We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Top Easy Access Savings Discussion Area

Comments

-

Another video from the Chip co-founder, the second one since the last BoE rate rise. If we didn't know already, it's pretty clear now that they are not about to beat Tandem. IMO there is no point in giving them more time in the hope they'll make a move any day soon..

https://youtu.be/Fldyyrdegu0

https://youtu.be/Fldyyrdegu0

3 -

Yep, having just received a £15.75 Topcashback bonus from Kroo for opening an account with them, I have now moved the remaining balance from Kroo to my 5% Tandem a/c.1

-

This isn't actually a change from Kroo, the current 4.35 is BR-.9 anyway, it's just going to be automatic now. They aren't becoming uncompetitive, they never were competitive in the first place.

Also just watched the Chip video... so they want to focus on having the fastest payments with lower rates. You know who else has the fastest payments... Atom

Points to who guessed they were working on an ISA.3 -

I think Chip might be stuffed.1

-

I'm surprised at the criticism of Kroo. They are a current account, not a savings account. No other current account pays more.5

-

7% eh. Oh well thats the first port of call for my funds then.0

-

Anyone with experience of Oxbury? They do an EA at 4.8 but was thinking of the 95 day notice account. But has pretty bad reviews especially of the app1

-

Sounds like that you can apply for Edge, open the Saver and downgrade after and fill the saver to the brim and skim off the monthly interest. However, if you do not meet the cashback criteria it seems like they won't charge you.Malchester said:

I opened an ordinary Santander Current Account and later changed it to an Edge account to get the Edge Saver Account when the rate was a good one. Overall the monthly fee alongside the interest and cashback gave me a plus. Then when other easy access accounts improved rates I switched my Edge Account to a non-fee account but the Edge Saver was allowed to run and gain interest. I have since switched back to Edge and filled the Edge Saver to its maximum for the 7% interestpecunianonolet said:

So, basically open the current account, open the Edge saver and leave the current account dormant, maybe bounce a few quid through so it qualifies for yougov.aaj123 said:

Whoa, good spot! Never occurred to me to be honest. I wonder what prompted them to put in such a strange conditional start of the £3 fee seeing as the fee continues once started even if you later fail the conditions.Bridlington1 said:

You don't really have to pay the £36/yr if I'm not mistaken. The terms say:aaj123 said:

No way to get this without an Edge current account, is there? I really like my 123 current account. Sure, one could think of getting an effective 6.1% by paying the £36 for the year and maxing out the 4k.Bridlington1 said:The fee for this account is £3 per month. We’ll start charging this fee after you meet the conditions for earning cashback for the first time. Then, we’ll take it from your account each month on the anniversary of the date you opened it. We’ll do this every month until your account is closed. This includes any months where you don’t earn cashback. If you don’t have enough money available to cover the monthly fee, we’ll still take it and your account may go into an unarranged overd

If you never meet the criteria for earning cashback, you won't pay any fees. So if you never have any DDs on the Edge account you won't have to pay the £3/mth account fee.

"If the rate goes down, we’ll let you know around 2 months before the rate changes." is a rather long period as well in todays agile market.

If they would now introduce a switch bonus as well it would make the current account opening even more worthwhile.

All I can quote in that instance....

"Dreams are my reality

The only kind of real fantasy

Illusions are a common thing

I try to live in dreams

It seems as if it's meant to be"

However, they also say "You’ll need to continue to hold a Santander Edge current account to stay eligible for exclusive products. If you stop being eligible, we may close or downgrade your exclusive product(s)"

Looks like it is at their discretion to keep the saver running or not after a downgrade.

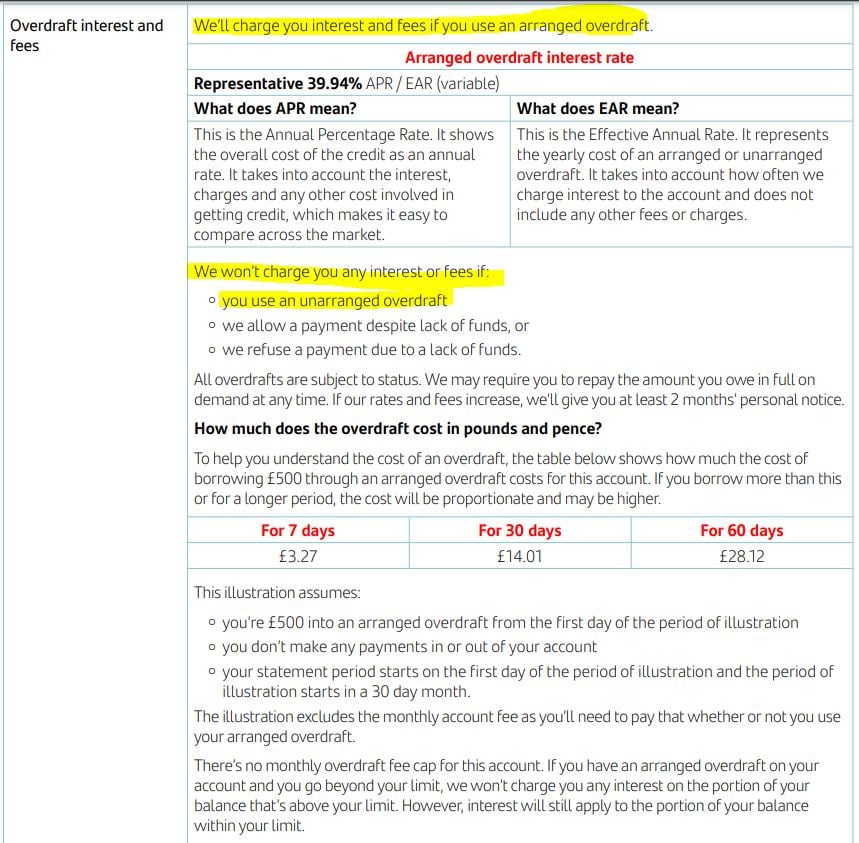

By reading the T&C's I find the below very odd. If you have an arranged overdraft they charge you for it but going for an unarranged overdraft they don't. It would be taking the p*** and the famous Santander algorithm will most likely put your file on somebodys desk for review but otherwise an opportunity for some stoozing.

0 -

I would certainly advise against stoozing an unarranged OD. Aside from the fact that you risk irritating Santander a fair bit, I can't imagine having a potentially quite substantial unarranged OD for any length of time would do your credit reports much good.pecunianonolet said:

Sounds like that you can apply for Edge, open the Saver and downgrade after and fill the saver to the brim and skim off the monthly interest. However, if you do not meet the cashback criteria it seems like they won't charge you.Malchester said:

I opened an ordinary Santander Current Account and later changed it to an Edge account to get the Edge Saver Account when the rate was a good one. Overall the monthly fee alongside the interest and cashback gave me a plus. Then when other easy access accounts improved rates I switched my Edge Account to a non-fee account but the Edge Saver was allowed to run and gain interest. I have since switched back to Edge and filled the Edge Saver to its maximum for the 7% interestpecunianonolet said:

So, basically open the current account, open the Edge saver and leave the current account dormant, maybe bounce a few quid through so it qualifies for yougov.aaj123 said:

Whoa, good spot! Never occurred to me to be honest. I wonder what prompted them to put in such a strange conditional start of the £3 fee seeing as the fee continues once started even if you later fail the conditions.Bridlington1 said:

You don't really have to pay the £36/yr if I'm not mistaken. The terms say:aaj123 said:

No way to get this without an Edge current account, is there? I really like my 123 current account. Sure, one could think of getting an effective 6.1% by paying the £36 for the year and maxing out the 4k.Bridlington1 said:The fee for this account is £3 per month. We’ll start charging this fee after you meet the conditions for earning cashback for the first time. Then, we’ll take it from your account each month on the anniversary of the date you opened it. We’ll do this every month until your account is closed. This includes any months where you don’t earn cashback. If you don’t have enough money available to cover the monthly fee, we’ll still take it and your account may go into an unarranged overd

If you never meet the criteria for earning cashback, you won't pay any fees. So if you never have any DDs on the Edge account you won't have to pay the £3/mth account fee.

"If the rate goes down, we’ll let you know around 2 months before the rate changes." is a rather long period as well in todays agile market.

If they would now introduce a switch bonus as well it would make the current account opening even more worthwhile.

All I can quote in that instance....

"Dreams are my reality

The only kind of real fantasy

Illusions are a common thing

I try to live in dreams

It seems as if it's meant to be"

However, they also say "You’ll need to continue to hold a Santander Edge current account to stay eligible for exclusive products. If you stop being eligible, we may close or downgrade your exclusive product(s)"

Looks like it is at their discretion to keep the saver running or not after a downgrade.

By reading the T&C's I find the below very odd. If you have an arranged overdraft they charge you for it but going for an unarranged overdraft they don't. It would be taking the p*** and the famous Santander algorithm will most likely put your file on somebodys desk for review but otherwise an opportunity for some stoozing.4 -

Totally agree, it would only be short term stoozing with low amounts e.g. 100 quid for 3 days to "cover" a payment for example. Surely not to take out 4k unarranged overdraft to put in the saver at the same timeBridlington1 said:

I would certainly advise against stoozing an unarranged OD. Aside from the fact that you risk irritating Santander a fair bit, I can't imagine having a potentially quite substantial unarranged OD for any length of time would do your credit reports much good.pecunianonolet said:

Sounds like that you can apply for Edge, open the Saver and downgrade after and fill the saver to the brim and skim off the monthly interest. However, if you do not meet the cashback criteria it seems like they won't charge you.Malchester said:

I opened an ordinary Santander Current Account and later changed it to an Edge account to get the Edge Saver Account when the rate was a good one. Overall the monthly fee alongside the interest and cashback gave me a plus. Then when other easy access accounts improved rates I switched my Edge Account to a non-fee account but the Edge Saver was allowed to run and gain interest. I have since switched back to Edge and filled the Edge Saver to its maximum for the 7% interestpecunianonolet said:

So, basically open the current account, open the Edge saver and leave the current account dormant, maybe bounce a few quid through so it qualifies for yougov.aaj123 said:

Whoa, good spot! Never occurred to me to be honest. I wonder what prompted them to put in such a strange conditional start of the £3 fee seeing as the fee continues once started even if you later fail the conditions.Bridlington1 said:

You don't really have to pay the £36/yr if I'm not mistaken. The terms say:aaj123 said:

No way to get this without an Edge current account, is there? I really like my 123 current account. Sure, one could think of getting an effective 6.1% by paying the £36 for the year and maxing out the 4k.Bridlington1 said:The fee for this account is £3 per month. We’ll start charging this fee after you meet the conditions for earning cashback for the first time. Then, we’ll take it from your account each month on the anniversary of the date you opened it. We’ll do this every month until your account is closed. This includes any months where you don’t earn cashback. If you don’t have enough money available to cover the monthly fee, we’ll still take it and your account may go into an unarranged overd

If you never meet the criteria for earning cashback, you won't pay any fees. So if you never have any DDs on the Edge account you won't have to pay the £3/mth account fee.

"If the rate goes down, we’ll let you know around 2 months before the rate changes." is a rather long period as well in todays agile market.

If they would now introduce a switch bonus as well it would make the current account opening even more worthwhile.

All I can quote in that instance....

"Dreams are my reality

The only kind of real fantasy

Illusions are a common thing

I try to live in dreams

It seems as if it's meant to be"

However, they also say "You’ll need to continue to hold a Santander Edge current account to stay eligible for exclusive products. If you stop being eligible, we may close or downgrade your exclusive product(s)"

Looks like it is at their discretion to keep the saver running or not after a downgrade.

By reading the T&C's I find the below very odd. If you have an arranged overdraft they charge you for it but going for an unarranged overdraft they don't. It would be taking the p*** and the famous Santander algorithm will most likely put your file on somebodys desk for review but otherwise an opportunity for some stoozing.") .

.

Risk vs. gain are obvious. It was more the fact and the anomaly that they charge you for something you have an agreement with them but borrowing without agreement is free. Much more sensible would be be to charge e.g. 10% interest for an arranged overdraft and 40% for unarranged.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards