We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is he a BAD mortgage broker?

MaiseMeal

Posts: 21 Forumite

Property I want to buy for £240,000 was down valued by £15,000

I wanted to put a 20% deposit of £48,000, 80%LTV at 192,000 mortgage fixed 2 years

I told him i want to negotiaite with the sellers to get a cheaper price on the house. And he gives me this answer:

"Natwest will only assess the property based on their valuation of £225k. You can still proceed with the purchase and use the Natwest offer, however, we’d have to amend the product on the application to fit with the new loan to value that is based on the valuation figure (see my previous email with the different mortgage product options).

Otherwise, the only other option is to try the next best mortgage lender and get them to value to the property.

£225k is the valuation that the surveyor has put on the property, so this is what Natwest will use. I’m afraid they won’t work with any other figure now the valuation has been carried out."

The mortgage advisor would rather I increase my LTV and get higher interest rates than even try and negotiaite money off the house price.

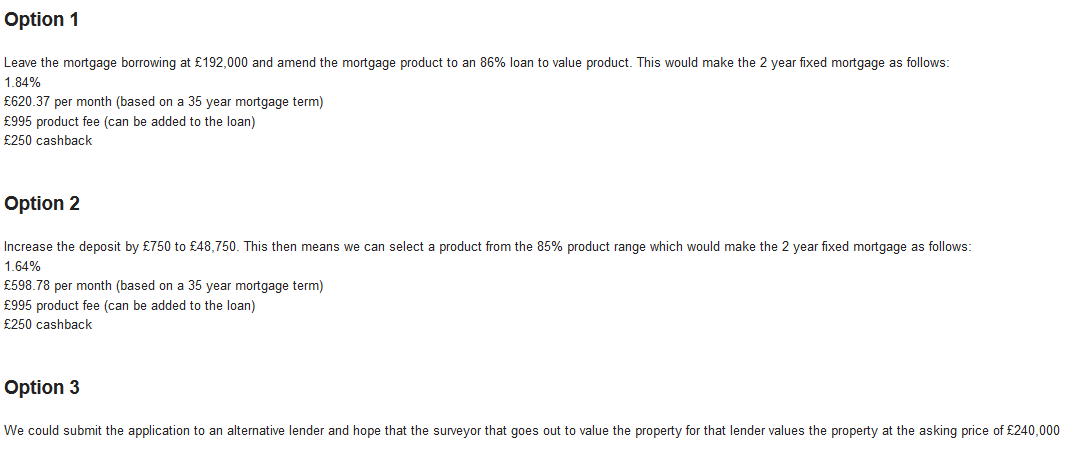

He gave me these options:

I'm trying to at most go halfway with the sellers by doing £7,500 making purcahse price £232,500

I wanted to put a 20% deposit of £48,000, 80%LTV at 192,000 mortgage fixed 2 years

I told him i want to negotiaite with the sellers to get a cheaper price on the house. And he gives me this answer:

"Natwest will only assess the property based on their valuation of £225k. You can still proceed with the purchase and use the Natwest offer, however, we’d have to amend the product on the application to fit with the new loan to value that is based on the valuation figure (see my previous email with the different mortgage product options).

Otherwise, the only other option is to try the next best mortgage lender and get them to value to the property.

£225k is the valuation that the surveyor has put on the property, so this is what Natwest will use. I’m afraid they won’t work with any other figure now the valuation has been carried out."

The mortgage advisor would rather I increase my LTV and get higher interest rates than even try and negotiaite money off the house price.

He gave me these options:

I'm trying to at most go halfway with the sellers by doing £7,500 making purcahse price £232,500

0

Comments

-

You can renegotiate the purchase price, but he is right, natwest will still work on the assumption that it is valued at £225k even if you renegotiate to £230k.

So effectively you can still purchase put you will still end up on a higher LTV product. However, if you were to renegotiate to £225k you could keep your 80% product.

It could just be a misunderstanding in communication?I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

I don't understand why you think he's a bad mortgage broker? Everything he has said is sensible?Know what you don't0

-

BAD mortgage broker. No biscuit.

The broker has nothing to do with what price you negotiate. He's merely finding you somebody willing to lend you however much you need.

What he's telling you is that NW are simply regarding the surveyor's value as the figure they'll use for calculating LtV, should you pay more. No more, no less.0 -

From his emails it seems he doesnt want me to negotiate a lower price on the house. I have put foward how strongly I want to reduce the purchase price of the house and he is replying as if thats not an option.I don't understand why you think he's a bad mortgage broker? Everything he has said is sensible?

I was buying a house this year July (fell through) and it was undervalued by £10,000 with Natwest direct from website and they accepted the mortgage. So im surprised when I have decided to go with broker, there's no wiggle room.0 -

You're reading something into his emails that isn't there.

You can negotiate whatever price you want and if you end up needing to borrow less, then you borrow less.

Your negotiations are nothing to do with him apart from him telling you the max you can borrow.0 -

Bad broker or bad customer?

I think I know.0 -

From his emails it seems he doesnt want me to negotiate a lower price on the house. I have put foward how strongly I want to reduce the purchase price of the house and he is replying as if thats not an option.

I was buying a house this year July (fell through) and it was undervalued by £10,000 with Natwest direct from website and they accepted the mortgage. So im surprised when I have decided to go with broker, there's no wiggle room.

You can negotiate whatever price you like but that is nothing to do with him. He is working on the assumption that the price is the price you have told him.

You seem to be aware that negotiating a lower price is an option you have, so what is your issue?0 -

If you negoatiate a lower price its not a issue, natwest would reduce the borrowing amount to account for the deposit.

All your broker is stating is that they wont change the valuation of the property not the borrowing.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards