mortgage at an uncertain point in the future.Thewannabedebtfree said:

Thank you, so I’ve just worked out it’s not £28k unsecured it’s more £38K, so if we sell the house and I pay them all of id be left with £0! (If I paid them off)K_S said:@thewannabedebtfree From a purely mortgage point of view, and based on the limited info in your post - option 1 is likely be better, as in have less of an adverse impact on your credit report.

I have an active claim going through the courts and have been advised I’d get upwards of £50k, hopefully next year at some point.So now thinking, continue with the DMP plan, as otherwise I’d walk away from the sale with £0. Wait for the other money next year, and put a pretty hefty deposit down for a new home.Would I likely get a mortgage with recent active defaults? (<1 year old) using a larger deposit, or would you say to avoid the defaults at all costs?

idea is I’d get a few settlement offeres down the line.Thank you

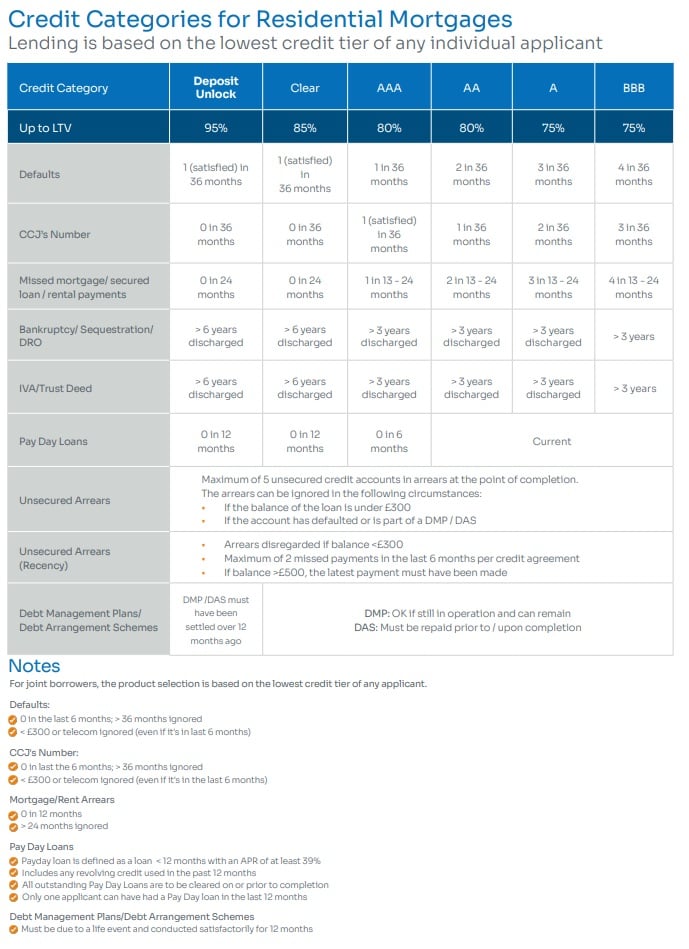

Bluestone is a heavy-adverse lender, and this is their product guide. https://bluestonemortgages.co.uk/wp-content/uploads/2024/12/Residential_Product_Guide.pdf?nocache=1 They have a matrix in there (screenshot below) which shows the details of the degrees of adverse credit they will consider at different LTVs, recency and number of defaults, acceptable DMP details, etc.

If even Bluestone will not consider an applicant due to their credit history, then the universe of potential mortgage options out there is likely to be tiny.

Hope that helps in some way!

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

2 -

K_S said:

@Thewannabedebtfree There are a lot of things you're saying here, different potential scenarios, etc. It's really not possible to say with any certainty how exactly your credit report should look like to maximise your chances of a mortgage at an uncertain point in the future.Thewannabedebtfree said:

Thank you, so I’ve just worked out it’s not £28k unsecured it’s more £38K, so if we sell the house and I pay them all of id be left with £0! (If I paid them off)K_S said:@thewannabedebtfree From a purely mortgage point of view, and based on the limited info in your post - option 1 is likely be better, as in have less of an adverse impact on your credit report.

I have an active claim going through the courts and have been advised I’d get upwards of £50k, hopefully next year at some point.So now thinking, continue with the DMP plan, as otherwise I’d walk away from the sale with £0. Wait for the other money next year, and put a pretty hefty deposit down for a new home.Would I likely get a mortgage with recent active defaults? (<1 year old) using a larger deposit, or would you say to avoid the defaults at all costs?

idea is I’d get a few settlement offeres down the line.Thank you

Bluestone is a heavy-adverse lender, and this is their product guide. https://bluestonemortgages.co.uk/wp-content/uploads/2024/12/Residential_Product_Guide.pdf?nocache=1 They have a matrix in there (screenshot below) which shows the details of the degrees of adverse credit they will consider at different LTVs, recency and number of defaults, acceptable DMP details, etc.

If even Bluestone will not consider an applicant due to their credit history, then the universe of potential mortgage options out there is likely to be tiny.

Hope that helps in some way!Thank you so much, sorry but it I have 5 defaults that will eventually go onto a DMP, will this exclude bluestone (as the BBB states 4 defaults in 36 months)? All the defaults are unsecured loans/credit cards, so not sure if this comes under unsecured arrers rather than defaults?

apologies for the questions, just time is running out before they default and want to secure mine and sons future hopefully in own property. Just don’t really understand the chart being non-mortgage wise

thanks again0 -

I have a question - essentially in 3 months time my landlord is selling the home I've been living in for 10 years - but giving me the option to buy it. I doubt I will be lent 100% of the mortgage required, but have been looking at shared ownership options. However usually these arrangements are for properties that housing associations already own (typically new developments) or are selling on behalf of a developer.

My issue is that the owner in this case is my landlord (so not a housing association) - so I'm looking for a 3rd party (could be anyone or any lender) to take a share in the ownership (rent typically paid on the part of the mortgage I don't own). I don't think a housing association would be interested if they aren't already involved in the property (ie. are selling it themselves), so unlikely, but possible perhaps - so would a bank or building society be interested?

What products/lenders/options would be possible options here? Many thanks for any suggestions.

0 -

@hedgerow2024 Afaik, no bank or BS will offer an SO mortgage option in the scenario described.Hedgerow2024 said:I have a question - essentially in 3 months time my landlord is selling the home I've been living in for 10 years - but giving me the option to buy it. I doubt I will be lent 100% of the mortgage required, but have been looking at shared ownership options. However usually these arrangements are for properties that housing associations already own (typically new developments) or are selling on behalf of a developer.

My issue is that the owner in this case is my landlord (so not a housing association) - so I'm looking for a 3rd party (could be anyone or any lender) to take a share in the ownership (rent typically paid on the part of the mortgage I don't own). I don't think a housing association would be interested if they aren't already involved in the property (ie. are selling it themselves), so unlikely, but possible perhaps - so would a bank or building society be interested?

What products/lenders/options would be possible options here? Many thanks for any suggestions.

In the pre-covid low interest era there used to be a handful of 'innovative' companies (not banks or lenders) which supposedly offered a part-buy part-rent scheme for non-new-build properties, but I don't really know anything about it. From a quick Google search - this is one example https://www.which.co.uk/news/article/new-scheme-offers-mortgage-free-homeownership-to-first-time-buyers-afDIO8J7X1J2I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Thank you - I'll take a look at Unmortgage!

0 -

Just FYI, Unmortgage are now known as WayHome - there's some interesting comments on Reddit about them - not looking good.

0 -

I've been cruising along fine on a trickle of money from Social Security and savings. Now the family that owns the house where I live wants to sell it to me. I need to get a mortgage. The monthly payment would be a couple few hundred more than I pay rent. And that same amount anywhere else would rent me two rooms in the deepest slums.Would a mortgage company look at my ability to pay (I'm able), or just look at the trickle and condemn me to losing everything I have?0

-

@wisdom_cracker If you're in retirement and your only income is the state pension then, with most conventional mortgages your max borrowing will be based on that.

If you have a hefty deposit to make the mortgage very low LTV (<60%) then there might be later-lending options (eg: Retirement Interest Only https://www.familybuildingsociety.co.uk/mortgages/later-life-mortgages/retirement-interest-only/retirement-interest-only-faqs ) from smaller building societies which look at affordability in a different way.Wisdom_Cracker said:I've been cruising along fine on a trickle of money from Social Security and savings. Now the family that owns the house where I live wants to sell it to me. I need to get a mortgage. The monthly payment would be a couple few hundred more than I pay rent. And that same amount anywhere else would rent me two rooms in the deepest slums.Would a mortgage company look at my ability to pay (I'm able), or just look at the trickle and condemn me to losing everything I have?I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards