We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Battery Electric Vehicle News / Enjoying the Transportation Revolution

Comments

-

Big BEV news, or perhaps, news about big BEV's, as the expansion of huge BEV's at Fortescue's Australian iron ore mine continues.

XCMG unveils world’s biggest all-electric wheel loader for FortescueXCMG celebrated the launch of its new, massive XC9260BEWL and XC9260BEWD lines by delivering one of each to Australian mining giant, Fortescue – part of a record-setting $400 million electric equipment order meant to help slash the company’s carbon emissions.

Unveiled this week at a formal ceremony in Xuzhou, China, the XC9260BEWL (battery electric wheel loader) and XC9260BEWD (battery electric wheel dozer) are built to meet or exceed the performance of XCMG’s diesel-hybrid XC9260 electric drive machines (above), which offer the same 783 kW (~1050 hp) electric motor as the battery-electric versions. Extending the similarities further, that should give the BEVs the same 127,000 kg (~280,000 lbs.) payload capacity and high-production bucket capacities (ranging from 11.5 to 14.5 cubic meters, or 15–19 cubic yards) as the hybrid machines, as well.

Fortescue is on track to deploy up to 100 similarly massive 70-130 ton battery electric haul trucks, loaders, and dozers from XCMG in its quest to reach “real zero” emissions at its iron mining operations in Australia’s Pilbara by 2030, meaning it will burn no fossil– or bio-based fuels for mining, transport, or power.

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.2 -

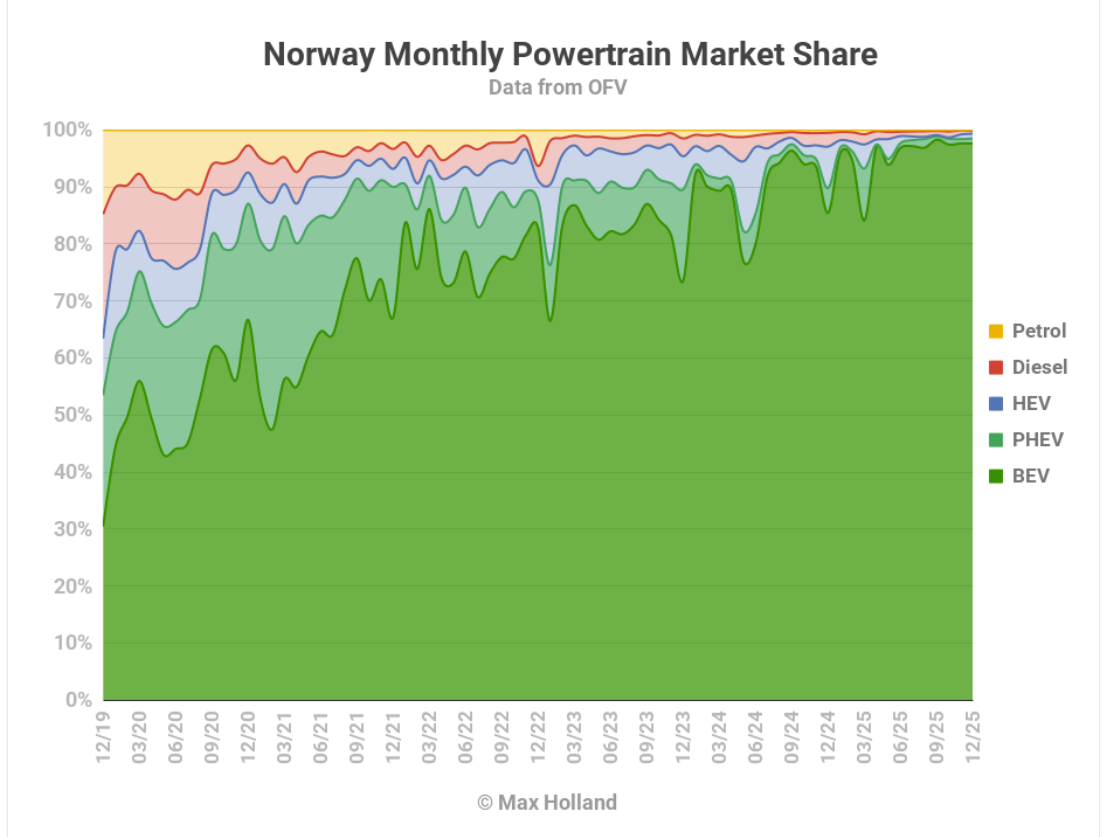

Sad news regarding Norway. 2025 was the last year of significant BEV sale %age increases. The good news of course, is because there simply isn't much further they can go, having increased for the year as a whole, from 91.3% to 97.5%. Mission accomplished …… (too soon?)

Also, potentially 'buried the lede', with the suggestion that for the fleet as a whole, BEV's may now have overtaken diesels, to become the single largest component of the whole Norwegian car fleet at ~32%.

2025 Saw EVs At 97.5% Share In Norway — Tesla Model Y Best-SellerDecember saw plugin EVs at 98.5% share in Norway, up from 89.8% year on year, with BEVs alone taking 97.6% share. Full year 2025 saw EVs at 97.5% share in Norway, up from 91.3% YoY, with all the growth coming from BEVs.

The latest BEV share figure given for the end of Q4 2025 is 32.1% of the fleet, and that’s up from 30.6% at the end of Q3. This is a larger than normal increase in share (it’s usually up around 1% per quarter), because December was an anomalously high sales volume month.

By my reckoning the diesel fleet share should now be down to around 31.5% share, and petrol down to 24.1%. HEVs and PHEVs combined are hovering around 12.5% (these have now both peaked and are on a slow decline).

Is this graph a thing of beauty?

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.5 -

In that graph showing the percentage market share for alternative fuel types there are a few blips down in the EV outcome with the deficit made up by a sudden but short-lived surge in hybrids. Five such events since beginning 2023 by the looks of it. Why are there these odd hybrid surges?

0 -

I think those periods coincide with Norway's BS internet filter failing to block the Daily Fail for short times during essential maintenance. ;-)

4.7kwp PV split equally N and S 20° 2016.Givenergy AIO (2024)Seat Mii electric (2021). MG4 Trophy (2024).1.2kw Ripple Kirk Hill. 0.6kw Derril Water.Vaillant aroTHERM plus 5kW ASHP (2025)Gas supply capped (2025)4 -

thevilla may be onto the issue. But otherwise, it could be many things, such as months with delivery issues for BEV's (such as Tesla shipping dates), or maybe pull forwards for BEV's or PHEV's due to policy changes, thus relating in weird months.

And also periods that look 'odd', linked to those or other reasons, but because the graph reflects %age, not absolute sales. So for instance, BEV's may look stronger, or weaker, due to a rise or fall in their sales, but because the period still adds up to 100%, 'others' may look greater or smaller (in %ages) even if their actual sales numbers haven't changed much.

But I'm only guessing/pondering. It may well be possible to identify a specific monthly article from Cleantechnica (in their search menu), to see if there's an explanation for the spike. Though the reason may relate (as mentioned above) more to a relative fluctuation against a month or so, before or after.

Clear as mud!

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.3 -

Decided to follow my own advice and have a look back.

Found the May 2024 and June 2024 articles, both of which suggested reasons for the apparent (short lived) spike in HEV's.

May 2024 (BEV's 77%, HEV's 12%):

The relatively low BEV volume (and market share) in May is not due to some sudden reversal of buying preferences from the average Norwegian consumer, but instead most likely due to a temporary shipping logistics dip from the three most popular manufacturers. The BEVs from BMW, Volkswagen Group, and Tesla, remain popular in Norway in recent months, though Tesla and VW Group are losing share compared to recent years. Each of these big three brands had a big volume dip in May compared to April, which strongly suggests the influence of erratic shipping allocations, which small markets (like Norway) can suffer from.

Long story short – BEVs likely don’t have any significant demand-side problem in Norway — beyond the broader economic slowdown — as they are as popular as ever so far this year in terms of market share. However, small volume markets are vulnerable to the vagaries of batch shipments and erratic temporary allocation priorities, in other words, supply-side challenges.

With BEVs at temporary low volume, other powertrain shares looked relatively shiny in May. For some reason (ask Toyota), May is one of the year’s peak months for plugless HEV sales, so HEV share temporarily looked good at 12.2%. Stepping back, year to date HEV volume is down 15% from the same period in 2023, and their overall share has fallen, currently at 6.4%.

June 2024 (BEV's 80%, HEV's 12%):

It’s not clear why HEV volumes (mostly Toyota) were so much higher than a year ago. It could possibly be related to a pull-forward (or firesale, if you prefer) ahead of new vehicle safety regulations about to hit (more on these below). I would have guessed that almost all of Toyota’s HEV vehicles are already compliant, however (unlike their combustion GR86, which is not compliant, and will be cancelled in Europe). If you have insights on this, or other factors around HEVs, please let us know in the comments.

In the May report, we noted that the YoY fall in that month’s BEV volume was likely due to an unusual shipping shortfall from each of the most popular manufacturers (Tesla, BMW Group, and Volkswagen Group). BMW Group was back close to seasonal norms in June, whereas Volkswagen Group is still down by around 40% from June 2023 (likely prioritising shipping to other markets). Tesla, however, recovered and was 6.5% up in volume from June 2023.

New EU Vehicle Safety Regulations

June was the last full month of sale before new EU vehicle safety rules (GSR2 rules, hammered out in 2019–2020) become mandatory for all new vehicle sales in the region. Because it doesn’t make sense for manufacturers to make substantially different models for small individual markets which are part of the same regional logistics group, these rules also spill over to EU-adjacent markets like Norway, and to some extent, the UK. Previously, models launched prior to 2022 and not originally designed with the new rules in mind were given a temporary pass (while all-new models launched after 2022 had to comply).

From the 7th of July, after 4 years of lead time from when the rules were formulated, there are no more exceptions. Now mandatory on all new vehicles sold are automatic safety features such as: speed limit assistance, emergency braking assist, collision avoidance assist, lane keep assist, drowsiness monitoring and warning, reversing sensors/camera, and event data recorder (aka “blackbox”).

Vehicles based on older platforms and architectures which preclude the practical addition of these features are thus stopping sale in the region. For example, this is the main reason why the Renault Zoe — on a vehicle architecture launched in 2011 — ceased selling earlier this year.

Mart. Cardiff. 8.72 kWp PV systems (2.12 SSW 4.6 ESE & 2.0 WNW). 28kWh battery storage. Two A2A units for cleaner heating. Two BEV's for cleaner driving.

For general PV advice please see the PV FAQ thread on the Green & Ethical Board.4 -

And on the flip side

https://www.thisismoney.co.uk/money/cars/article-15566615/Vauxhall-Stellantis-resurrect-diesel-cars-19bn-hit-EV-sales.html

Vauxhall owner Stellantis resurrects diesel cars after taking a £19bn hit from EV sales slump

……. it has already started reintroducing diesel engines across its model ranges, adding them as a powertrain option for seven cars and vans across its line-up.

0 -

I wouldn't want a Stellantis diesel either..

2 -

That’s a personal choice but Peugeot has historically made very good diesel engines. I did over 200,000 miles trouble free in company Citroen Xantias which ran PSA 1.8 and 2.1 diesel engines.

In fact PSA diesel engines are so well regarded that other manufacturers including JLR, ford, Mini (the BMW version) and even Toyota have partnered with them for some of their diesel offerings.

Northern Lincolnshire. 7.8 kWp system, (4.2 kWwest facing panels , 3.6 kWeast facing), Solis inverters installed 2018, 5kW SSE facing system (shaded in afternoon) added in 2025 with Tesla PW3 battery, Mitsubishi SRK35ZS-S and SRK20ZS-S Wall Mounted A2A Heat Pumps, ex Nissan Leaf owner.0 -

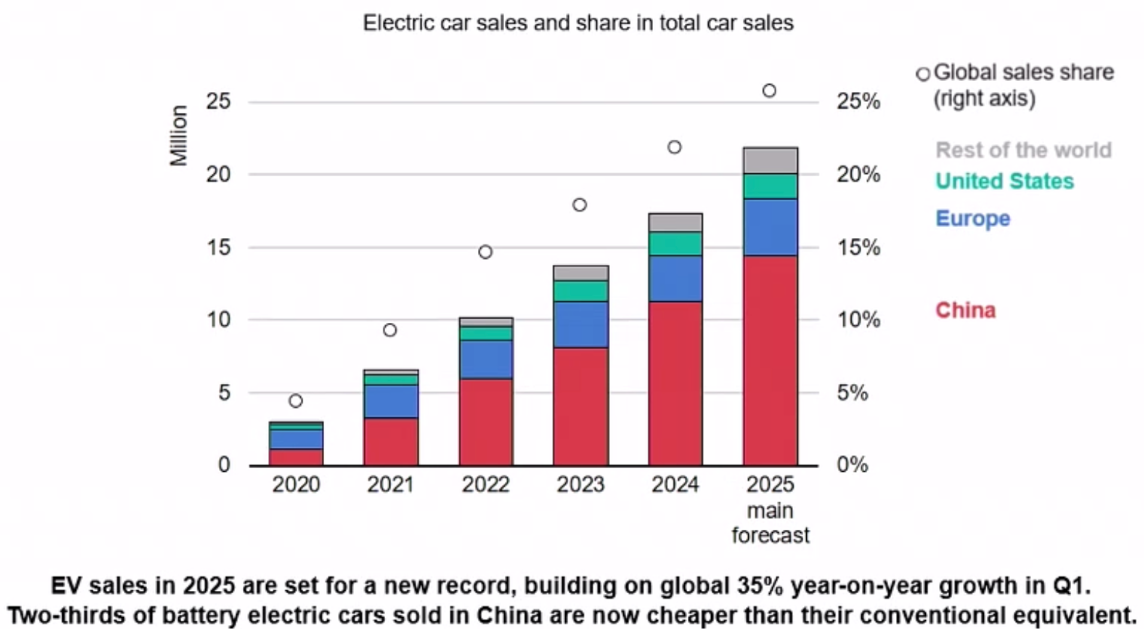

What slump? IEA figure:

Fully expect to see Stellantis get the begging bowl out for subsidies and calls for tariff protections from Chinese makers who were better prepared for the transition.

Solar install June 2022, Bath

4.8 kW array, Growatt SPH5000 inverter, 1x Seplos Mason 280L V3 battery 15.2 kWh.

SSW roof. ~22° pitch, BISF house. 12 x 400W Hyundai panels3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards