We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Do people budget for interest rate rises?

Comments

-

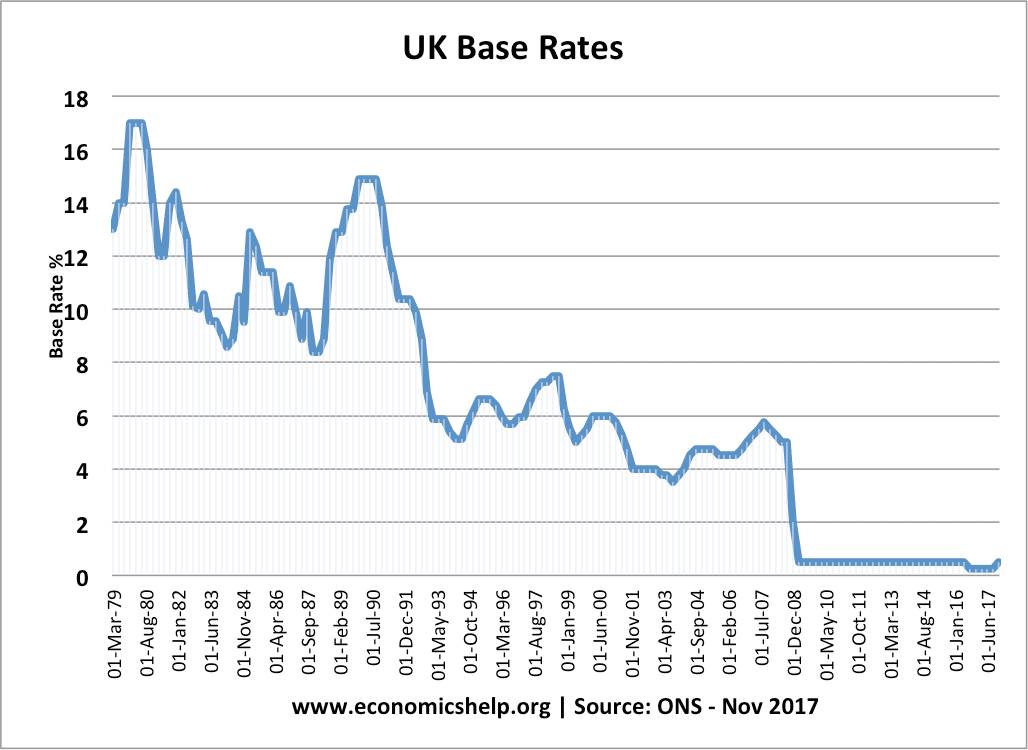

This demonstrates it beautifully - it's the low, low rates of the last decade which are the exception, not higher rates.

This demonstrates it beautifully - it's the low, low rates of the last decade which are the exception, not higher rates.

~4-5% is the long-term median rate.

The low rate has gone on for some years now, so its a lot more stable than the high rates of the past.

That being said, interest rates cannot be predicted 2+ in advance.

No one back in 2006/07 predicted the almost zero interest rates were coming on 2009/10; so it would be very difficult for anyone now, to say what the interest rates will be in 20200 -

walwyn1978 wrote: »We did/do. But my honest guess based on the last few years of extremely low interest rates and high house prices is that a lot of people are maxed out on their affordability and if (when) rates go up there will be tears.

That`s my guess too.0 -

“ Do you think people are generally prepared for higher interest if it does happen?

Originally posted by lookstraightaheadMobileSaver wrote: »Mortgage affordability rules mean that lenders have already checked that people can afford rates of around 7% or 8% so, at least for the foreseeable future, it is highly unlikely that many people will get into trouble.

Don't bank on that - they may well have taken out other financial commitments since the mortgage check.0 -

sevenhills wrote: »The low rate has gone on for some years now, so its a lot more stable than the high rates of the past.

That being said, interest rates cannot be predicted 2+ in advance.

No one back in 2006/07 predicted the almost zero interest rates were coming on 2009/10; so it would be very difficult for anyone now, to say what the interest rates will be in 2020

If the Fed are raising the chances are they will rise, interest rates are rising globally as well.0 -

Theres pros and cons of high interest rates.

One of the cons is you have to pay more for borrowing.

One of the pros is that the reason youre paying more is because there is an abundance of money floating around in the economy.

I would happily take 15% interest rates. Its basic supply and demand. If people want money, interest rates go up, if people dont want money they go down. People do not borrow money to put in their bank, they dont borrow money to put food on the table, they dont borrow money to flitter it away. They borrow money to invest in a house, invest in business or infrastructure. And what happens when you invest in thigns, you expect a return. No one borrows £200k to buy a £100k house. They borrow £100k to avoid paying £200k in rent, we call this a benefit.

Everyone thinks high interest rates would be terrible, the opposite side of that is it suggest the economy is booming and its not unusual for such a boom to offset the high costs and more as seen in the 70's and 80's0 -

Theres pros and cons of high interest rates.

One of the cons is you have to pay more for borrowing.

One of the pros is that the reason youre paying more is because there is an abundance of money floating around in the economy.

I would happily take 15% interest rates. Its basic supply and demand. If people want money, interest rates go up, if people dont want money they go down. People do not borrow money to put in their bank, they dont borrow money to put food on the table, they dont borrow money to flitter it away. They borrow money to invest in a house, invest in business or infrastructure. And what happens when you invest in thigns, you expect a return. No one borrows £200k to buy a £100k house. They borrow £100k to avoid paying £200k in rent, we call this a benefit.

Everyone thinks high interest rates would be terrible, the opposite side of that is it suggest the economy is booming and its not unusual for such a boom to offset the high costs and more as seen in the 70's and 80's

The problem with your theory is that demand for debt has never been higher, but interest rates have never been lower?0 -

Yes. You'd be daft not to.

Rates are at rock bottom - all they can do is go up. The only unknown is when.No longer a spouse, or trailing, but MSE won't allow me to change my username...0 -

People do not borrow money to put in their bank, they dont borrow money to put food on the table, they dont borrow money to flitter it away.

Sorry to quibble, but people definitely do borrow money for the last two out of that list, sadly.

Go on the debt free wannabe board to see how many people end up in trouble because they had to borrow just to live when they fell on hard times, or who got trapped in a gambling spiral, or have huge credit card balances with hardly anything to show for it and barely any memory of where the money actually went.0 -

trailingspouse wrote: »Yes. You'd be daft not to.

Rates are at rock bottom - all they can do is go up. The only unknown is when.

They can go negative

https://www.ft.com/content/bcc092fc-7743-11e6-a0c6-39e2633162d5

Admittidely seems unlikely but ultimately if you're saying it's totally unpredictable over more than a couple of years you have to include this possibility.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards