We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Npower. Refused mortgage.

Comments

-

Unless you updated th with your new forwarding address they won’t spend time looking for you. It’s not their job to do that.0

-

I understand that, but for the sake of £58. We were always in credit, never in negative. Paid DD the whole time we were there. Assumed (wrongly) there would be credit in there to cover any final payment... There was... Just obviously not enough 🙄 Assumption is the mother of all, I know. Never had issues getting credit in the past either.0

-

Oh i see. I thought they fell off the date the default was createdDeleted_User said:

No. Accounts drop off six years from closure, or default if earlier.jazzyja said:Shouldn't it of dropped off on the 21/06/20? Who did you apply with?0 -

Yes, they do - if there's been a default.0

-

It definitely was in default as it went to a debt collectors, so I can't understand why it isn't listed as such. Do I have a case for them removing it as they haven't listed it properly??Deleted_User said:Yes, they do - if there's been a default.0 -

No. You have a case for them applying a default to the appropriate date.

0 -

Thanks for this. Will get in contact with them today.Deleted_User said:No. You have a case for them applying a default to the appropriate date.0 -

Gemm83 said:We are through a broker. He has been really good to be fair. We have a 17% deposit (based on house prices in the area) but the lenders that would overlook it are currently requiring a 20% deposit and there's no way we can get that extra 3% together. 🙄

Would this help anyone?

Back in Nov they said they had been chasing me for ages. Don't understand why though as have been on the electoral role at our current place for the past 2.5 years 🤔

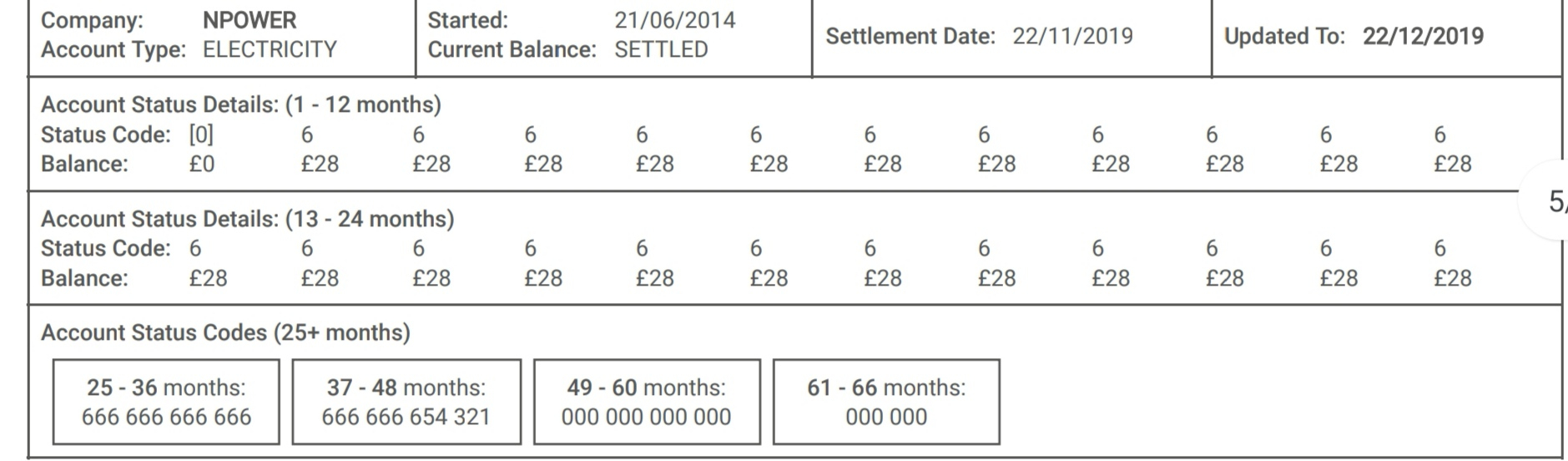

Just to clarify, this definitely hasn’t been registered as a default by NPower. A default is marked as a ‘status 8’ by Experian, status 6 which this was reported as is essentially as high as it goes when it comes to missed payments (without default).

As things stand the record remain on your file until 21/06/2025.0 -

Thanks for this Fletcher86. So can I ask.... What's the difference between missed payments (without default) and missed payments (with default)?0

-

A default means the lender has terminated your account and feel the agreement with you has reached an impasse. A default is a formal "Breach of contract, no turning back now"; whereas missed payments are arrears; e.g. the account has fallen behind, but can be brought up to date and the account can then be continued in good standing.

It seems to me that nPower in this instance, should have recorded a default when you fell 3-6 months behind, but didn't.

It's difficult to judge whether a default three or four years ago would be better or worse than what is currently recorded on your credit file. As it stands, you're likely to be ineligible for a mortgage until 12 months have passed since your last recorded missed payment at least, which was November in this case.

As the account doesn't appear on your Equifax or Trans Union credit file, have you considered using a lender which relies on Equifax, like Yorkshire Building Society? Or one who relies on Trans Union, like Skipton Building Society?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards